Global X has been a pioneer in the covered-call ETF space, and the Global X Nasdaq 100 Covered Call ETF (NASDAQ:QYLD) is considered its flagship with $7.96 billion in net assets. Global X was managing covered calls ETFs well before they became popular, and it has been synonymous with generating double-digit yields for years. From an income investment perspective, QYLD has continued to perform throughout the years, even if the share price has been in a perpetual decline. When it comes to QYLD, there has always been a debate about its viability due to the fund’s mechanics. Global X is extremely clear that QYLD is geared toward investors looking to generate income through writing covered calls rather than discussing generating capital appreciation. I am now neutral on QYLD rather than being bullish because the sector for covered call ETFs has evolved, and I like some of the other strategies more. They leave more room for appreciation, as the entire fund isn’t capped. QYLD is still a strong fund for income, but if we get a rally from rate cuts, it is likely to underperform similar high-income funds.

Seeking Alpha

Following up on my previous article about QYLD

In my previous article about QYLD, I discussed why the opportunity cost of an appreciating market may not outweigh the needs of an income-focused investor when it comes to QYLD (can be read here). Since the article was written on April 10th, the S&P 500 has appreciated by 8.21%, and QYLD has declined by -0.84%. QYLD has generated monthly income, and when the distributions are taken into consideration, its total return is 4.13%. I am following up with a new article to discuss why I am no longer bullish on QYLD, and downgrading my investment thesis to neutral. I think QYLD is a solid fund for income investors who can tune out the noise and not look at the fluctuating share price and just focus on the income being generated. The covered call space has evolved, and I think there are other funds that are more appealing than QYLD.

Seeking Alpha

Risks to my investment thesis

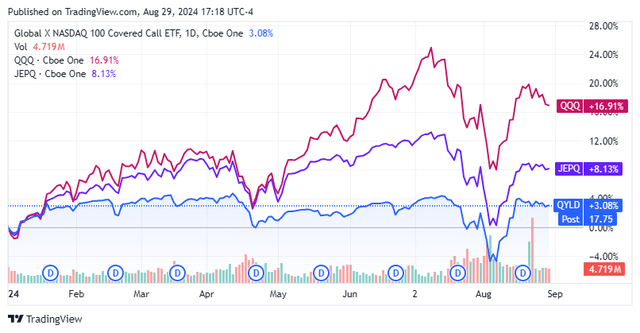

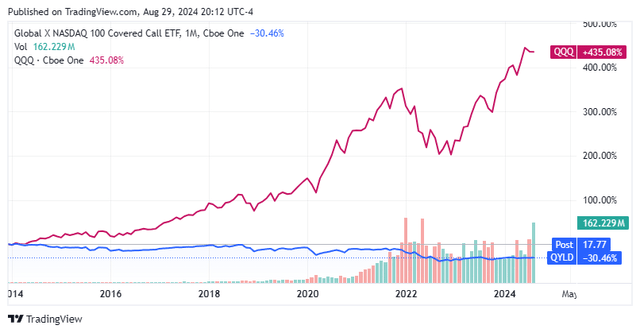

While I am still a shareholder of QYLD, I am no longer as bullish as I once was. There are several risks to my investment thesis and to my own investment in QYLD. It’s been over a decade since QYLD went public and shares have declined by -28.96% despite the Nasdaq climbing 377.54%. Investors could continue to see price erosion or a stagnant share price as the Nasdaq potentially benefits from tailwinds from rate cuts. QYLD has tremendous opportunity costs because of its covered call strategy, and while investors are allocating capital toward QYLD for income, opportunity costs are real risks. The other main risk is that QYLD’s income fluctuates, and there is a risk that future distributions won’t be as large as previous ones. Ultimately, QYLD has lived up to its investment thesis and opinions vary if the fund’s structure has been a net positive for investors. QYLD could continue to underperform the market, and its future income could be impacted. Investors should consider the risks because this is a unique fund with a dedicated strategy for the specific outcome of generating income.

The facts are that QYLD has lived up to its investment objectives for its shareholders

Everyone has an opinion, and whether QYLD is a good investment depends on an individual’s goals. QYLD invests in the companies that create the Nasdaq 100 index, then writes covered calls against the positions to generate income. The fund has a specific objective to generate immediate recurring income by selling either at the money or close to the money covered calls each month. QYLD trades most of the potential upside for an upfront premium, which is paid to shareholders on a monthly basis in the form of distributions. The income generated by the distributions fluctuates each month as the premiums in the options markets constantly change. QYLD is currently yielding 11.63% based on the TTM distributions, and despite what the bears think about the mechanics, QYLD has outpaced the risk-free rate of return since its inception.

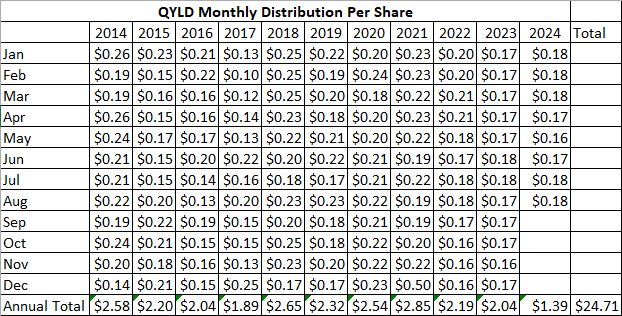

QYLD went IPO on 12/16/13 at $25 and has never missed a monthly distribution. Currently, shares of QYLD trade for $17.76, which is a decline of -$7.24 or -28.96%. Long-term investors have endured capital appreciation since its inception as QYLD has spent minimal time above $25. Over this period, QYLD has paid 128 monthly distributions and generated $24.71 of income throughout the years. QYLD has paid 98.82% of its initial share price in income over the years while generating a 69.86% ROI since inception when accounting for the distributed income. While the share price has declined, QYLD has never claimed it was constructed to generate capital appreciation. Based on QYLD’s goals, the primary objective is being achieved despite a declining share price.

Some will argue that the opportunity cost of underperforming the market isn’t worth it while others will cite that they would have an income-producing asset still operating at 100% that has generated 98.82% of the initial investment in income. This is an investment that is very specific in its objectives, and who should consider allocating capital toward it. The bears would be correct in saying that despite the income generated, QYLD’s share price over time has declined despite being in a long-term bull market cycle. Bulls would be correct in saying that despite the declining share value, income is being generated each month without having to deplete their share count by selling each month.

Steven Fiorillo, Global X

Why I am turning neutral on QYLD

There is no question that QYLD has been a strong income-producing asset for more than a decade, but its strategy hasn’t evolved. By selling covered calls at the money or close to the money, QYLD hasn’t been able to capitalize on the perpetual bull market of the past decade. The disconnect between QYLD and QQQ has only increased over time. It has been frustrating that when the market sells off, it’s often hard for QYLD to rebound because it’s writing new covered calls very close to where the current share price is, which caps the upside potential when the market rebounds. When the market crashed in 2022, the drawdown in QQQ was significantly more drastic than in QYLD, but QQQ ultimately rebounded and made new highs whereas QYLD didn’t. This is because investors are sacrificing all forms of upside appreciation, whether it’s making new highs or rebounding off of a sell-off for immediate income.

Seeking Alpha

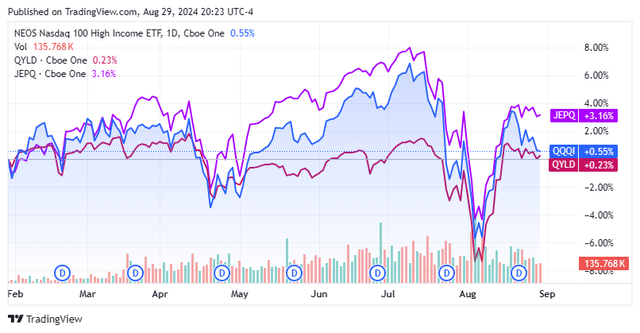

If you’re willing to sacrifice upside appreciation for income, then QYLD has a fantastic track record of consistently generating double-digit annual yields. I am invested in QYLD, but I am not adding to my position. At this point, I prefer the structure from the NEOS Nasdaq-100 High Income ETF (QQQI) or the JPMorgan Nasdaq Equity Premium Income ETF (JEPQ) more. QQQI utilizes a call option spread strategy where it writes covered calls to generate income and uses some of the premium to purchase out-of-the-money calls to participate in some upside if there is a strong rally in the market. JEPQ invests 80% of its assets in the Nasdaq 100 while utilizing up to 20% for ELN’s. JEPQ deploys a covered call strategy within the ELN portion of the portfolio while leaving the investments in the Nasdaq 100 uncapped. While it’s not much, QQQI and JEPQ have both outperformed QYLD over the past year on price appreciation. QQQI is on pace to generate about a 14% yield for its first year as an ETF, and JEPQ has generated a 9.3% yield over the TTM. I have been adding to JEPQ and QQQI rather than QYLD over the recent months.

Seeking Alpha

Conclusion

QYLD will always be a pioneer in the covered call ETF space that has never missed a distribution. Despite the price erosion, QYLD has produced 98.82% of its initial share price from distributions, and long-term investors still have an income-producing asset in their hands, churning out monthly payments. As the income space for ETFs evolved, other funds, such as JEPQ and QQQI, have become more interesting. I am still a shareholder of QYLD and reinvest the distributions each month, but I am no longer bullish as some of the other strategies are more aligned with what I am looking for in an income-producing fund. I am ok giving up most of the upside to generate income, but I do want to benefit as the markets appreciate, and QYLD’s strategy is more constricted than other ETFs that are able to produce similar yields. At this point, I would just hold QYLD, as there are other funds out there that have taken a hybrid approach to try and achieve a dual outcome.

Read the full article here