Broadcom’s Leading Position In AI

Broadcom Inc. (NASDAQ:AVGO) is one of the most important semiconductor companies beyond the semi value chain. Its exposure to the leading hyperscalers and cloud data center customers underscores its vital position in the AI upcycle. In addition, it has substantial non-AI revenue that’s inherently more cyclical, affected by broad macroeconomic cycles. The recent integration with VMware has also enhanced its enterprise software and cybersecurity capabilities, bolstering its infrastructure software revenue segment.

Therefore, there’s little doubt that Broadcom is widely considered a semiconductor bellwether. Understanding AVGO’s primary growth drivers is crucial to assessing whether the AI-led semiconductor upcycle can continue its stellar performance. In my previous bullish article in July 2024, I highlighted that I was too cautious about the company’s leading position in the AI growth inflection thesis. As a result, I’ve understated its custom AI chips opportunity while overstating its cyclical non-AI revenue prospects.

While AVGO has underperformed the S&P 500 (SP500) since my previous article, its bullish proposition has been assessed to remain intact. Therefore, the recent weakness in the stock has opened up another solid opportunity for investors to add more exposure.

In the third fiscal quarter earnings release last week, the market was palpably disappointed with its relatively tepid guidance. As a result, it sent AVGO into a tailspin, as investors likely took profit to protect their gains. Notwithstanding the near-term caution, I’ve not assessed a structural decline in the AI infrastructure thesis. Accordingly, the AI arms race involving big tech and the leading hyperscalers is expected to intensify, bolstering growth prospects for semiconductor leaders like Broadcom.

Should You Worry About Broadcom’s Tepid Guidance?

As a reminder, management indicated Broadcom attained AI revenue of $3.1B in FQ3 and guided to AI revenue of $3.5B for FQ4. However, the full-year AI revenue outlook of $12B (up from $11B previously) disappointed the market, potentially raising risks of a growth normalization phase from the next fiscal year.

Given Broadcom’s less enthusiastic guidance upgrade, the market is justified in reassessing its optimism on the AI growth momentum. It also follows Nvidia’s (NVDA) recent earnings, suggesting a lack of significant follow-through on their guidance upgrades from the leading semi-companies.

Despite that, the AI investment theme is alive and well. There’s a need to continue upgrading the AI infrastructure to ensure that leading tech companies stay ahead of the curve. However, I concur that software companies must demonstrate that they can monetize Generative AI effectively, lending credence to the AI investment thesis. Microsoft (MSFT) has reportedly faced challenges in improving the adoption of its AI co-pilot, potentially dampening investor optimism about its software peers. Hence, I assess that the market will likely remain cautious over a more aggressive valuation re-rating on AVGO until they garner more visibility from the leading software companies.

Notwithstanding the caution over AI growth opportunities, management anticipates an inflection on its non-AI revenue. Therefore, investors should continue to assess whether its non-AI bookings could translate to more revenue visibility over the next few quarters. Broadcom highlighted that non-AI bookings increased by 20% YoY. Therefore, it corroborates management’s confidence that its cyclical revenue segments have “passed the bottom.” That should afford investors more confidence as the company navigates the market’s caution on its AI revenue streams in networking and compute. I assess that the competitive advantages in Broadcom’s networking solutions should continue to underpin its ability to provide an integrated portfolio encompassing critical solutions across the AI value chain.

Is AVGO Stock A Buy, Sell, Or Hold?

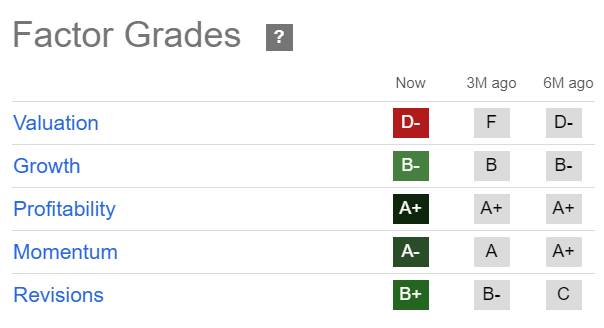

AVGO Quant Grades (Seeking Alpha)

AVGO is still priced for growth (“D-” valuation grade), even though it hasn’t improved markedly from the optimism observed three months ago (“F” valuation grade). However, its best-in-class profitability (“A+” profitability grade) underpins its robust buying momentum, suggesting a buy-the-dip opportunity remains intact.

AVGO’s forward adjusted PEG ratio of 1.46 is nearly 20% below its sector median, underscoring a relative undervaluation thesis. Wall Street estimates have also been lifted, potentially bolstering the buying sentiment on the stock.

Risks To AVGO Thesis

Investors are palpably concerned about whether the AI upcycle could be nearing its peak, potentially leading to a growth normalization phase for Broadcom. Investors must scrutinize the investment and monetization drivers closely, as they could determine the revenue trajectory of AVGO and its leading peers.

In addition, the stock is still priced for growth. While the company is confident its non-AI revenue segments have seen their worst, the recovery remains uncertain. If macroeconomic headwinds intensify, they could lengthen the recovery of the company’s more cyclical solutions, potentially impacting their earnings recovery.

Rating: Maintain Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Consider this article as supplementing your required research. Please always apply independent thinking. Note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Read the full article here