As my readers will know, I’m a big fan of founder-led companies. Tecnoglass has recently caught my interest as the company has grown revenue at a CAGR of over 15% for the last ten years. The company has also been reducing their debt, while growing free cash flow and currently pays a dividend to shareholders. Also impressively, Tecnoglass has a return on equity of over 25% and has recently been buying back their own outstanding shares.

Despite all the positives, I’m not completely sold on the company. I’ll explain why as I did into the details on this interesting small-cap founder-led organization.

The Company

Tecnoglass (NYSE:TGLS) is a global leader that manufactures, supplies and installs architectural glass as well as aluminum and vinyl windows for commercial and residential real estate. The company was founded in 1983 by the Daes brothers, Jose and Christian, both are still with the organization. Tecnoglass went public back in 2013, via a SPAC.

The company is located in Barranquilla, Columbia and has a 5.6 million square foot vertically integrated manufacturing complex that allows the firm to easily supply customers with Tecnoglass’s high-quality products. As of the company’s last 10K filing, Tecnoglass had over 1,000 customers, most of their business was coming from the United States.

The company’s mission is, “The transformation of glass using superior manufacturing technology.”

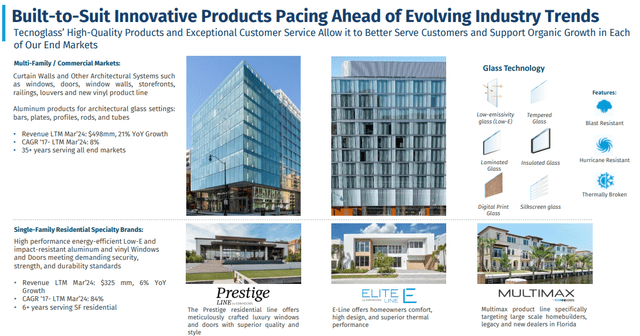

As you can see below, the company does have a nice variety of glass products for different residents and markets:

Investor Presentation

Additionally, many of these products are “green” and eco-friendly which has certainly become a focus of late for not only companies but for investors. Currently, 85% of Tecnoglass’s revenues are considered “green revenues” as they come from low emission and impact-resistant glass and windows which contribute to reducing global emissions.

Tecnoglass’s revenue comes from single family residential and multi-family/commercial housing. Over the last several years the company’s commercial side of the business has generated more revenue but both aspects of the business have been growing which I’ll discuss in more depth in the financial section.

Moat and Opportunity

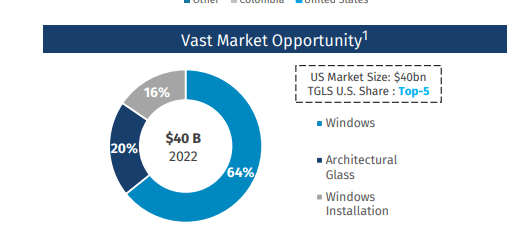

Tecnoglass believes they have a large market opportunity with a $40 billion market for windows, architectural glass and window installation as you can see below:

Investor Presentation

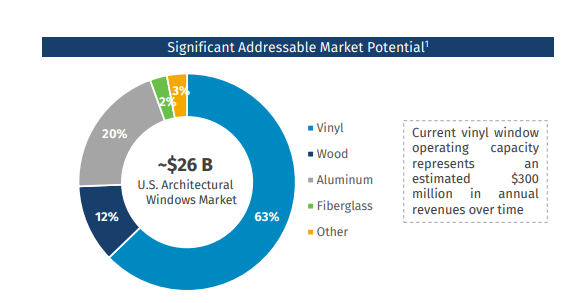

Furthermore, the company believes they have a recent significant market opportunity with vinyl windows as you can see below:

Investor Presentation

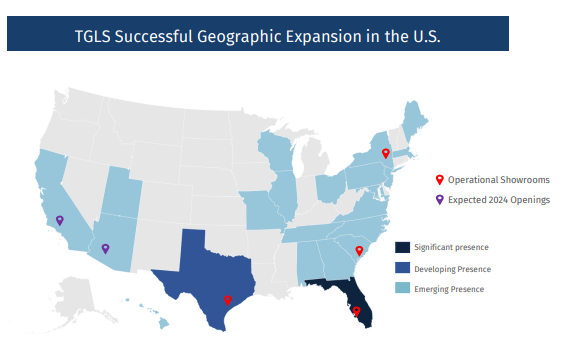

Tecnoglass must further penetrate the United States to continue to grow the business. As you can see below, the company has a significant presence in Florida, which accounted for 90% of the company’s U.S. revenue as of 12/31/2023:

Investor Presentation

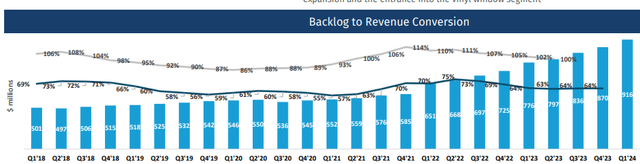

The company is growing their presence in Texas and various other coastal states. In order to grow revenue Tecnoglass must continue to be successful at converting their backlog into revenue. As you can see from the graphic below Tecnoglass has been very good at converting their backlog:

Investor Presentation

During the company’s latest earnings call, Christian Daes had this to say about the company’s current backlog, “We were pleased to report another record multi-year backlog of approximately $1 billion. Our backlog growth reflects an expanding pipeline of projects with visibility through 2025 and now building into 2026. This robust backlog represents 2.1 times our LTM multifamily commercial business, providing us with a multiyear view on the multifamily commercial portion of our revenues.”

The company believes they have numerous competitive advantage due to their vertical integration which helps the company create operational efficiencies and thus lower the costs for the business. Also, due to the company’s strategic location in Columbia, they are able to benefit from a wage perspective, yet this location is close enough to Miami that Tecnoglass can easily get their products to the United States.

Due to these factors and others such as high-quality employee training and experience in this industry Tecnoglass believes there are high barriers to entry in this market. I would agree with that assessment thus I feel Tecnoglass does have a moat.

Management

As noted earlier, Jose Daes co-founded Tencoglass with his younger brother Christian Daes. Jose is the CEO of the company and Christian is the company’s Chief Operating Officer. Both men are members of the company’s board of directors.

The company’s CFO is Santiago Giraldo who has been with Tecnoglass since 2016.

There are limited Glassdoor reviews for Tecnoglass so I don’t feel as though the Glassdoor ratings provide a good picture of life at Tecnoglass or working under the Daes brothers.

The Daes family certainly have an interest in the future success of Tecnoglass as according to the company’s most recent 10K filing, Energy Holding Corporation holds 52.4% of the outstanding ordinary shares. The Daes family own 100% of the shares of Energy Holding Corporation.

Financials

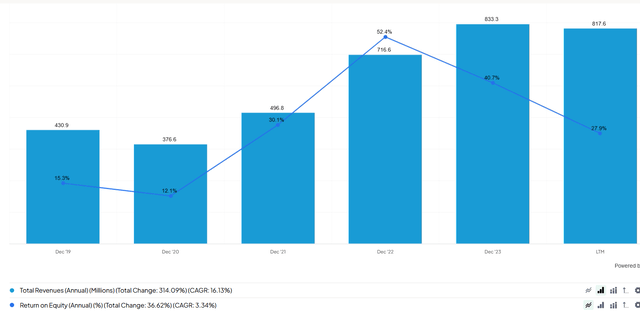

To start, taking a extended look at Tecnoglass’s revenue growth, you can see that the company has impressively grown revenue since 2019 at a CAGR of over 16%:

Finchat.io

Furthermore, return and equity (ROE) which I believe is a key metric which identifies how effectively management is using capital has grow since 2019 and is still impressively over 25% for the last twelve months.

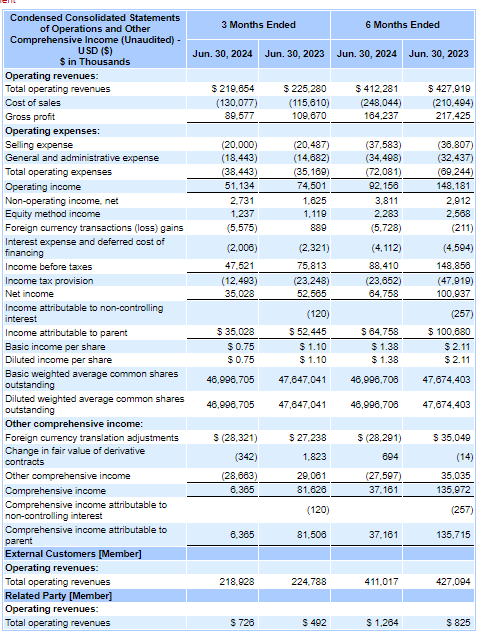

For the second quarter 2024, Tecnoglass brought in revenue of roughly $220 million which is a decrease of 2.5% compared to Q2 2024. Despite the decline, this was the company’s second highest revenue quarter in company history. Single family resident revenues accounted for roughly $96 million which is 10% higher than the $87 million recorded in Q2 2023. Roughly $124 million was generated from commercial revenue which is down compared to the $138 million in Q2 2023.

The company’s gross margin for the quarter was nearly 41% for the quarter which as you can clearly see below is not as good as the roughly 48% in the prior year second quarter:

SEC.gov

Management noted an unfavorable foreign currency impact caused this difference and as can see above from the foreign currency transactions (loss) gains line, has impacted operating margins as well as net income.

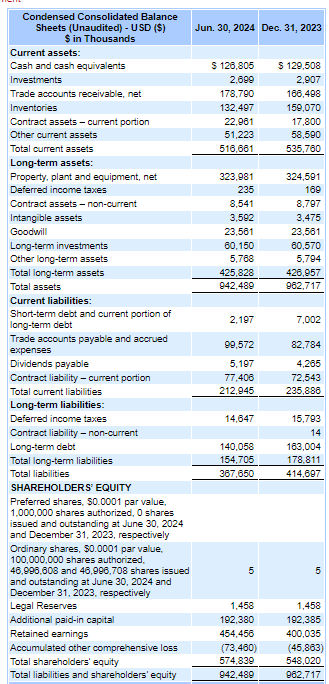

Tecnoglass has a healthy balance with more than enough current assets to cover the company’s current liabilities as you can see below:

SEC.gov

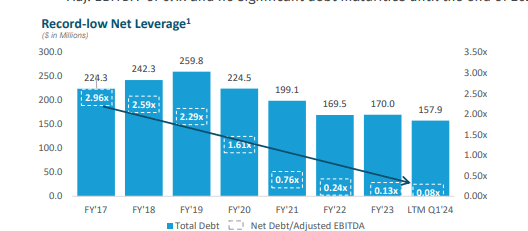

Although Tecnoglass does have some long-term debt they have done a great job of paying it down as you can see from the below graphic from a recent investor presentation:

Investor Presentation

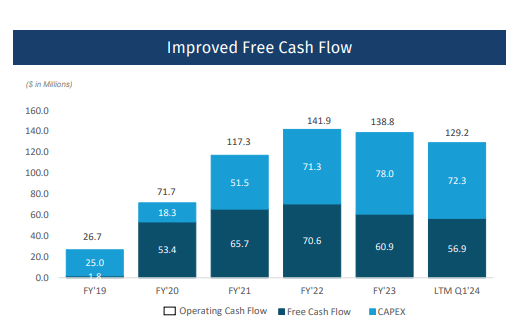

From a cash flow perspective, Tecnoglass had over $35 million of cash provided from operating activities and as you can see from the graphic below the company has done an excellent improving the company’s amount of free cash flow:

Investor Presentation

Risks

As I was researching Tecnoglass, I stumbled against a short report by Hindenburg Research. While Hindenburg’s analysis hasn’t always been completely accurate, some of the insights from Hindenburg have resulted in exposing frauds which led to criminal indictments.

This article was published in 2021. To highlight a few of the main points, Hindenburg stated, the Daes brothers had connections to the Colombian cocaine cartel, didn’t disclosed or lacked significant details with related parties, overstated revenue, and had numerous accounting issues. Interested investors can read the entire report here.

In term of accounting issues, I see no current issues as the company has received a clean audit opinion from PWC over the last few years nor has the company filed any amendment filings or restatements due to accounting issues or irregularities.

I also found an article that debunked most of these accusations, however the site seems to be Colombian based so it many also be bias.

Management also recently mentioned a review of strategic alternatives. The press release was rather vague about what was being reviewed and management provided no details on the company’s recent earnings call. These types of reviews can cause stock volatility and could certainly alter one’s investment thesis about the company should Tecnoglass’s board to directors decide to sell or perhaps make a material acquisition.

Valuation

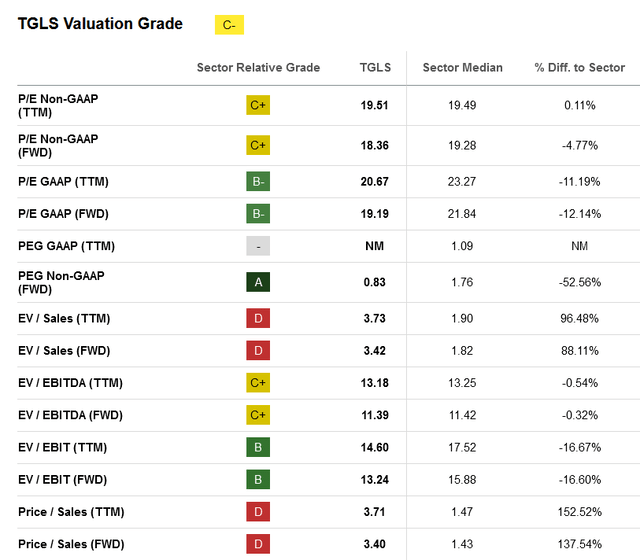

Tecnoglass has a current valuation grade of a “C-” at Seeking Alpha:

Seeking Alpha

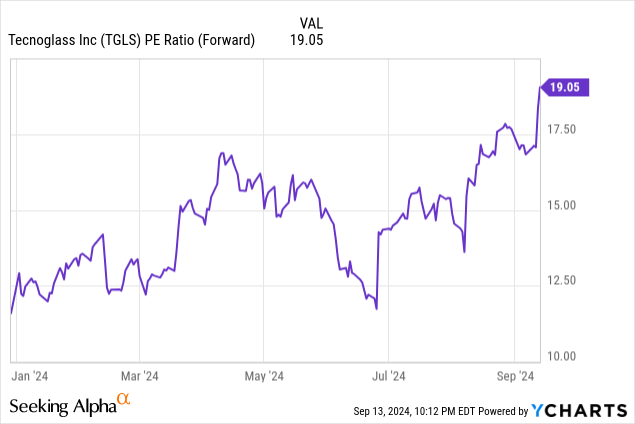

As Tecnoglass is profitable, I think P/E is a good metric to value this company. Although Tecnoglass’s forward P/E is slightly less than the section median, it’s trading at it’s highest level currently in 2024 as you can see below:

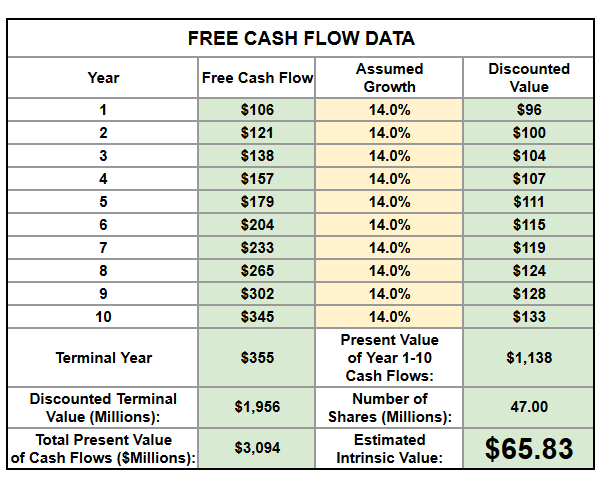

Looking at valuation from a different standpoint, using a reverse discounted cash flow model with a discounted rate of 10% and a terminal rate of 3% you would need future growth of over 14% to justify the current share price:

Arthur calculation

I think that’s somewhat of a stretch given most analysts aren’t expecting that double-digit growth in the upcoming years. I think growth below 10% is more reasonable, which would come to nearly $45 dollars a share in my model. Should the company’s stock price return to the values seen in June I’d be a more likely buyer.

Conclusion

I like that Tecnoglass is founder-led and it seems the Daes brothers have a large stake in the corporation thus are highly motivated.

Tecnoglass appears to leader in this niche market and given their strategic location and vertical integration have done a great job creating operational efficiencies that competitors likely can not easily duplicate.

The organization has stellar financials as revenues and free cash flow are increasing, debt is declining, and management is clearly very effective given their percentage of return on equity. Hindenburg Research may feel Tecnoglass’s figures are “too good” but given the amount of time that has passed since their report was published as well as lack of legal action taken against Tecnoglass or the Daes brothers, I’m inclined to think their findings might be exaggerated.

However, given the company’s current valuation is much higher than it’s been compared to earlier this year and the company’s internal strategic review, I’m not in a rush to add Tecnoglass to my portfolio. I plan to wait to see what, if anything, comes from the review then I’ll reevaluate the company’s valuation at that time.

Read the full article here