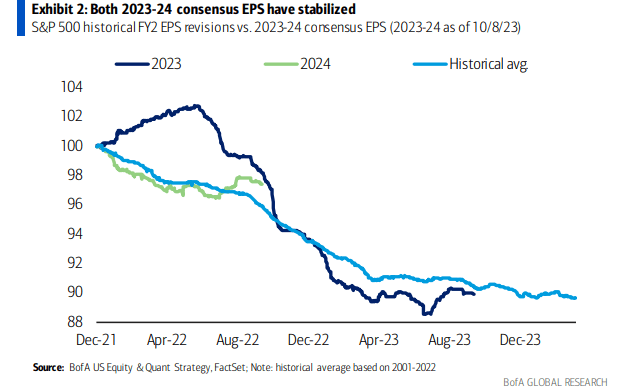

Q3 earnings season is off to a lukewarm start. The 73% EPS beat rate is in line with the historical average and aggregate earnings are verifying 6.6% ahead of expectations.

We will hear from more big names in the coming days with many tech titans reporting next week. AI will continue to be a hot theme, and firms simply mentioning artificial intelligence outperformed back in the Q2 reporting period. For now, though, AI infrastructure is in focus as demand runs hot. In all, SPX 2023-24 EPS estimates have flat-lined.

I have a hold rating on Arista Networks (NYSE:ANET), which reports next week. I see it near fair value while a few technical cracks may be emerging.

S&P 500 Earnings Estimates Hold Steady

BofA Global Research

According to Bank of America Global Research, Arista Networks develops high-performance cloud networking solutions, including switches, routers, and Wi-Fi software. The company’s low latency switches reduces networking costs for high-frequency trading platforms, large internet companies, and cloud service providers.

The California-based $58 billion market cap Communications Equipment industry company within the Information Technology sector trades at a high 34.4 trailing 12-month GAAP price-to-earnings ratio and does not pay a dividend. Ahead of earnings due out next week, shares trade with a high 55% implied volatility percentage, and short interest on the stock is low at just 1.1% as of October 20, 2023.

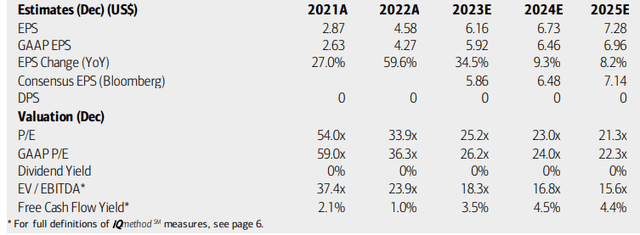

In late July, Arista reported a solid EPS beat. Per-share operating earnings verified at $1.58, topping the $1.44 consensus estimate. Sales were about in line with expectations at $1.46 billion, up 39% from the same quarter a year ago. Shares surged nearly 20% by the close after it reported results.

Along with the EPS beat, margins came in higher sequentially. Interestingly, the management team was somewhat cautious when looking ahead to Q4 this year and the first half of 2024 – it sees a dip in revenue growth from 25% YoY in 3Q23 to 11% in 4Q23, with sequential decreases in subsequent quarters. Still, its Enterprise and Tier-2 Cloud segments continued to perform well as margin strength persists.

Arista has been getting a lot of sellside attention as it presents at many industry conferences. In late August, Citi upgraded the name as an AI play, taking its price target to $221 from $177 on expectations that 400G cloud spend should recover into 2024.

Key risks include increased competition from other cloud providers, potentially leading to margin compression. Corporate ad spending could also ease should a broader macroeconomic slowdown take place – that was largely the reason for a downgrade of the stock by Piper Sandler earlier this month. So that’s something to monitor in its upcoming Q3 report. Arista has topped earnings estimates in each of the past 12 quarters, and YoY EPS growth is expected to come in close to +26% this time.

On valuation, analysts at BofA see earnings rising sharply this year before per-share profit growth moderates to a high-single-digit pace in the out year and 2025. The Bloomberg consensus estimate is about on par with what BofA projects – at last check, the 2024 EPS figure is $6.82 and 2025’s figure is $7.65, with increasing EPS estimates just recently.

Arista has positive free cash flow, but its FCF yield is low, and no dividends are expected to be paid on this fast grower. Earnings multiples in the low 30s today and an above-market EV/EBITDA ratio appears to the high side when considering EPS growth that may settle near 10% after 2023.

Arista: Earnings, Valuation, Free Cash Flow Forecasts

BofA Global Research

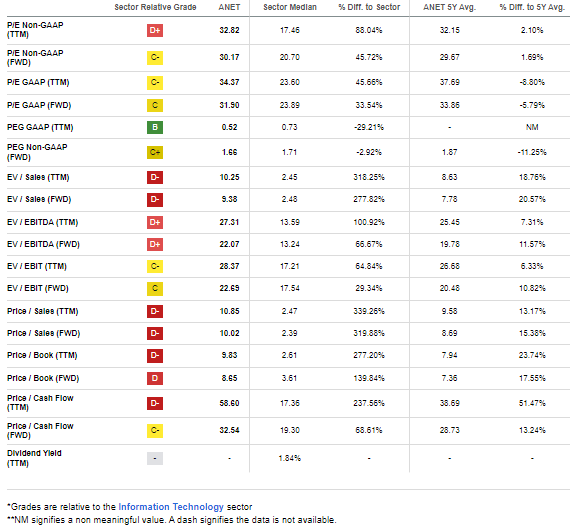

If we assume long-term EPS growth of 10% along with its current forward operating earnings multiple of 30.2, then the PEG ratio on the stock is slightly above 3. Thus, there is a considerable amount of optimism priced into the stock today. What’s more, sales-based valuation metrics show that ANET is to the expensive side when compared to the I.T. sector median and relative to its own history. A P/E ratio near 30, though, may be the right valuation when comparing Arista to higher-P/E software companies and lower-P/E networking/communications firms.

Neutral Valuation Metrics

Seeking Alpha

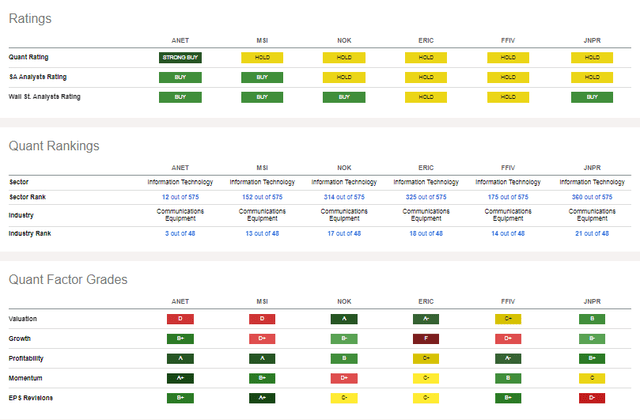

Compared to its peers, ANET features the most bullish analyst and Wall Street sentiment. Not surprising given the stock’s massive 2023 absolute and relative performances. The valuation is priced rich today, and about near full and fair value today, in my opinion.

Still, the growth outlook is strong and largely better than its competitors. ANET also features robust profitability trends, and recent EPS revisions have been very strong. Finally, stock price momentum has been stellar, though there is a near-term cautionary signal I spotted on the chart which I will detail later.

Competitor Analysis

Seeking Alpha

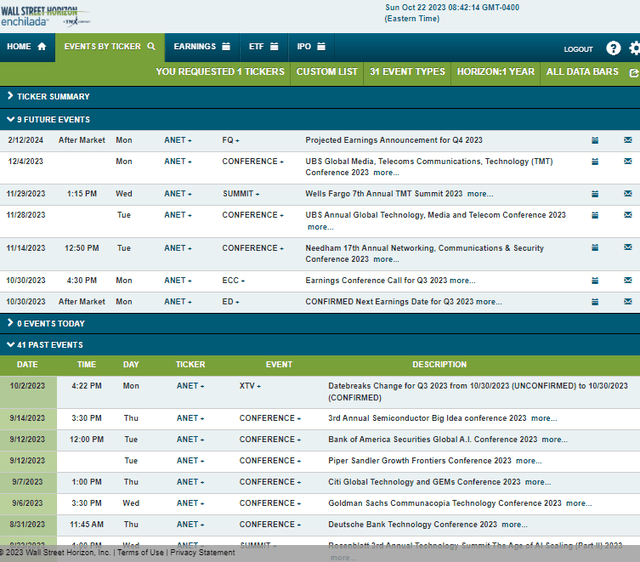

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q3 2023 earnings date of Monday, October 23 AMC with a conference call immediately after the numbers hit the tape. You can listen live here. The management team remains on the speaking circuit with conference presentations through early December that could also bring about share-price volatility.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

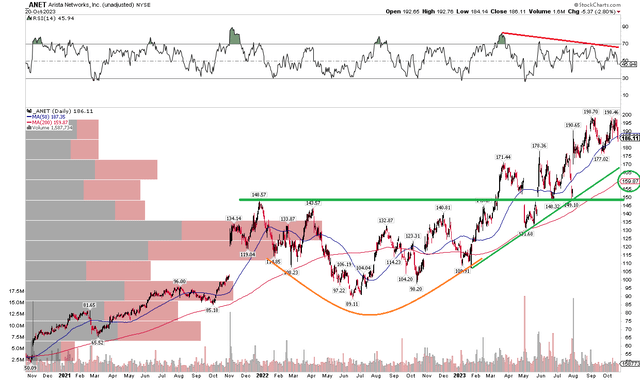

ANET has been a major winner this year. Notice in the chart below that shares are up more than 50% in 2023, and a strong uptrend remains in play. Following an upside breakout from a rounded bottom (which turned out to be a continuation pattern, not a reversal pattern), the bulls took ANET to fresh all-time highs just shy of $200 in early September. The stock has an uptrend support line off the January nadir around $107 and the long-term 200-day moving average is on the rise with shares holding that indicator line on a few occasions.

It is not all roses for ANET, however. Take a look at the RSI momentum indicator at the top of the graph – as the stock has notched higher highs, momentum has slowed. It’s often said that momentum changes before price, so this is something the bulls should acknowledge. Moreover, the $198 to $199 range could be a near-term bearish double top as the October rally lost steam last week. I see downside support between $177 and $178 with long-term support around $150. A possible upside target to $210 could still be in play based on the height of the rounded bottom pattern ($148 – $89).

Overall, the uptrend is clear, but momentum has waned, so I am cautious about where the stock could go over the weeks and months ahead.

ANET: RSI Deterioration, Near-Term Double Top In Play

Stockcharts.com

The Bottom Line

I have a hold rating on Arista. The fundamental earnings growth story is strong, but the valuation appears reflective of the sanguine outlook. Additionally, the technicals show some near-term weakness possible while a long-term uptrend is solid.

Read the full article here