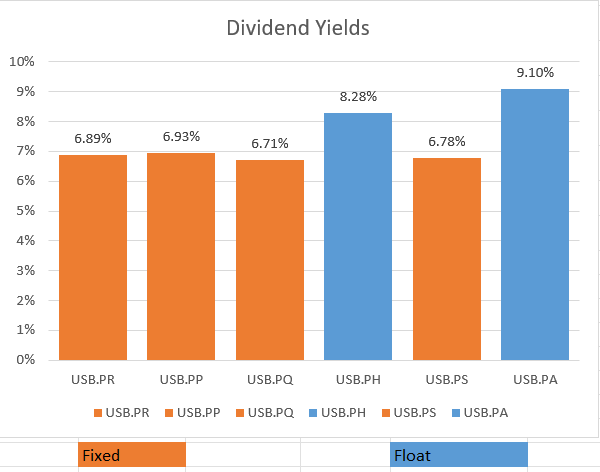

U.S. Bancorp (NYSE:USB) is one of the largest banks in the United States. Like many in its industry, the bank has a variety of preferred shares. Of the six issuances, two of them are paying dividends based on a floating interest rate. The Series A preferred share (NYSE:USB.PR.A) is on pace to pay a dividend yield of 9.1% over the next twelve months based on its most recent dividend declaration. Recently, after examining the bank’s third quarter financials, I purchased the bank’s series A preferred shares and I believe they are a good holding for income investors.

Yahoo Finance

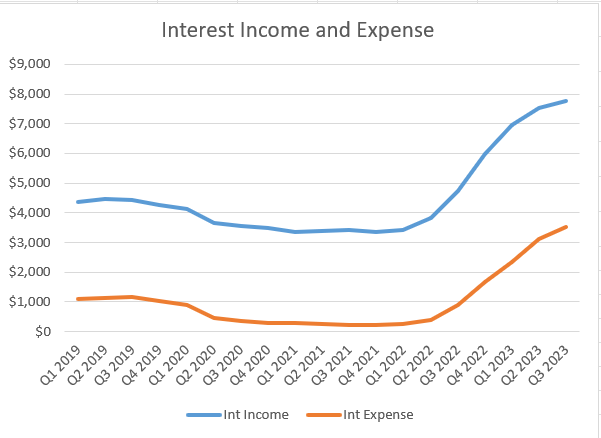

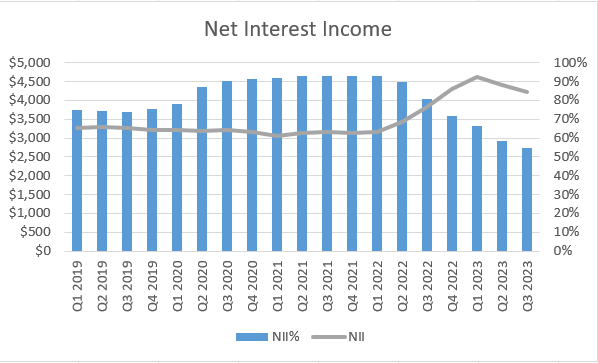

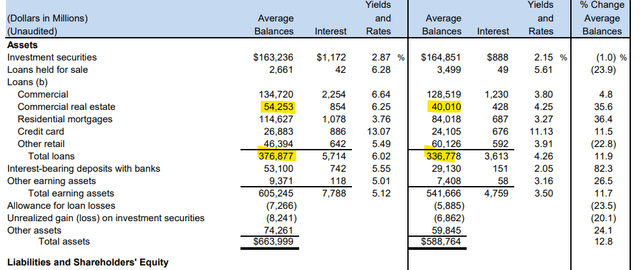

With the rise in interest rates, US Bank has seen as a rise in both interest income and interest expenses. Net interest income (interest income less interest expense) rose notably in 2022 and peaked in the first quarter of this year before declining for two consecutive quarters. Despite the erosion of net interest income, the levels remain above where they were prior to the pandemic.

Company Financials Company Financials

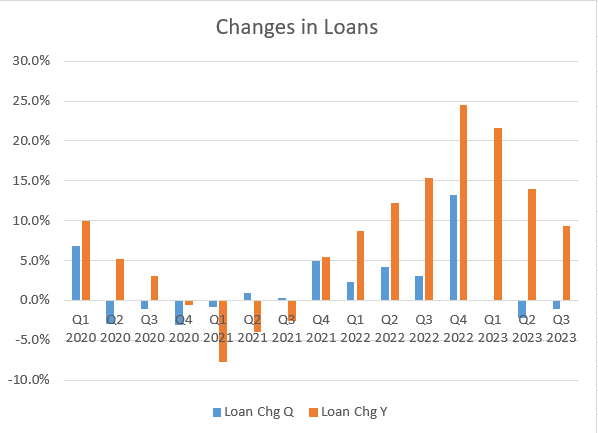

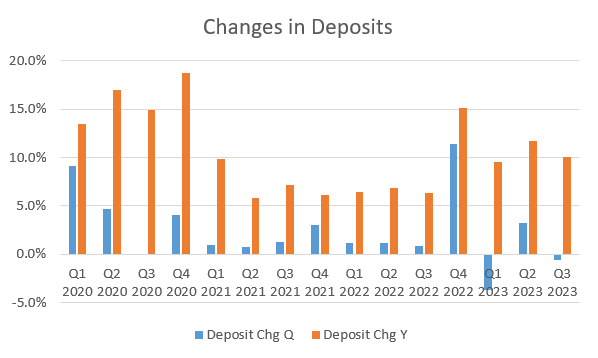

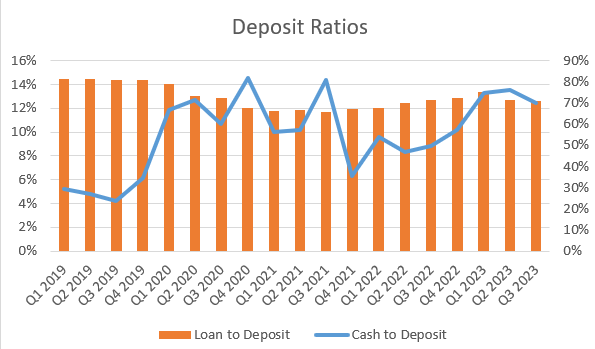

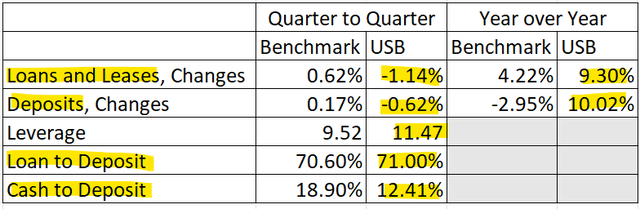

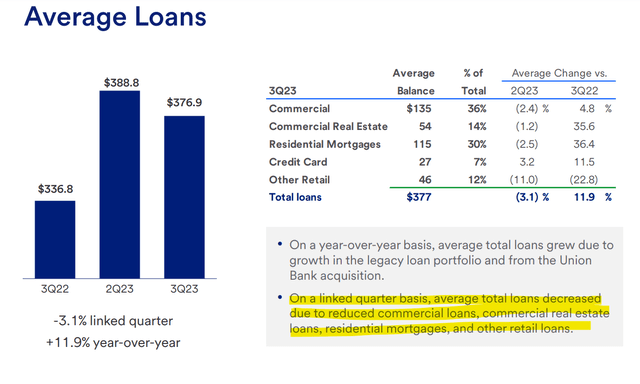

US Bank’s lending and deposit growth over the last four quarters has been influenced by the acquisition of Union Bank. Still, the bank saw a solid tick up in deposit growth during the second quarter, and a slight pullback in the third quarter. Lending growth by the bank has been much slower, in fact, negative across the last two quarters. These trends have led to a lower loan to deposit ratio, approaching 70%.

Company Financials Company Financials Company Financials

The Union Bank acquisition was also a contributing factor to an uncomfortable rise in leverage. Prior to the pandemic, leverage at US Bank was a conservative 8 to 1, rising to 9.5 to 1 during the pandemic, and peaking at 12 to 1 in the same quarter as the Union Bank acquisition. Leverage has since dropped by half a point into 2023 but remains above the peer average. Fortunately, the bank’s loan to deposit ratio and cash to deposit ratio is conservative enough where additional leverage should not be required with the existing operation.

Company Financials & Federal Reserve Data

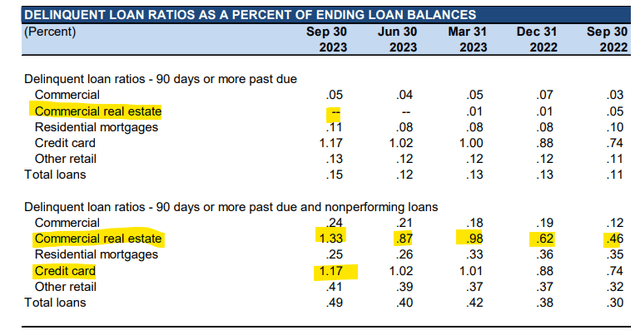

There is some concern regarding the bank’s exposure to commercial real estate (CRE). While the Union Bank acquisition increased the bank’s share of CRE compared to its total portfolio, the loan portfolio is only 14% exposed to the sector with its lending being much more prevalent in commercial and industrial along with residential mortgage sectors.

Company Financials

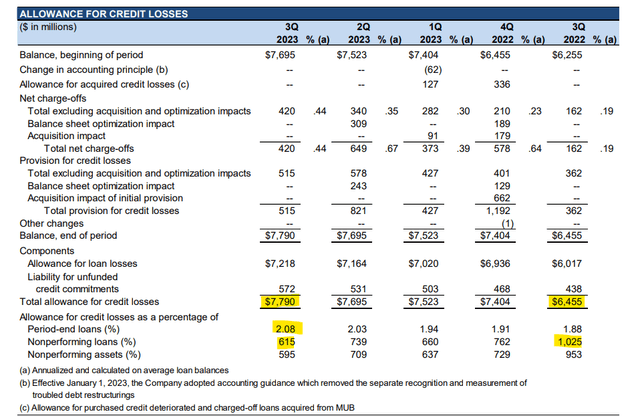

In the face of growing delinquencies across the industry, US bank has established an allowance for credit losses that currently covers its nonperforming loans by more than six times its current nonperforming balance. It is important to note that the bank is seeing a notable increase in delinquent loans that appears to not have peaked, but the allowance should cover it.

Earnings Release Earnings Release

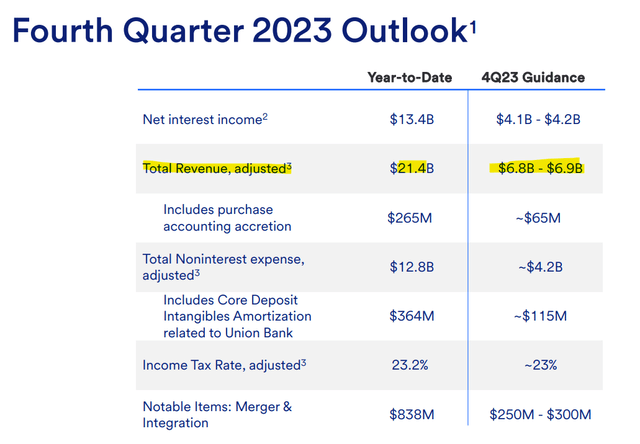

In terms of outlook, it appears as if US Bank is expecting loan growth to remain negative in the fourth quarter. This is because of the existing trend of loan decline across most types of loans and the bank’s projection of fourth quarter revenue below the quarterly trend achieved in the first three quarters of 2023. US Bank should be collecting cash on performing loans and either building its cash position, building its securities portfolio, or reducing leverage.

Earnings Presentation Earnings Presentation

In any case, US Bank is nowhere near suspending its preferred share dividends. In terms of call risk, the Series A preferred shares have been floating since 2011 and even if the shares were called, they are currently trading at 74% of call value and would represent a sizable return for shareholders. The shares are subject to lower income should interest rates drop, but historically lower rates have meant higher share prices, giving investors a good opportunity for capital appreciation. Overall, investors are hard pressed to find a bank the size of US Bank with a preferred share yielding over 9%. The Series A preferred is a good place to invest while waiting for higher interest rates to abate.

Read the full article here