It has been a foundational thesis that narratives while intangible are a powerful and very real mover of stock prices

Because it is an intangible the waxing and waning of a narrative can fluctuate prices in either direction. The more cognizant of that pattern the more able you will be to counteract downward pressure and smooth out returns

I have one point major I want to make about the above. It is human nature to detect cause and effect when multiple events coincide. Meaning tech stocks are falling so it must mean that AI is overhyped and the stocks are all overvalued. Yet for the most part ALL stocks have been falling this week because of interest rate volatility. Is AI overhyped? Short-term very likely, long-term, it is likely not. The stock market is really a dialectic, a constant debate between the skeptics and the dreamers. Somewhere in the middle is the truth.

Extending this thought process to GLP-1 injectables like Wegovy, Mounjaro, and Ozempic has a narrative that is very disruptive to the valuation of a wide range of sectors. It was because of very recent news of a clinical trial leveled at children aged 6 who are obese that I was reminded of the “Jump the Shark” metaphor. It was as if the GLP-1 narrative had a mind of its own and sensing the market’s ennui that it had to go to the extreme to get attention. In case you’ve never heard of this idiom, according to the Urban Dictionary, something is said to have “jumped the shark” when it has reached its peak and begun a downhill slide to mediocrity or oblivion. It was originally meant to describe TV shows of a bygone era, though I feel like it is apropos here somehow. To my mind, a young child who is so obese that doctors feel okay to prescribe a regular injection is beyond the pale, Either this kid is a victim of child neglect or this doctor forgot the Hippocratic oath. Tell the parents either they ban the XBOX, and the Twinkies or they are calling child services. I think both Eli Lilly (LLY) which hasn’t gotten approval for Mounjaro as a diet drug, and Novo Nordisk (NVO) may have sensed that this green field opportunity has its limits. That is why we hear that GLP-1 might dampen other cravings like drinking, gambling, cigarettes, will to live, etc. They also can cure heart and kidney disease. All these are real indications except the will to live, and we come to dosing little kids like that is okay. What does that do for the central nervous system of a growing brain? This is a step too far sorry, I know we have veered away from the topic of stocks, but in a way, we haven’t. We may be at peak GLP-1, well not totally peak first Mounjaro should be approved any day now, and then we deal with Shark Jumping

What does this all mean for stocks?

Ok now let me climb down from the soapbox, there is a warning here for traders and investors, not just parents. Both of these narratives have captured the imagination of market participants. As I expressed this notion of dialectic, characterizes the debate between bull and bear if you will. The assertion of the bull has primacy until counterarguments by the bears gain currency. This can go back and forth for weeks, months, and years. This is not so for television shows, generally when their “Shark is Jumped” it is curtains for the show. What I am trying to say here is that while it appears that GLP-1 is about to wane in influence on sectors like snacks, and MedTech, I fully expect it to reinvigorate the bears again at another point. I believe that pushing injections on veritable toddlers does herald a coming rethink of the limits of GLP-1. So let’s start with MedTech we are seeing some bounce-back on names like DexCom (DXCM) which was literally cut in half, another Medtech I like Shockwave (SWAV) has also recovered a bit, so has Stryker (SYK). Each one of these names has been devastated by the idea that once 70M Americans are shooting up Mounjaro or Wegovy, the need for new knees, a device that counteracts arterial sclerosis, or a continuous glucose monitor will no longer be able to grow in profits and revenue. Never mind that in the case of DXCM, type 1 diabetes is not helped by these drugs. Or that every type 2 diabetic might not qualify for these drugs, or that “pre-diabetics” a demographic that doesn’t yet use CGM might find it wise to use it to control their glucose. SYK is actually a paradoxical case since many people who need knee or hip replacement are too heavy to safely get them. They may first get on a Wegovy, and then get the knees. How’s that for irony? So when I say GLP-1 has jumped the shark this is what I mean. That should also work for the likes of PepsiCo (PEP) or Mondelez (MDLZ), and since I mentioned Twinkies (TWNK) earlier, let’s throw in The J. M. Smucker Company (SJM) which is overpaying for it in an acquisition. Not all people who are obese are going to give up their Chips Ahoy, Cheese Doodles, or Doritos, there are also millions of people who give in to snacks who aren’t morbidly obese. Maybe they are marathoners who indulge in a treat now and then. Yeah, the bull case for snacks being the reliable grower it once was is a bit more difficult than a purveyor of knees. At some point, even these names will bounce. I would likely want to get on the short side if they approach old highs though.

Now what about AI?

We’ve seen some strong AI performers on the back foot. The newest name in retreat is Oracle (ORCL). Executives at an ORCL investor event shared that they don’t expect significant revenue from their AI and close collaboration with NVIDIA (NVDA) for 2023, and some part of 2024. I am not sure how they isolate the branding they now have through that partnership and the fact that they are growing quite fast right now. In fact, ORCL has a lot of defenders after this statement. ORCL still has an average price target of $129.92, implying more than 27% upside potential. Still, ORCL fell 6% on Friday, not a super confidence builder and it reflects poorly on NVDA. I make much of narrative but price action affects sentiment as well. It could be the tail wagging the dog so to speak but AI is being reassessed as the tsunami of change. In this case, I believe the culprit is the historically high volatility in interest rates moving to the upside.

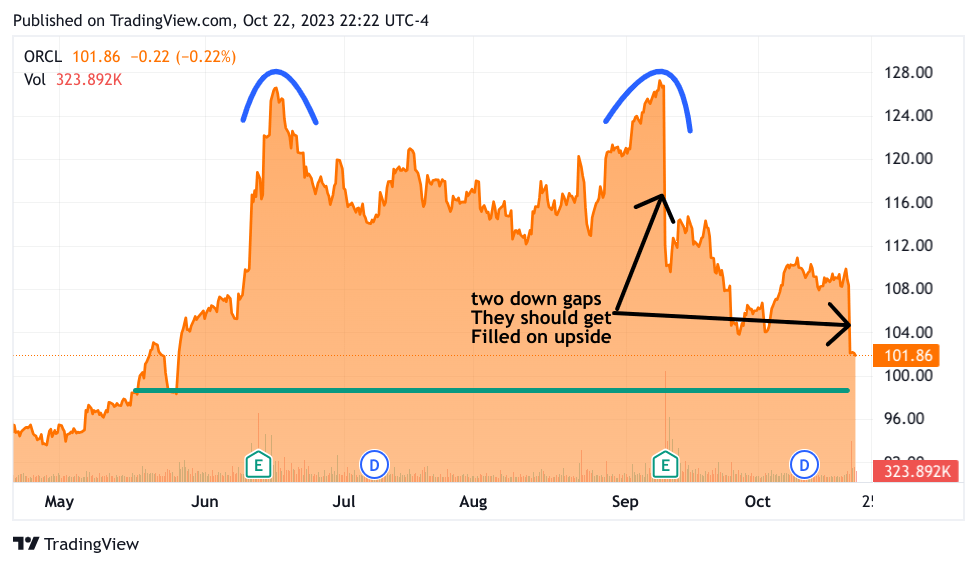

Right now it might seem that AI is overextended on the hype cycle but AI is real and it is already disrupting the enterprise. Let’s take a look at the charts of ORCL and see if it has further to fall…

TradingView

ORCL has fallen quite a lot, and the bears will note that we have a strong double top. However, I think we have fallen quite enough to satisfy this formation. I do like these down gaps that could portend a nice recovery. The green horizontal line is only 3 points below Friday’s close. I am pretty comfortable being in this stock and the call option.

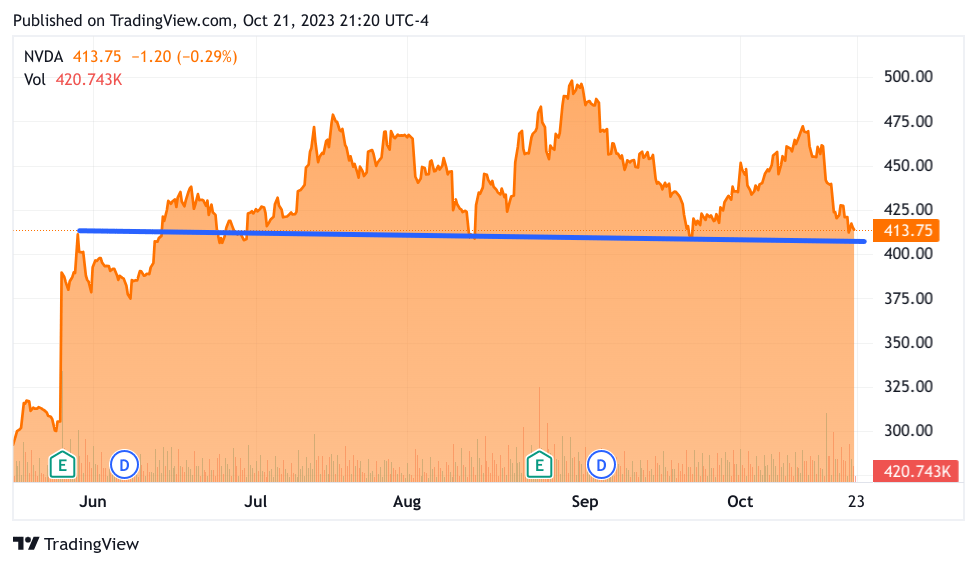

Bears have been singling out NVDA as primed for a fall but it is in a similar vein right now. Check out its 6-month chart as well.

TradingView

Looks like a lot of support to me, though if it breaks under 400 there might be a lot further to go in retreat.

I am maintaining both equity and call options in these 2 names. As far as the Medtech names, I added to my DXCM position in equity in my long-term investment account. I don’t own SYK but I think it makes sense to start a long-term investment in this name.

I can’t step away without a few words about the macroenvironment.

Geopolitically it could get a bit more crispy, at least until the ground war starts. Once that happens I believe the market will focus on more mundane matters like interest rates. I think the 10-year “touched the stove” so to speak and could significantly retreat from here. I also thought that 3.887% was going to hold onto the top for a while longer. I will say that that was a wrong assumption. That doesn’t mean that I have to change my stance and now expect the 10-year bond to get to 5.50% immediately or some such level. I do admit that the credit market is not my strong suit and other than the fact that this kind of volatility is quite rare. The 10-year bond should take a rest. That will re-ignite technology stocks and AI will once again be in the domain of the bulls.

Read the full article here