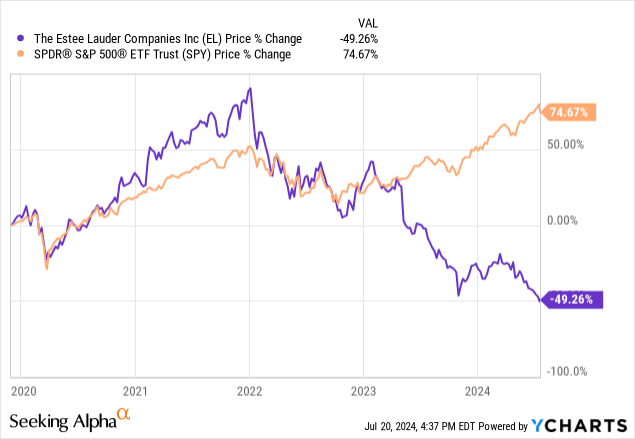

Estee Lauder (NYSE:EL), one of the pioneer companies in the cosmetics industry, has seen its stock get hammered by more than 70% since its all-time highs by the end of 2021 and close to 30% since its recent highs in March 2022. Despite this massive underperformance compared to the S&P 500, which is up more than 15% year-to-date, Estee Lauder might now be a clear buy since its business fundamentals have begun to find a solid bottom.

Estee Lauder’s nature is not a flawless business

Following the company’s most recent 10K, EL is one of the biggest cosmetics participants in the world. Their products include powerful brands like Clinique, Estee Lauder, MAC, Tom Ford, and LaMer, amongst many others, and are sold in over 150 countries.

Additionally, the company can be considered a legacy company due to its main distribution channels, which are physically in retailers trying to provide what is called High-Touch services instead of the more digital approaches like those used by high-growth companies like e.l.f. Beauty (ELF). These High-Touch services are basically a form of cosmetics advisory to catch clients in brick-and-mortar stores, which adds a sense of prestige and support from the brand to the potential client.

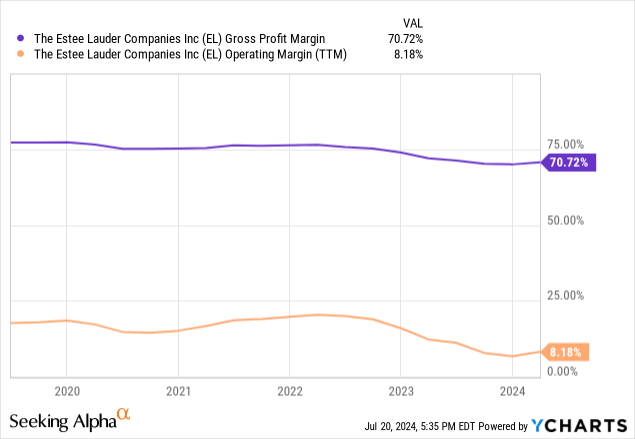

Another important characteristic of the EL business model is that the manufacturing facilities are located in expensive operational places, such as the US, the UK, Switzerland, Belgium, and Canada. This does not help the company’s operating margins, as the current Q3 2024 earnings report indicates that the company has a very good gross margin of around 72% but a terrible operating income margin of around 11%, meaning that operating expenses weigh around 60% of EL revenues. In my view, that is an awful way of optimization, especially when trying to keep margins afloat in a complex economic environment.

From a balance sheet standpoint, Estee Lauder is also quite apart from being flawless. With a long-term debt of $7 billion, increased by $2 billion from 2022 due to the Tom Ford’s acquisition, with maybe around $2 billion in free cash flows by the end of 2026, and paying dividends of around a billion a year, it seems relatively uncomfortable to reinvest in growth or to buy back shares in the mid term. Fortunately, current assets are sitting nicely over $3 billion higher than current liabilities, and the company is far from running out of liquidity. Dividends seem safe for now.

Why has Estee Lauder fallen so much?

There are quite a few specific reasons why Estee Lauder stock has had such a hard downfall. Still, in my opinion, all can be condensed into a management that was dazzled by immediate post-pandemic amazing results and then got shocked by heavy stagnation and disappointing margins after having to fight inflation and increased operating expenses.

Additionally, according to Reuters, Estee Lauder’s pre-pandemic revenues from Chinese customers were from traveling customers, who were quite diminished because of the long lockdown restrictions that took place in China up until the beginning of 2023.

Furthermore, the Chinese authorities have also begun a hard crackdown on the smuggling activity called Daigou, which consists of Chinese travelers buying cheap products worldwide and re-selling them when they get back to China at discounted prices. Without these revenues, it has been quite difficult for Estee Lauder to rebound its margins back to the immediate post-pandemic period, while also having a hard time re-encountering revenue growth.

This meant, in my opinion, that EL saw a severe contraction due to continuous growth expectations that were not realized. Having grown from around $5 in EPS by the end of 2019 to $8 by the beginning of 2022, it just fell apart after that, down to the current $1.78, dragging down the stock too from $370 to the current $100s.

Why have margins collapsed?

The main reason EL’s margins have collapsed is the nature of its business model. This, combined with inflation pressures, made it more difficult to keep gross margins at around 76% and had to come down to the current 70.7%.

Additionally, operating margins have collapsed from around 16% in 2019 to the current 8.2%. This happened because of some reasons like a really high operating expenses infrastructure due to having to pay production in costly developed countries, like Canada, Belgium, or the UK, while also having to pay relatively expensive selling channels like advisory in brick-and-mortar retailers and then the Chinese crackdown on duty-free smuggling.

What is the recovery plan?

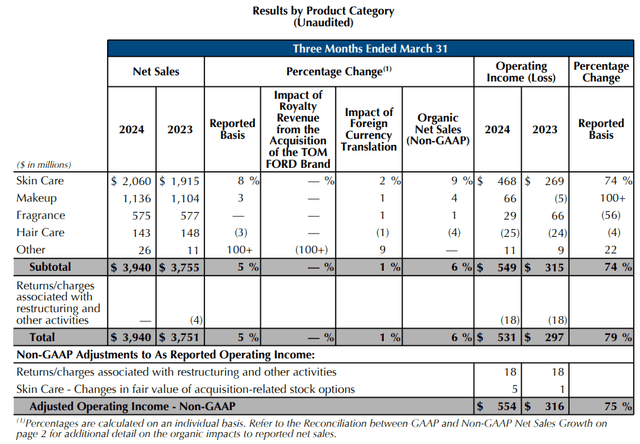

For the company to get back on the rails, in my opinion, at least three things have to happen. First, inflationary pressures have to give up. Fortunately, this might be the case as time goes on. For more details, check out this good article on the inflation situation. Second, the stock has to come back to growth or at least stop losing revenues. This also might be the case following the most recent Q3 2024 earnings report, where the company is finally seeing organic net sales growth, especially in the skincare category, which is the biggest source of revenue by a mile. Unfortunately, the Hair Care category is still not seeing growth, but this segment is relatively immaterial for the company as it represents less than 3% of revenues.

Estee Lauder Operating Income (Estee Lauder Q3 2024 Earnings Report)

The third, but maybe the most important factor to ensure the company is back on track, and even more significant, to ensure the stock might finally find a bottom and even some important growth, is the margin recovery. The management has expressed, in its most recent earnings call, its intentions to raise operating profit by $1.1 billion to $1.4 billion by the end of fiscal year 2026, or around August 2026. This could translate into around $1 billion in net earnings by that date, which is, in my opinion, the correct final sign that we have reached the bottom we were looking for in the stock.

Valuation

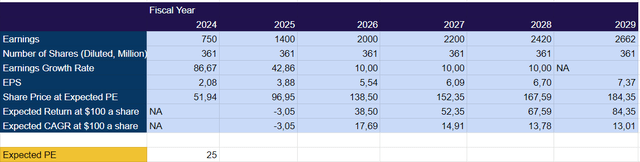

Currently, I consider Estee Lauder to be undervalued, if the management is able to execute correctly the margin recovery discussed earlier. While the current PE ratio might be considered quite high, at close to 50, it is better to take into account the future numbers for EPS instead. For that, I think that if management opex reduction is successful and revenue growth continues at 6%, the stock might be able to see an EPS of 5.54 by the end of fiscal year 2026, or close to August 2026. I am also not considering Estee Lauder buying back stock or even adding dividends to the returns, which might increase the performance of this investment. In this model, I also project an EPS growth of 10%, which I think is achievable if the company manages to grow revenues at 6%.

Image created by the author based on 10K projections (Author)

The model suggests that EL stock might give a solid return of around 15% for the next three years. I believe this is extremely valuable because this investment has a wide margin of safety, as it is already heavily discounted by more than 70% from all-time highs. Additionally, compared to the recent big gains in the SP500, I think continuous big performance on the big index might be difficult to sustain in the near future, while EL, at this price, can be a very good instrument to have exposure in a well-rounded portfolio.

Some risks

As I mentioned, I think there are at least three core components that have to be solved before the stock might be considered safe to invest. Excluding obvious big geopolitical risks with China that could heavily disrupt Estee Lauder’s revenue sources in Asia, the risks might be associated with a stickier or even resurging inflation, an even more challenging economic environment that makes it difficult for EL to get growth again, more specifically in America, and the operational risk that the management could not reach the goals at cutting operating expenses quickly enough. Any of these factors not achieved could conduce to a poor performance in the stock.

Conclusion

Estee Lauder is not a perfect company, far from it, but at this compelling stock price, with management that, in my view, is doing the necessary to redirect the company’s profitability, the company might be worth a chance in a well-diversified portfolio, before it is too late.

The brands have demonstrated to be strong enough, competition while high, still manageable, and mainly, a good stock price make of this a decent buy here.

Read the full article here