Airlines provide for tricky investments due to the highly dynamic nature with swings in demand and cost structure. For more than a year, the airline industry has been able to recover financial results rather quickly driven by labor and airplane shortages which prevented unbridles capacity expansion and provided solid topline growth. The reality for many airlines and mostly the airlines which focus on short-haul flights is that the recovery phase is nearing completion, and while unit revenues still stand strong, there is little to no growth while costs are mounting as new labor costs and higher fuel prices provide a higher cost basis.

As the industry is a rather dynamic one, we also see quick reaction to news items on air fares as well as oil prices, which causes swing in stock prices.

The Buy Rating Is Not Paying Off

In November 2022, I marked shares of easyJet (OTCQX:EJTTF) (OTCQX:ESYJY) a Hold and back then I saw no particular reason to buy the stock. However, since that Hold rating in November the stock climbed nearly 15% compared to a >10% gain for the broader markets. In January, I saw better signs validating a buy rating for the stock but since then the stock lost nearly a quarter of its value. In hindsight, it looks like I was too late upgrading the stock to buy and that is the continuous risk with any investment. Sometimes waiting for buy signs to flash strongly or any market change to be reflected in results leaves you a step or two behind on the actual stock price performance.

A Strong End Of The Year For easyJet

easyJet

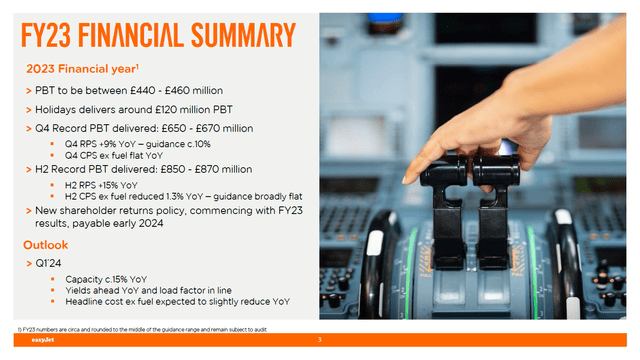

While there are some pressures, the preliminary results for easyJet show the company had a strong second half of the year with unit revenues growing 15% and ex-fuel unit costs dropping by 1.3% which was ahead of expectations for a full year pre-tax profit of £440 million to £460 million. For Q1’24, the company will be adding 15% capacity with further growth in unit revenues while unit costs excluding fuel will drop slightly. So, while there are concerns on sustained strength in unit revenues, we see that easyJet is guiding for it. Perhaps, the unfortunate element is that unit cost reductions are in no way in line with capacity increases so we continue to see that capacity reductions are not used to significantly reduce unit costs as airline envisioned but to keep the unit costs stable. At some point, the airline industry has to start looking what it will do with the higher cost basis. Will flying be made more expensive permanently or will the airline take the earliest reduction in air fares to restructure its costs?

A Buy, Hold Or Sell For easyJet Stock?

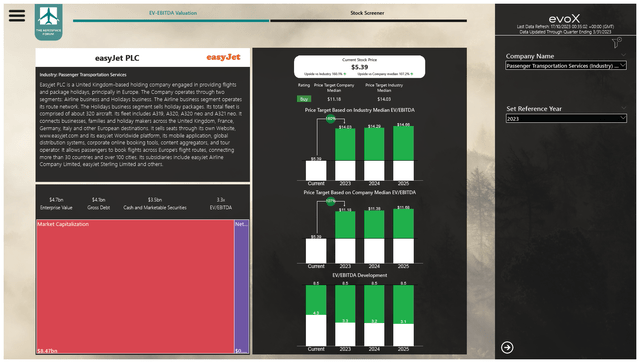

easyJet stock price valuation (The Aerospace Forum)

Since the stock has tanked 10% since providing its FY23 trading update, it is also a good time to revisit my rating on the stock, where I will also be implementing the new dividend distribution envisioned by easyJet which calls for 2023 dividends to be 10% of the after-tax earnings to be paid in 2024 and 2024 dividends to be 20% of the after-tax earnings. What we do see is that currently easyJet is significantly undervalued compared to the industry as well as its median EV/EBITDA. An improvement in results as well as an expansion towards historical EV/EBITDA multiples provides doubling potential for easyJet stock price.

Conclusion: easyJet Stock Is Significantly Undervalued

When I started writing this report, I expected that I should be lowering the price target for easyJet and revising my rating downward. The opposite, however, is true as parsing the number shows a $0.37 higher target of $11.18. So, I am maintaining my buy rating with the notion that upside might not materialize due to the fear that is encapsulated in airline investors and sudden swings in cost and revenue dynamics that might increase that fear even if the underlying performance is solid.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

If you want full access to all our reports, data and investing ideas, join The Aerospace Forum, the #1 aerospace, defense and airline investment research service on Seeking Alpha, with access to evoX Data Analytics, our in-house developed data analytics platform.

Read the full article here