Introduction & Investment Thesis

Okta (NASDAQ:OKTA) is a cloud-based identity and access management company that has underperformed the S&P 500 and Nasdaq 100 YTD. I had last written about the company on April 23 and had rated the stock a “buy”. My thesis was predicated on my belief that the company should be able to reignite growth back into the business as it realigns its sales team and leverages its partner ecosystem to drive customer acquisition and expansion efforts, along with reinforcing the security of their access management platform by building out customer best practices and launching new products. Since the time of my writing, the stock has remained flat, underperforming the S&P 500.

The company reported its Q1 FY25 earnings on May 29, where revenue and earnings grew 19% and 270% YoY, respectively, beating expectations. The company saw success in driving large deals, particularly in the public sector, while customers with $100K+ in Average Contract Value (“ACV”) grew 11.5% YoY to 4550 customers. One of the things that stood out to me was that its Current Remaining Performance Obligations (“cRPO”) exceeded management’s expectation, growing 15% YoY vs. 13% expectation, indicating that the company’s renewed go-to-market strategies are starting to bear fruit.

Assessing both the “good” and the “bad,” I believe that Okta is attractively priced to drive substantial returns over a 3-year investment horizon, thus making it a “buy.” Although it faces competitive pressures from large companies with extensive resources at their disposal, I am encouraged by the results so far in the company’s success in moving upmarket while unlocking operating leverage at the same time.

The good: Customers with $100K+ in ACV continue to grow while profitability expands

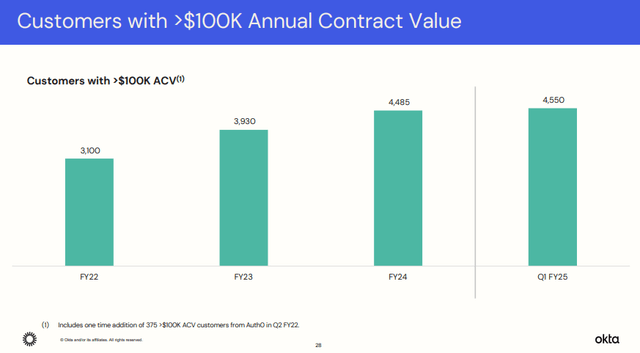

Okta reported its Q1 FY25 earnings, where revenue grew 19% YoY to $617M, driven by strength in winning large customers, particularly in the public sector, while customers with $1M+ in ACV are the fastest growing cohort. During the quarter, the company added 150 new customers, bringing the total customer count to 19,100 growing, while customers with $100K+ in ACV grew 1.4% sequentially and 11.5% YoY to 4550 customers, indicating that it is able to drive expansion of its solution suite within its existing customer base as it aims to reignite growth as part of its strategic initiative.

Q1 FY25 Earnings Slides: Momentum in customers with $100K+ in ACV

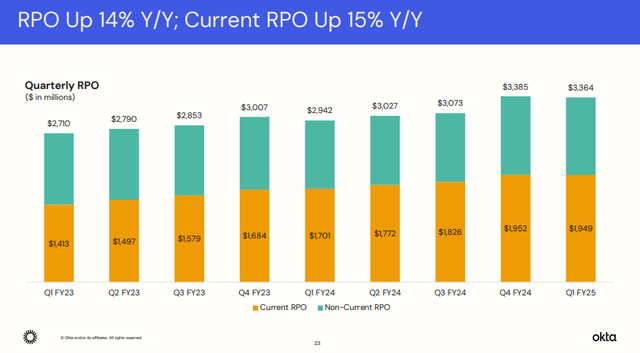

In the previous post, I wrote about how the company is redesigning its sales team by assigning two separate teams of account executives, one that focuses on customer acquisition and the other that focuses on driving upsells. In addition to that, I also wrote about how Okta plans to leverage its partner ecosystem to drive some of the largest deals by introducing their partner framework called Elevate to better align partner incentives to the total value they deliver to Okta. I believe the approach is yielding initial results as cRPO grew 15% YoY, better than the management’s expectation of 13% YoY growth. cRPO is a leading indicator of future Subscription Revenue which consists of 1) new customer bookings, 2) upsells, and 3) renewals.

Q1 FY25 Earnings Slides: cRPO growth exceeded expectations

In terms of their commitment to security and product innovation, the company had launched an initiative called Okta Security Identity Commitment after the security breach that the company faced in October 2023 to fortify their corporate systems, strengthen their products and services, and build out extensive customer best practices so that their customers can be highly protected. During the earnings call, the management outlined that the company is continuing to make progress while enhancing their customer policies to ensure that their products are deployed with Okta’s best security practices. Plus, the company also introduced a new product called Identity Security Posture at their 2024 Okta Showcase Event that they have started rolling out to select customers in North America, which will proactively identify vulnerabilities and security gaps, thus bringing a multilayered defense strategy on top of the workforce identity cloud.

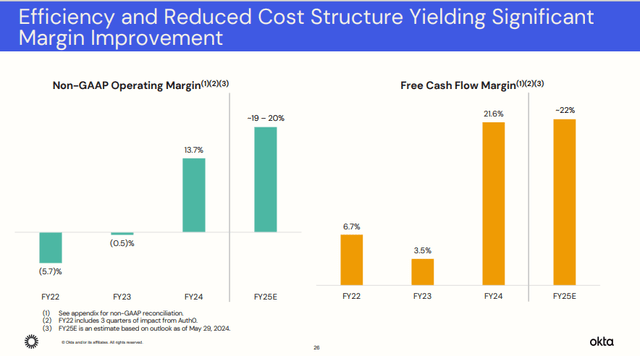

Shifting gears to profitability, the company generated $133M in non-GAAP operating income, which grew 270% YoY with a margin of 22%, an improvement of 1500 basis points from the previous year. As part of Okta’s initiative to position it for long-term profitability, it has been driving efficiencies in cost structure where it was able to keep its R&D expenses anchored on a GAAP basis while reducing its sales & marketing spend by 7.8% YoY. To me, this suggests that the management has shifted its focus from “growth at all costs” to “profitable growth” as it leverages its sales and partner ecosystem to target high ACV deals, thus unlocking operating leverage in the process.

Q1 FY25 Earnings Slides: Growing profitability from streamlining OpEx

The bad: Stagnating R&D spend may hurt innovation, especially given the competitive landscape and vendor consolidation

While I like Okta’s success in moving upmarket is enabling it to land larger customers while unlocking profitability as it pushes towards becoming a $5B company, the competitive landscape from behemoths such as Microsoft (MSFT), IBM (IBM), and Oracle (ORCL) cannot be ignored, as they possess larger resources at hand to bundle solutions across their customer base. Plus, in an environment where businesses are looking to consolidate across integrated platforms in order to gain pricing advantage and operational efficiencies, it may make it hard for Okta to compete at scale against larger competitors, especially if it falls behind on its R&D to fuel innovation. However, I would like to note that an improving picture for cRPO along with stabilizing Net Retention rate (“NRR”) at 111% is a positive sign that it is able to win net new customers and drive adoption of its solution set while improving on its cost of acquisition.

Revisiting my valuation: Okta is attractively priced

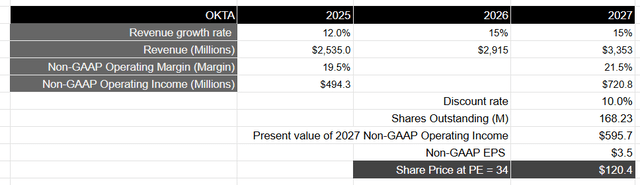

Looking forward, the management has raised its revenue guidance from its previous 10.5% growth projection to 12% for FY25. Although the management expects cRPO to slow to a 10.5% YoY growth rate in Q2, it is likely expecting it to pick up pace in the second half of the year given its upward revenue revision. Assuming that Okta can reignite growth back to its business by growing in the mid-teens after FY25 into FY27 on its path to becoming a $5B company, as it grows upmarket with higher ACV deals from larger customers, while deepening adoption through upsells with its product roadmap, it should generate close to $3.3B in revenue.

From a profitability standpoint, the management has also raised their guidance for non-GAAP operating margin from 18.5% to 19.5% for FY25. Assuming it can continue to grow its non-GAAP operating margin by 100 basis points every year as it streamlines its operating expenses, while unlocking operating leverage by driving higher spend per customer, it should generate $720M in non-GAAP operating income at a 21.5% margin in FY27. This will be equivalent to a present value of $595M when discounted at 10%.

Taking the S&P 500 as a proxy, where its companies grow their earnings on average by 8% over a 10-year period, with a price-to-earnings ratio of 15-18, Okta should trade at twice the multiple, given the projected growth rate of its earnings during this period of time. This will translate to a PE ratio of 34, or a price target of $120, which represents an upside of 30%.

Author’s Valuation Model

My final verdict and conclusions

I believe that Okta is starting to demonstrate its progress towards reigniting growth as it sees success in moving upmarket, winning larger ACV deals with enterprises. It is also encouraging to see that its cohort of $1M+ ACV customers is the fastest growing along with stabilizing NRR rates, indicating that it is able to successfully drive expansion of its solutions suite among its customer base. I also think that the company outperforming its cRPO target in Q1 is an early indication that its go-to-market strategies by realigning its sales team and better leveraging their partner ecosystem are starting to bear fruit while allowing them to expand their profitability. Although the competitive landscape is fierce, I believe that Okta can drive investor optimism once again as it continues to demonstrate success by moving upmarket. Assessing both the “good” and the “bad,” I reiterate my “buy” rating, as I believe that the stock is attractively positioned to drive long-term returns.

Read the full article here