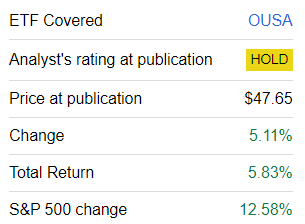

Continuing my series of updates on dividend-focused exchange-traded funds, today I would like to reassess the ALPS O’Shares U.S. Quality Dividend ETF (BATS:OUSA). This vehicle initially attracted my attention in June 2021, when I wrote the article with a neutral tone, chiefly influenced by its good but not excellent returns as well as its too-small dividend yield. My most recent analysis was presented in February of this year, when I addressed three essential matters:

- its inability to keep pace with the market,

- its hardly appealing dividend yield (a perennial concern), which back then stood at 1.76% (1.66% as of writing this article),

- and its somewhat burdensome expense ratio of 48 bps.

All these combined outweighed the fact that OUSA was capable of calibrating top-quality equity mixes with robust cash flows, moderate leverage, and decent returns on capital.

Today’s note is supposed to discuss OUSA’s recent soft performance, with due attention paid to detractors from and contributors to it, and offer an assessment of the changes in its factor mix to explain why this vehicle remains a Hold.

What is OUSA’s strategy?

From the fact sheet, we know that OUSA’s current underlying index, the O’Shares U.S. Quality Dividend Index, has been in place only since June 2020, while the fund itself was incepted in July 2015. And although there was some methodological overlap between it and the FTSE USA Qual/Vol/Yield Factor 5% Capped Index, which it abandoned, I prefer to ignore OUSA’s performance delivered prior to June 2020.

As mentioned in the summary prospectus:

The Underlying Index is constructed using a proprietary, rules-based methodology designed to select equity securities from the S-Network US Equity Large-Cap 500 Index that have exposure to the following four factors: 1) quality, 2) low volatility, 3) dividend yield and 4) dividend quality.

Investors seeking a dividend vehicle for more diversification should pay attention to the fact that the O’Shares index and, consequently, OUSA ignore such sectors as energy, materials, and real estate. I believe it is worth repeating my point from the July 2022 article. The gist here is that the removal of capital-intensive sectors that are closely connected to the economic cycle is more of a good thing for risk-adjusted returns and downside capture (smaller exposure to cyclicals should mean less sensitivity to market declines) in the long term. However, the OUSA investors would also likely miss on some tactical upside that these sectors can deliver in a favorable environment, i.e., when the WTI price is rising, which is boosting oil companies’ cash flows, or when the monetary conditions become looser, so real estate companies can benefit.

OUSA returns: comments on performance attribution

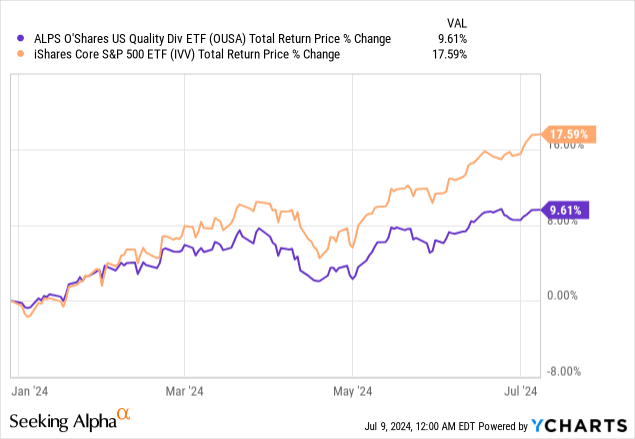

Since my February article, OUSA has disappointed again, as it has significantly underperformed the S&P 500.

Seeking Alpha

With January included, juxtaposed to the return of the iShares Core S&P 500 ETF (IVV), its result is not appealing either.

Certainly, this is not a growth portfolio by any means (a weighted-average forward revenue growth rate stood at just 5.6% in February, as per my calculations), so its inability to benefit from the long-duration equities rally is explainable.

Digging deeper, I should note that OUSA’s holdings have not changed since the previous coverage, which makes the performance attribution process much easier. The first fact that should be mentioned is that 52 stocks out of 100 (45.3% weight as of July 8) saw their price decline (the median was at -7.2%). The five companies below delivered the worst performance over the February 2–July 8 period:

| Symbol | Weight | Sector | % decline |

| Nike (NKE) | 0.68% | Consumer Discretionary | -27.5% |

| Brown-Forman (BF.B) | 0.06% | Consumer Staples | -26.0% |

| Starbucks (SBUX) | 0.70% | Consumer Discretionary | -19.8% |

| Accenture (ACN) | 1.40% | Information Technology | -19.7% |

| Bristol-Myers Squibb Company (BMY) | 0.43% | Health Care | -17.9% |

Created using data from Seeking Alpha and the fund

Stocks that gained had a median price return of 13.6%, yet they were unable to compensate for laggards. I compiled the top-performing companies below:

| Symbol | Weight | Sector | % price return |

| QUALCOMM (QCOM) | 1.44% | Information Technology | 46.7% |

| Broadcom (AVGO) | 4.89% | Information Technology | 42.6% |

| Eli Lilly (LLY) | 3.99% | Health Care | 37.5% |

| Garmin (GRMN) | 0.20% | Consumer Discretionary | 34.1% |

| Amphenol (APH) | 0.52% | Information Technology | 31.4% |

Created using data from Seeking Alpha and the fund

Besides, in the previous note, I mentioned that it was likely OUSA’s insufficient growth exposure that hindered it from demonstrating stronger gains. This time, the issue is the same. The argument I would like to present to corroborate is that stocks that have delivered negative returns over the period concerned have seen their median forward revenue growth rate decline, which means that pundits grew more skeptical about their prospects.

| Group | Median Revenue Fwd (February 3) | Median Revenue Fwd (July 9) |

| Stocks that gained | 5.35% | 5.42% |

| Stocks that declined | 4.91% | 3.57% |

Calculated using data from Seeking Alpha and the fund

Regarding sectors, it were communication, health care, and consumer staples that detracted most, while IT contributed significantly, as the sector enjoyed the buoyant environment marked by the expectations for interest rate cuts and AI adoption narrative.

| Sector | Average price return |

| Communication Services | -9.3% |

| Consumer Discretionary | -1.0% |

| Consumer Staples | 4.3% |

| Financials | 0.9% |

| Health Care | -2.2% |

| Industrials | 1.3% |

| Information Technology | 14.2% |

| Utilities | 26.1% |

Calculated using data from Seeking Alpha and the fund

Speaking of utilities, even though their average return was stellar, it is worth remarking that there are only two stocks from that sector in the OUSA portfolio, with a 2.24% weight. So their contribution was minor.

| Stock | Weight | Sector | % return |

| Public Service Enterprise Group Incorporated (PEG) | 0.44% | Utilities | 28.2% |

| NextEra Energy (NEE) | 1.80% | Utilities | 24.0% |

Calculated using data from Seeking Alpha and the fund

Overall, since the index change, OUSA has not only underperformed the market proxied with IVV but also a few counterparts from the dividend ETF universe, including the Schwab U.S. Dividend Equity ETF (SCHD), the Global X S&P 500 Quality Dividend ETF (QDIV), and the WisdomTree U.S. Quality Dividend Growth Fund ETF (DGRW).

| Metric | OUSA | IVV | SCHD | QDIV | DGRW |

| Start Balance | $10,000 | $10,000 | $10,000 | $10,000 | $10,000 |

| End Balance | $16,159 | $19,126 | $17,171 | $17,501 | $18,832 |

| CAGR | 12.47% | 17.21% | 14.16% | 14.69% | 16.77% |

| Standard Deviation | 14.88% | 17.10% | 15.98% | 16.53% | 15.19% |

| Best Year | 23.74% | 28.76% | 29.87% | 28.99% | 24.35% |

| Worst Year | -9.33% | -18.16% | -3.23% | -0.50% | -6.34% |

| Maximum Drawdown | -19.40% | -23.93% | -15.68% | -16.50% | -16.85% |

| Sharpe Ratio | 0.71 | 0.88 | 0.76 | 0.77 | 0.95 |

| Sortino Ratio | 1.19 | 1.45 | 1.41 | 1.33 | 1.71 |

| Upside Capture | 79.31% | 101.7% | 75.91% | 75.4% | 88.31% |

| Downside Capture | 86.02% | 98.18% | 73.12% | 69.88% | 80.65% |

Data from Portfolio Visualizer. The period is June 2020–June 2024

OUSA factor mix: quality dominates at the expense of growth and value

The OUSA portfolio as of July 8 is similar to the February version, as the index is reconstituted only once a year in September. However, holdings’ weights have changed owing to their out- or underperformance, so it is necessary to reassess factor exposures.

Value and dividends

OUSA’s weighted-average market cap has advanced to $668.3 billion from $540.4 billion as of the previous analysis. Despite such a massive WA market cap, it has a 4.1% earnings yield, as per my calculations, which is a bit stronger compared to 3.65% of the S&P 500 index. At the same time, the share of holdings with a B- Quant Valuation grade or higher is almost unchanged at 10.7% (10.6% in February).

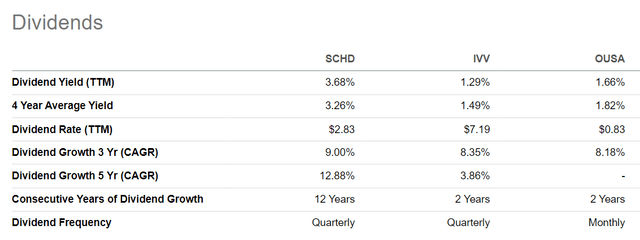

OUSA’s dividend yield has never been especially attractive. At this point, the WA DY of the portfolio is at around 2%, while the fund itself is yielding 1.66%. At the same time, the SCHD investors get 3.68% and the IVV investors get 1.29%.

Seeking Alpha

Growth

OUSA’s growth exposure remains clearly not spectacular. However, there has been a slight improvement in its allocation to stocks with a B- Quant Growth grade or better (32.9% in February vs. 35.5% in July). The growth rates are modest nonetheless.

| Portfolio as of | EPS Fwd | Revenue Fwd |

| July | 8.3% | 6.4% |

| February | 7.0% | 5.6% |

Calculated using data from Seeking Alpha and the fund

Quality

Regarding quality, OUSA has an unquestionably solid portfolio. Most holdings are cash-rich, with the share of FCF-positive companies at 89.1%. Next, capital efficiency is robust across the portfolio, as indicated by the adjusted Return on Equity of 23.7% (24.7% in February) and Return on Assets of 11.6% (12.3% in February), as per my calculations. ROE was calculated with negative and triple-digit outliers removed. The holdings with a B- Quant Profitability grade or higher account for 95.4% vs. 99.8% in February.

Low volatility

The lion’s share of OUSA’s net assets is allocated to low-beta names, which is reflected in the weighted-average figures, which have not changed at all:

| Coefficient | July | February |

| 24-month beta | 0.85 | 0.85 |

| 60-months beta | 0.87 | 0.87 |

Calculated using data from Seeking Alpha and the fund

Final thoughts: a rating upgrade is unnecessary

In conclusion, OUSA is offering a high-quality portfolio with an EY above that of the S&P 500. However, its dividend yield is hardly alluring, growth exposure is not spectacular, and returns leave a lot to be desired (partly due to the low volatility ingredient), especially assuming its 48 bps expense ratio. That is to say, my Hold rating remains unchanged.

Read the full article here