Buster Compares Total Returns With RYLD’s Yield. Buster Should Not Have Listened To Income Chasers.

On our last coverage of Global X Russell 2000 Covered Call ETF (NYSEARCA:RYLD) we gave it a sell and told you why you should stay away. We are going to look at how things have moved along since then and tell you why the call was the right one, even though the fund has delivered these returns.

The Performance

We are big believers in absolute numbers and you won’t find hand waiving when we assess our performance. If the indices are down 20% you won’t find us patting our own backs because we were down “only” 10%. So by that standard, RYLD is ahead since our Sell rating. But conceptually, our sell rating had a deeper purpose. To help investors sell the very long term problems with this fund and we think this six and half month period is excellent to do so.

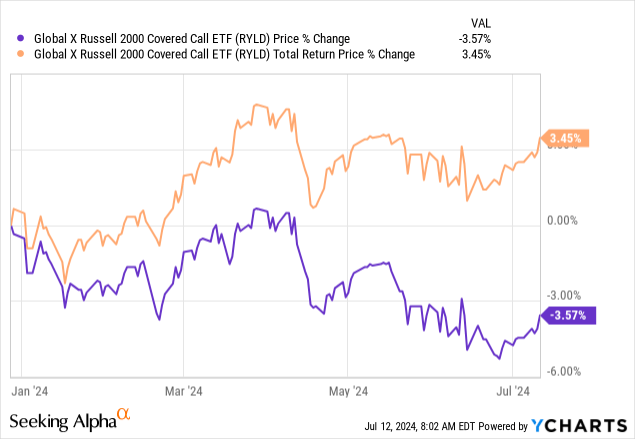

Let’s start with the chart above. First thing to notice is that the price is down 3.57%. That is about a 6% annualized rate. This is not an outlier. The fund has been falling quite steadily for some time.

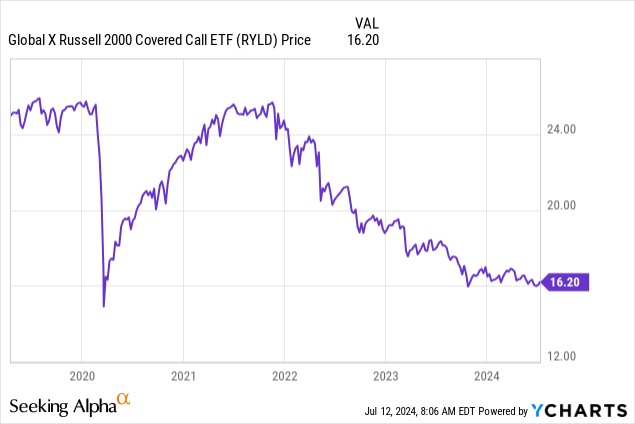

The price started at $25.00 and you have lost about $9.00 of capital in the process.

The second point we want to make on the returns is that 3.45% is not exactly earthshattering when you have risk free rates that would give you around 2.75% in the same time.

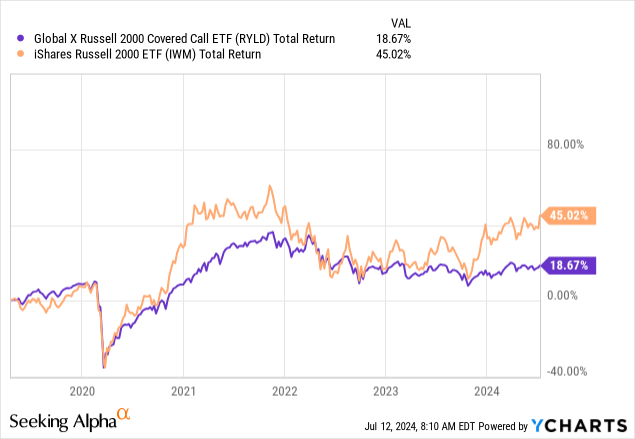

The third point here is that RYLD has really, really lagged. Here we are referring to how it has done relative to iShares Russell 2000 ETF (IWM). IWM does no covered calls and no fancy ways to generate income, and yet it has taken RYLD to the cleaners, since late 2023.

Why Consider Selling RYLD Today?

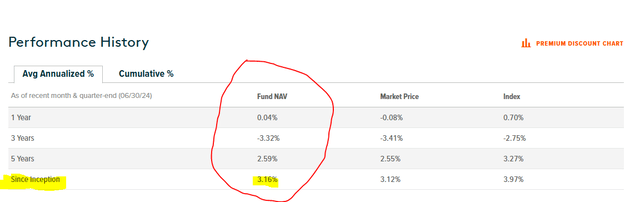

The fund’s total return since inception is sitting at 3.16%.

RYLD

That is the only real number that matters and not all those fictional 12% or 14% or 16% “yields”. One big question investors should have is what is the actual potential of this fund over the very long run. If these returns are below average, then there is of course some room to catch-up. There are a couple of ways to answer that. The first being the index returns themselves for the timeframe that RYLD has been around. These are actually easy to find and you can see them in the picture above. 3.97%. Across all 4 timeframes, one thing is clear, RYLD lags the performance of the index. There are two sources of this. One major and one minor. The major is the expense ratio of 0.6%. The fund pays it, the index does not. The second is slippage and this is worse in small caps than most other places. So RYLD will do about 0.8% annually less than what the index does. So what can you expect from the index, in the very long run?

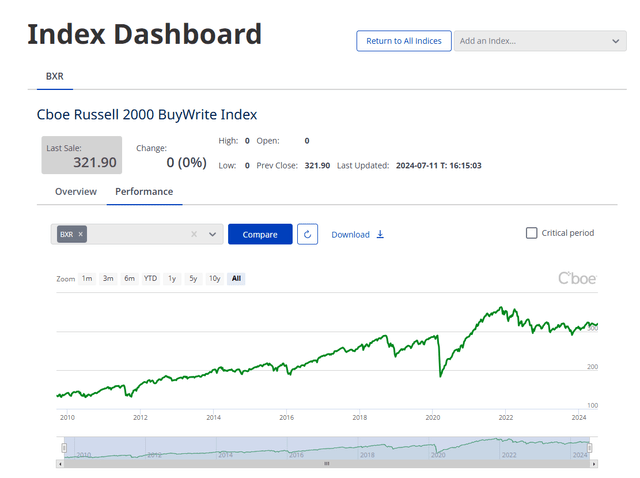

Unfortunately this index has not been around for too long, but it has certainly been around longer than RYLD. You can find the complete data set here. The performance below is the total return including all distributions.

CBOE

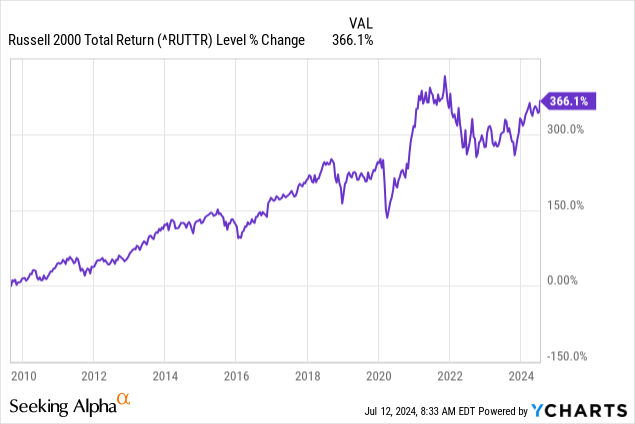

So what do those numbers tell you? The index moved from 134 to 321 in about 15 years. There are no compounded returns stated but we worked it out and it was very close to 6.1% per annum. Total cumulative return is about 140%. So RYLD would do about 5.3% annualized returns in the long run. Here is the Russell 2000 total return index over the same timeframe.

366.1% versus 140% for the covered call strategy. It is mind boggling that investors keep promoting blind-covered call selling as a way to generate returns when you are starting with a huge handicap.

Alternatives

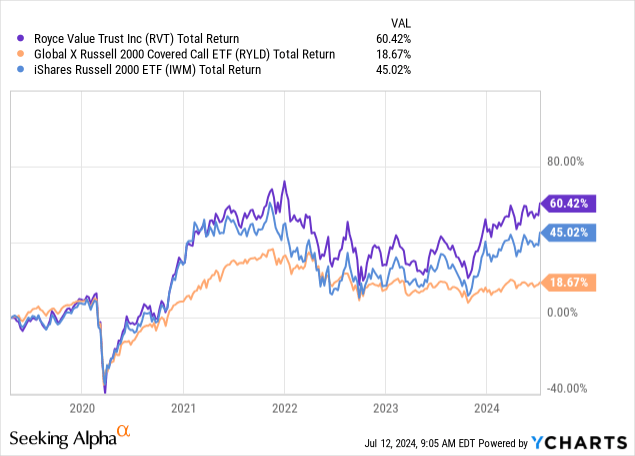

1) Royce Value Trust (RVT)

We have written about this fund before and won’t go into extensive details. But we will hit the highlights as to why this one is way better that RYLD. The first reason is the chart below. RVT has done 3X as well as RYLD and outperformed even IWM.

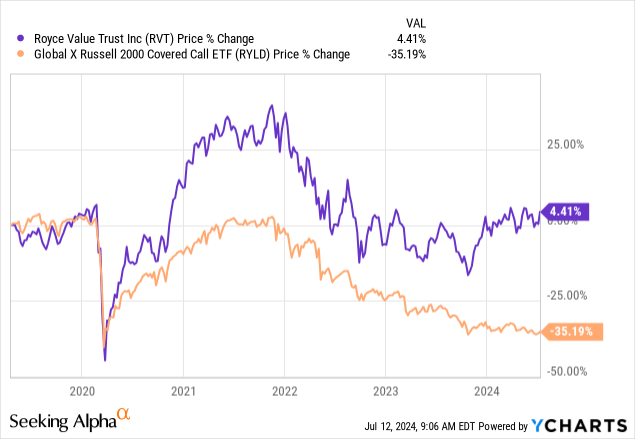

The fund doles a generous (but variable) distribution. While this is not as high as RYLD, the fund has managed to earn it over the long run. You can figure that out simply with the next chart.

We view small cap space as very bifurcated. There are very good values but also very expensive and poor quality stocks in the index. We don’t want to own IWM. RVT is the best trade on this.

2) Individual Covered Calls On Value Stocks

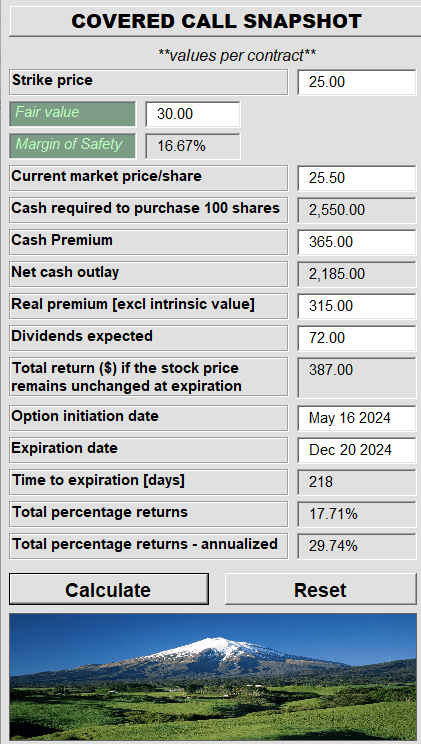

It is easy to buy one ETF and then sit back and count the income. Of course in the case of RYLD, the only thing you have more of since your bought, is regret. Individual stocks are more work. But they can give you far more yield and better risk-adjusted returns. We will go over one we did recently to show you how it works out. Riley Exploration Permian, Inc. (REPX) is a small cap oil and gas producer that was caught in some relentless selling in April and May of this year. With the stock at $25.50, we felt there was an interesting income setup on May 16, 2024. We sold the covered calls for December 2024, for $25 strikes, for $3.65 each.

The stock is quite volatile but the value tends to change in a slower manner over time. Due to the high premiums we received, our net cost basis was just $21.85. Also, we were going to make an annualized yield of 29.74%, as long as the stock did not decline below $25.00 on option expiration.

Author’s App

In other words, if the stock even fell 2% by option expiration we would make a near 30% yield. As it turns out, the stock has rallied and we are sitting back collecting the fat premium and the dividends. An early exercise is possible, but that will only move up our yield substantially. The key aspect here is that we waited for a good price after a sizeable decline and then created a further large buffer. If you do this on small-caps with due diligence, you can improve your returns above RYLD. You can see a longer term performance chart over here of this methodology.

Verdict

RYLD could outperform IWM over the next 24 months if we have a severe bear market. That should push up implied volatility and the premiums could offset some declines in the NAV. So in that scenario both would give you negative returns, but RYLD less so. Even in a bear market, RYLD could underperform. Bear market rallies are fierce and RYLD could squander all upside by selling calls at the wrong time. We see no reason to support this methodology and continue to rate this as a Sell.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Read the full article here