Written by Sam Kovacs

Introduction

The Schwab U.S. Dividend Equity ETF (NYSEARCA:SCHD) tracks the Dow Jones US 100 Dividend index, which is overall a very well constructed index.

In a nutshell, the index is made of 100 stocks from the Dow Jones Broad Market index, filtered for the following characteristics.

- Dividend yield: Prioritizes companies with strong current dividend yields.

- Dividend payment history: Requires at least 10 consecutive years of dividend payments.

- Free cash flow to total debt: Focuses on companies with healthy financials to sustain dividend payments.

- Return on equity: Selects companies that generate strong profitability.

- Dividend growth rate: Emphasizes companies with a history of growing dividends.

In a recent article comparing our (superior) performance to that of SCHD, I pointed out one weakness of the ETF, which is that it had no exposure to REITs, and that dividend investors who wanted to go the passive investing route would be better suited to incorporate some REIT exposure into their portfolios given the current market environment. An easy way to do it would be to add the Cohen & Steers Quality Income Realty Fund (RQI).

I must admit, though, that I do not cater to the passive investor crowd. I’m an active investor at heart. I like to pick my securities, at which price and when I buy them, and at which price and when I sell them.

It’s the same reason I don’t buy premade boxes of assorted chocolates. Sure there are a few you really like, and maybe a couple you didn’t know of that turn out to be great surprises, but I really don’t like those cherry liquor ones, and I’m forced to throw them out, to my great displeasure.

When you buy an ETF, you buy all of the stocks at today’s price. This idea is a very dangerous one to me.

It says: I don’t care about price, just give me a basket of stocks.

This is a very challenging proposition, because if you want to get returns which are disproportionate to the risk you’re taking (the core tenant of value investing), then the most important factor is price.

Don’t believe me? That’s fine. How about generations of investors, far more successful than myself, who all drive home the same point.

The memory lane of value investors stressing the importance of price.

Let’s go down the memory lane of value investing quotes, stressing the importance of the price you pay.

- The intelligent investor is a realist who sells to optimists and buys from pessimists. – Ben Graham

- Price is what you pay, value is what you get. – Warren Buffett

- Value investors know better: They understand that the future price of a stock depends on the present price they pay for it. – Seth Klarman

- No matter how wonderful a business is, it’s not worth an infinite price. – Charlie Munger

- Risk comes from the price you pay. It’s more about what you pay for an asset than the asset itself. – Howard Marks

- All intelligent investing is value investing — acquiring more than you are paying for. You must value the business in order to value the stock. – Charlie Munger

- The secret to investing is to figure out the value of something – and then pay a lot less. – Joel Greenblatt

- I seek individual opportunities where the price is far lower than the value, which is something most investors overlook. – Michael Burry

- The discipline of buying only when prices are attractive is a winning formula for long-term success. – Jean Marie Eveillard

- You have to be an intelligent speculator and recognize when prices are too low. – Irving Kahn

- The key to value investing is not just finding the right business, but paying the right price for it. – Mohnish Pabrai

- We buy businesses that are mispriced because the market temporarily overlooks their value. – Sanjay Bakshi

- Price is the only thing that matters. If the price is too high, stay away. – Walter Schloss

- To beat the market, you have to find stocks that are mispriced. – Bruce Greenwald

Decades of good investing advice is thrown out with the bathwater with investing ETFs.

Some setbacks of SCHD’s methodology

Like I mentioned earlier, SCHD does a very good job at applying a few filters which ensure that a reasonable selection of stocks are included, there are some pitfalls.

While dividend yield is considered, it’s only sorted relative to the universe and not relative to a stock’s valuation. If a stock which has historically yielded 5% now yields 3% (and thus might be quite overvalued) then it could still very well be included in the methodology.

The return on equity metric as a source of quality of earnings is questionable. For one net income is a highly variable input, which creates a lot of noise around one time events. Second, in the age of shareholder buybacks, equity can be depressed to low levels which inflate ROE. These are things we can live with when analyzing stocks individually as we can make adjustments, but it makes it a subpar screener.

This is mitigated somewhat by the free cash flow to total debt ratio, which I believe is a great ratio to include in a screen and is a big part of the reason that the SCHD gets good quality stocks within it.

The dividend growth rate is used as a factor in ranking the securities within the index, but it’s once again looked at in isolation rather than relative to dividend yield.

It’s hard to say whether a 7% dividend growth rate is satisfactory without linking it to a dividend yield. For a stock yielding 4% it would be very satisfactory. If the stock yields 2%, intuitively you’d expect more growth. This isn’t considered in the SCHD and creates an opportunity for overvalued stocks to get included, or stocks which would produce subpar income returns.

This is particularly problematic when it is marketed towards investors seeking dividend income.

As a dividend investor, I want to be getting the most bang for buck, SCHD falls short in quite a few ways.

How our methodology diverges from ETF investing

Because price is such an important element in investing, we use it to identify two factors which improve our results: Value and momentum.

We focus on buying stocks when they trade at yields which are superior to their 10-year median yield, which we track using our Dividend Freedom Tribe (DFT) charts.

These charts help identify times when a stock’s dividend yield suggests it’s undervalued relative to its historical norms, allowing us to capitalize on temporary market inefficiencies. We also tie in a growth aspect, to buy stocks when the dividend growth in conjunction with the dividend yield is attractive.

Even for high-growth stocks, which often trade at a premium, there are periods when sentiment or external factors create the opportunity to buy at favorable prices, as we’ll see in this article.

But value alone isn’t enough. Timing is crucial, and this is where momentum comes into play. We use the 200-day simple moving average as a “bare bones” technical signal to confirm whether a stock’s price movement aligns with its fundamental value.

A stock trading above its 200-day SMA indicates positive momentum, suggesting the market is starting to recognize the value we see. Conversely, if a stock breaks below the 200-day SMA, it could signal the start of a downturn, prompting a reassessment in our exit strategy.

Furthermore, while SCHD focuses on strong, stable dividend-payers with a consistent payout history, it doesn’t consider the relationship between current dividend yield and historical norms as we do.

Additionally, we focus on the combination of dividend yield and growth, whereas SCHD focuses more on dividend yield and consistency. Again this discards price from the investing decision.

So it must be understood that when I present the “worst” stocks in the SCHD, it’s not the worst business, but the worst stocks to buy today, due to unreasonable valuations.

Buying a stock when it’s severely overvalued sets you up for failure. For dividend investors, this should be of particular concern:

Not only is your capital at risk, but you’re receiving less dividend income than you could have from buying these stocks at great prices.

Approaching the task systematically.

First I got a hold of all the 100 constituents of the SCHD.

I discarded all that had a weight of less than 0.1%, because let’s face it, they don’t contribute much to the portfolio.

Doing so removed 33 names, while only removing 1.68% of the portfolio. So we’re dealing with 67 names which represent 98.32% of SCHD.

I listed them below with their dividend yield, 10-year historical yields (median, 25th percentile, and 75th percentile) as well as the one-year, five-year, and 10-year dividend growth scores.

I also threw in our momentum score for good measure (slightly different from SA’s but overall a similar methodology).

| Company | Last price | Dividend Yield | 25th Percentile 10 year Dividend Yield | Median 10 year Dividend Yield | 75th Percentile 10 year Dividend Yield | Dividend 1 year CAGR | Dividend 5 year CAGR | Dividend 10 year CAGR | Price Momentum Score | Relative Dividend Valuation |

| Coterra Energy Inc. (CTRA) | 23.49 | 3.58 | 0.36 | 1.43 | 2.25 | 5 | 19.77 | 27.23 | 3 | undervalued |

| Apache Corporation (APA) | 25.97 | 3.85 | 1.41 | 2.12 | 2.77 | 0 | 0 | 0 | 3 | undervalued |

| HF Sinclair Corp (DINO) | 45.58 | 4.39 | 2.83 | 3.35 | 4.27 | 11.11 | 8.67 | 0 | 3 | undervalued |

| MSC Industrial Direct Company Inc. (MSM) | 77.51 | 4.28 | 2.43 | 3.28 | 3.72 | 5.06 | 2.05 | 9.66 | 3 | undervalued |

| Huntsman Corporation (HUN) | 21.91 | 4.56 | 2.25 | 2.84 | 3.44 | 5.26 | 9 | 7.18 | 3 | undervalued |

| United Parcel Service Inc. (UPS) | 127.4 | 5.12 | 2.8 | 3.09 | 3.5 | 0.62 | 11.17 | 9.3 | 4 | undervalued |

| Chevron Corporation (CVX) | 140.93 | 4.63 | 3.78 | 4.04 | 4.56 | 7.95 | 6.49 | 4.3 | 4 | undervalued |

| Valero Energy Corporation (VLO) | 135.52 | 3.16 | 2.93 | 3.67 | 4.45 | 4.9 | 3.52 | 14.55 | 4 |

slightly overvalued |

| Ford Motor Company (F) | 10.77 | 5.57 | 4.02 | 4.89 | 5.77 | 0 | 0 | 2.21 | 4 |

slightly undervalued |

| LyondellBasell Industries NV Class A (LYB) | 94.23 | 5.69 | 3.76 | 4.47 | 5.15 | 7.2 | 5 | 6.71 | 4 | undervalued |

| T. Rowe Price Group Inc. (TROW) | 104.12 | 4.76 | 2.45 | 2.84 | 3.44 | 1.64 | 10.29 | 10.92 | 4 | undervalued |

| CF Industries Holdings Inc. (CF) | 78.54 | 2.55 | 2.09 | 2.59 | 3.31 | 25 | 10.76 | 5.24 | 4 |

slightly overvalued |

| Vail Resorts Inc. (MTN) | 185.1 | 4.8 | 2 | 2.47 | 3.3 | 7.77 | 4.75 | 18.26 | 4 | undervalued |

| Robert Half International Inc. (RHI) | 61.4 | 3.45 | 1.69 | 2.01 | 2.32 | 10.42 | 11.32 | 11.4 | 4 | undervalued |

| Western Union Company (WU) | 12.07 | 7.79 | 3.35 | 3.92 | 5.23 | 0 | 3.28 | 6.52 | 4 | undervalued |

| Insperity Inc. (NSP) | 88.6 | 2.71 | 1.3 | 1.7 | 1.96 | 5.26 | 15.26 | 21.4 | 4 | undervalued |

| Cisco Systems Inc. (CSCO) | 49.13 | 3.26 | 2.86 | 3.08 | 3.36 | 2.56 | 2.71 | 7.73 | 5 |

slightly undervalued |

| Bristol-Myers Squibb Company (BMY) | 49.8 | 4.82 | 2.59 | 2.93 | 3.27 | 5.26 | 7.91 | 5.24 | 5 | undervalued |

| Pfizer Inc. (PFE) | 28.51 | 5.89 | 3.35 | 3.69 | 4.03 | 2.44 | 4.26 | 5.48 | 5 | undervalued |

| EOG Resources Inc. (EOG) | 121.55 | 2.99 | 0.71 | 1.35 | 2.64 | 0 | 25.92 | 18.96 | 5 | undervalued |

| Fastenal Company (FAST) | 65.18 | 2.39 | 2.3 | 2.54 | 2.74 | 11.43 | 12.32 | 12.14 | 5 |

slightly overvalued |

| The Hershey Company (HSY) | 198.1 | 2.77 | 2.01 | 2.28 | 2.54 | 14.93 | 12.13 | 9.86 | 5 | undervalued |

| Darden Restaurants Inc. (DRI) | 157.94 | 3.55 | 2.82 | 3.09 | 3.42 | 6.87 | 9.73 | 11.01 | 5 | undervalued |

| Skyworks Solutions Inc. (SWKS) | 101.39 | 2.76 | 1.23 | 1.48 | 2.15 | 2.94 | 9.73 | 20.33 | 5 | undervalued |

| Snap-On Incorporated (SNA) | 272.09 | 2.73 | 1.68 | 2.29 | 2.63 | 14.81 | 14.38 | 15.51 | 5 | undervalued |

| Interpublic Group of Companies Inc. (IPG) | 31.46 | 4.2 | 2.83 | 3.54 | 4.1 | 6.45 | 7.03 | 13.26 | 5 | undervalued |

| Tapestry Inc. (TPR) | 41.01 | 3.41 | 2.96 | 3.45 | 3.99 | 0 | 0.73 | 0.36 | 5 |

slightly overvalued |

| Whirlpool Corporation (WHR) | 97.53 | 7.18 | 2.36 | 2.79 | 4.16 | 0 | 7.84 | 8.84 | 5 | undervalued |

| Bank of the Ozarks (OZK) | 40.98 | 3.9 | 1.54 | 2.72 | 3.4 | 11.11 | 10.76 | 12.79 | 5 | undervalued |

| Home Depot Inc. (HD) | 361.85 | 2.49 | 2.05 | 2.24 | 2.48 | 7.66 | 10.59 | 16.95 | 6 | undervalued |

| Verizon Communications Inc. (VZ) | 41.31 | 6.56 | 4.35 | 4.65 | 5.14 | 1.88 | 1.95 | 2.11 | 6 | undervalued |

| PepsiCo Inc. (PEP) | 179.3 | 3.02 | 2.73 | 2.83 | 2.97 | 7.11 | 7.25 | 7.54 | 7 | undervalued |

| Paychex Inc. (PAYX) | 130.07 | 3.01 | 2.81 | 3.04 | 3.21 | 10.11 | 9.59 | 9.94 | 7 |

slightly overvalued |

| Watsco Inc. (WSO) | 449.55 | 2.4 | 2.55 | 2.88 | 3.33 | 10.2 | 11.03 | 16.23 | 7 | overvalued |

| Unum Group (UNM) | 55.26 | 3.04 | 2.07 | 2.93 | 3.82 | 15.07 | 8.06 | 9.79 | 7 |

slightly undervalued |

| Nexstar Media Group Inc. (NXST) | 162.78 | 4.15 | 1.72 | 1.91 | 2.25 | 25.19 | 30.3 | 27.4 | 7 | undervalued |

| BlackRock Inc. (BLK) | 876.64 | 2.33 | 2.29 | 2.54 | 2.82 | 2 | 9.1 | 10.2 | 8 |

slightly overvalued |

| Amgen Inc. (AMGN) | 324.36 | 2.77 | 2.55 | 2.79 | 3.11 | 5.63 | 9.18 | 13.94 | 8 |

slightly overvalued |

| Texas Instruments Incorporated (TXN) | 201.55 | 2.58 | 2.42 | 2.62 | 2.84 | 4.84 | 11.04 | 15.79 | 8 |

slightly overvalued |

| U.S. Bancorp (USB) | 45.54 | 4.3 | 2.34 | 2.88 | 4.11 | 2.08 | 5.78 | 7.18 | 8 | undervalued |

| Kimberly-Clark Corporation (KMB) | 146.83 | 3.32 | 3.03 | 3.28 | 3.51 | 3.39 | 3.44 | 4.24 | 8 |

slightly undervalued |

| Amcor Plc (AMCR) | 11.22 | 4.46 | 3.92 | 4.14 | 4.53 | 2.04 | 0.82 | 1.33 | 8 |

slightly undervalued |

| Dick’s Sporting Goods Inc (DKS) | 214.83 | 2.05 | 1.35 | 1.99 | 2.58 | 10 | 31.95 | 24.81 | 8 |

slightly undervalued |

| Comerica Incorporated (CMA) | 55.05 | 5.16 | 1.76 | 3.26 | 4.34 | 0 | 1.17 | 13.51 | 8 | undervalued |

| Lockheed Martin Corporation (LMT) | 568.59 | 2.22 | 2.5 | 2.69 | 2.9 | 5 | 7.44 | 9 | 9 | overvalued |

| AbbVie Inc. (ABBV) | 192.86 | 3.21 | 3.55 | 3.92 | 4.53 | 4.73 | 7.69 | 13.95 | 9 | overvalued |

| Coca-Cola Company (KO) | 71.17 | 2.73 | 2.98 | 3.14 | 3.31 | 5.43 | 3.93 | 4.75 | 9 | overvalued |

| Altria Group Inc. (MO) | 54.27 | 7.52 | 4.01 | 6.66 | 8.15 | 4.08 | 3.96 | 6.97 | 9 |

slightly undervalued |

| ONEOK Inc. (OKE) | 91.81 | 4.31 | 5.01 | 5.58 | 6.5 | 3.66 | 2.15 | 5.58 | 9 | overvalued |

| Fifth Third Bancorp (FITB) | 41.7 | 3.36 | 2.54 | 2.96 | 3.71 | 6.06 | 7.84 | 10.41 | 9 |

slightly undervalued |

| M&T Bank Corporation (MTB) | 168.8 | 3.2 | 2.27 | 2.59 | 3.22 | 3.85 | 6.19 | 6.79 | 9 |

slightly undervalued |

| Cincinnati Financial Corporation (CINF) | 136.34 | 2.38 | 2.47 | 2.73 | 2.97 | 8 | 7.66 | 6.44 | 9 | overvalued |

| Huntington Bancshares Incorporated (HBAN) | 14.65 | 4.23 | 2.68 | 3.95 | 4.57 | 0 | 0.66 | 11.98 | 9 |

slightly undervalued |

| Regions Financial Corporation (RF) | 22.61 | 4.42 | 2.31 | 3.12 | 3.95 | 4.17 | 10.03 | 17.46 | 9 | undervalued |

| Best Buy Co. Inc. (BBY) | 99.41 | 3.78 | 2.37 | 2.7 | 3.79 | 2.17 | 13.46 | 17.64 | 9 |

slightly undervalued |

| Packaging Corporation of America (PKG) | 203.98 | 2.45 | 2.68 | 2.98 | 3.32 | 0 | 9.61 | 12.07 | 9 | overvalued |

| FNF Group of Fidelity National Financial Inc. (FNF) | 58.99 | 3.25 | 2.55 | 3.17 | 3.91 | 6.67 | 9.14 | 0 | 9 |

slightly undervalued |

| KeyCorp (KEY) | 16.24 | 5.05 | 2.22 | 3.63 | 4.63 | 0 | 2.07 | 12.17 | 9 | undervalued |

| C.H. Robinson Worldwide Inc. (CHRW) | 101.56 | 2.44 | 2.13 | 2.33 | 2.52 | 1.64 | 4.4 | 5.88 | 9 |

slightly undervalued |

| East West Bancorp Inc. (EWBC) | 80.57 | 2.73 | 1.73 | 2.08 | 2.53 | 14.58 | 14.87 | 11.82 | 9 | undervalued |

| H&R Block Inc. (HRB) | 63.55 | 2.36 | 2.79 | 3.67 | 4.21 | 17.19 | 7.6 | 6.49 | 9 | overvalued |

| Zions Bancorporation (ZION) | 46.15 | 3.55 | 0.97 | 2.44 | 3.29 | 0 | 3.82 | 26.2 | 9 | undervalued |

| Synovus Financial Corp. (SNV) | 43.89 | 3.46 | 1.47 | 2.83 | 3.61 | 0 | 4.84 | 18.43 | 9 |

slightly undervalued |

| Radian Group Inc. (RDN) | 35.33 | 2.77 | 0.06 | 0.08 | 3.17 | 8.89 | 150.18 | 58.17 | 9 |

slightly undervalued |

| Columbia Banking System Inc. (COLB) | 24.25 | 5.94 | 2.5 | 3.33 | 4.28 | 0 | 5.28 | 0 | 9 | undervalued |

| Janus Henderson Group plc (JHG) | 36.46 | 4.28 | 4.32 | 5.48 | 6.26 | 0 | 1.61 | 0 | 9 | overvalued |

| International Bancshares Corporation (IBOC) | 61.34 | 2.15 | 2.07 | 2.38 | 2.77 | 4.76 | 3.71 | 9.35 | 9 |

slightly overvalued |

The final column shows the relative valuation compared to the dividend yield.

Remember this is not an end in itself, it’s the beginning of the process.

Assessing the worst buys today

OK, so how would we assess the worst stocks in SCHD you could buy today?

First we will filter for those that are either overvalued, or slightly overvalued relative to their historical 10-year median yield.

We will then look at the yields, the expected growth rates, and the price momentum (using our momentum score and the 200-day SMA as a bare bones technical signal).

Why the 200D SMA? It’s elegant, simple, doesn’t give too many false signals, and can serve as a great way to get out before the worst happens.

As legendary trade Paul Tudor Jones explained on an interview with Tony Robbins:

My metric for everything I look at is the 200-day moving average of closing prices. I’ve seen too many things go to zero, stocks and commodities. The whole trick in investing is: “How do I keep from losing everything?” If you use the 200-day moving average rule, then you get out. You play defense, and you get out.

This reduces our list to 18 stocks.

Below I’ll list them and paste their DFT charts, which will give a graphic representation of the historical yields listed in the table above, as well as the 200D SMA.

A picture is worth a thousand words, and I’m sure seeing this visually will accelerate the task at hand.

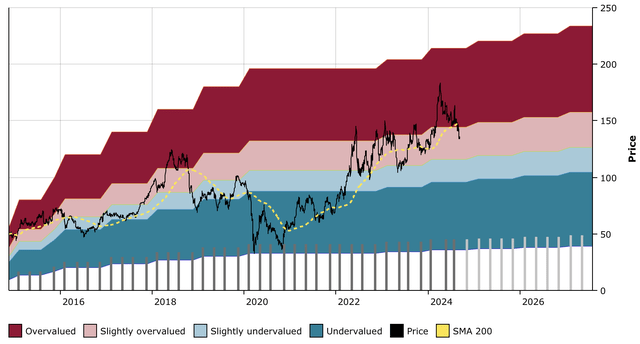

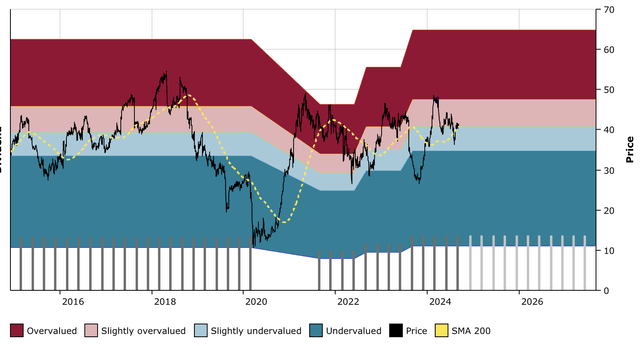

1. Valero Energy (VLO)

VLO DFT Chart (Dividend Freedom Tribe)

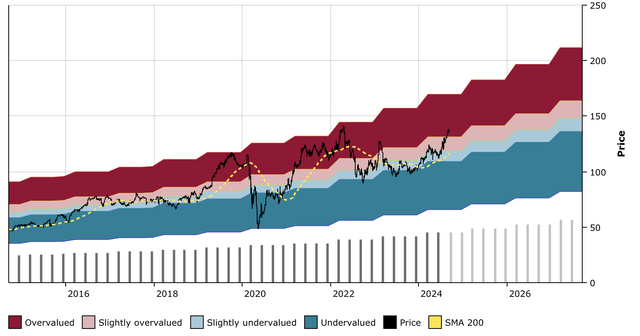

2. CF Industries (CF)

CF DFT Chart (Dividend Freedom Tribe)

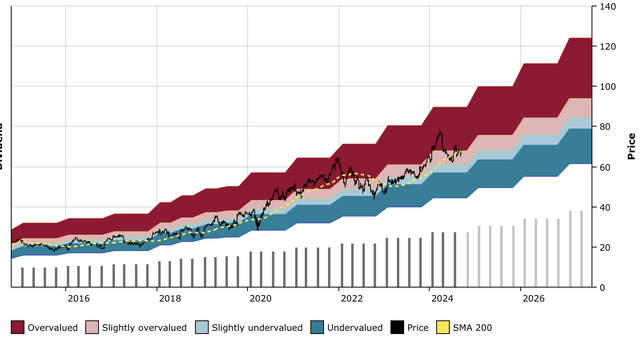

3. Fastenal (FAST)

FAST DFT Chart (Dividend Freedom Tribe)

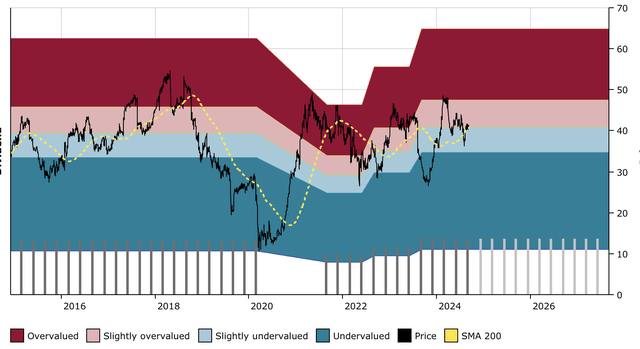

4. Tapestry (TPR)

TPR DFT Chart (Dividend Freedom Tribe)

5. Paychex (PAYX)

PAYX DFT Chart (Dividend Freedom Tribe)

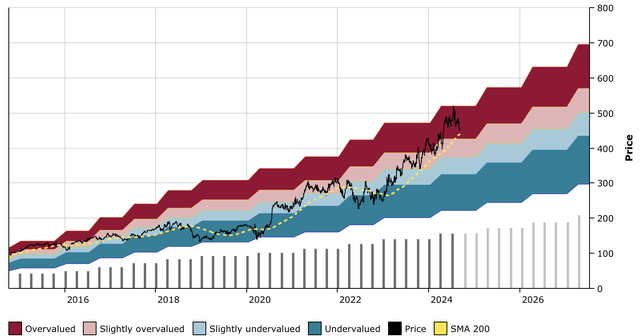

6. Watsco (WSO)

WSO DFT Chart (Dividend Freedom Tribe)

7. Blackrock (BLK)

BLK DFT Chart (Dividend Freedom Tribe)

8. Amgen (AMGN)

AMGN DFT Chart (Dividend Freedom Tribe)

9. Texas Instruments (TXN)

TXN DFT Chart (Dividend Freedom Tribe)

10. Lockheed Martin (LMT)

LMT DFT Chart (Dividend Freedom Tribe)

11. Abbvie (ABBV)

ABBV DFT Chart (Dividend Freedom Tribe)

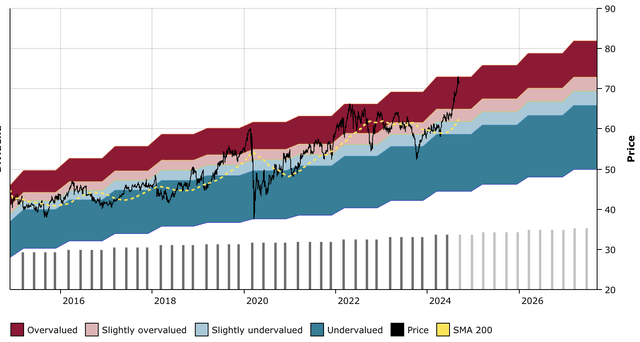

12. Coca Cola (KO)

KO DFT Chart (Dividend Freedom Tribe)

13. Oneok (OKE)

OKE DFT Chart (Dividend Freedom Tribe)

14. Cincinnati Financial (CINF)

CINF DFT Chart (Dividend Freedom Tribe)

15. Packaging Corporation of America (PKG)

PKG DFT Chart (Dividend Freedom Tribe)

16. H&R Block (HRB)

HRB DFT Chart (Dividend Freedom Tribe)

17. Janus Henderson (JHG)

JHG DFT Chart (Dividend Freedom Tribe)

18. International Bancshares Corp (IBOC)

IBOC DFT Chart (Dividend Freedom Tribe)

The five worst dividend buys today.

Looking at the charts above there are five that stand out to me as the worst buys today:

- Valero

- Fastenal

- Tapestry

- Watsco

- Coca Cola

Let’s dive into why when we care about price, (and therefore about value and momentum) each of these are particularly unattractive.

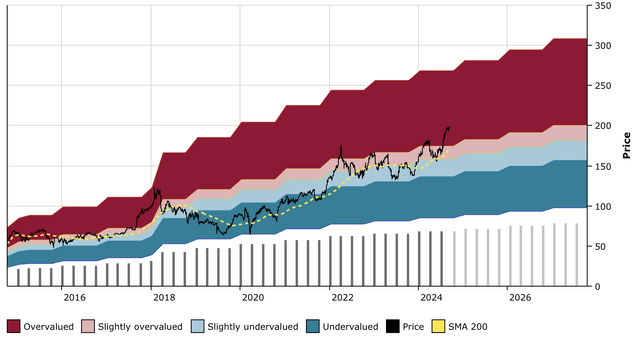

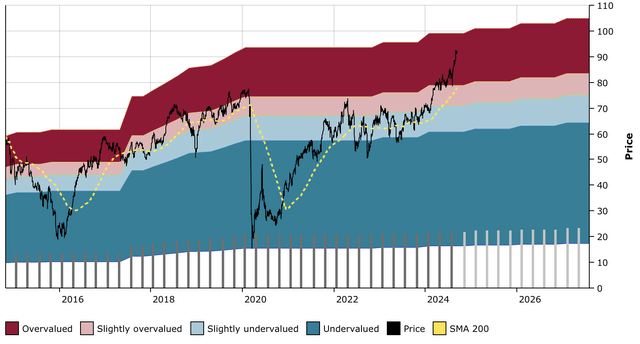

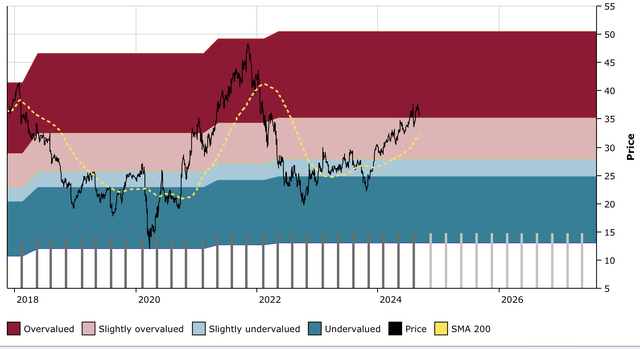

1. Valero

Valero peaked on April 2 this year at $177, and has since fallen to $136.

On Aug. 21, it crossed below its 200-day SMA, and has continued to dip lower.

Let’s see this on the chart again:

VLO DFT Chart (Dividend Freedom Tribe)

While there have been quite a few false signals in the past two years from the SMA, this time it comes as oil prices are going lower, and as Valero is coming off a historically very overvalued price relative to the dividend.

It yields 3.15% which is still quite a bit below its 10-year median yield of 3.67%.

Given the past couple of years history of growing the dividend at 5% per annum, its hard to get excited by a 3.15% yield.

There’s a good chance Valero goes back to $115 in upcoming months, and as such I’d be very cautious investing in the stock.

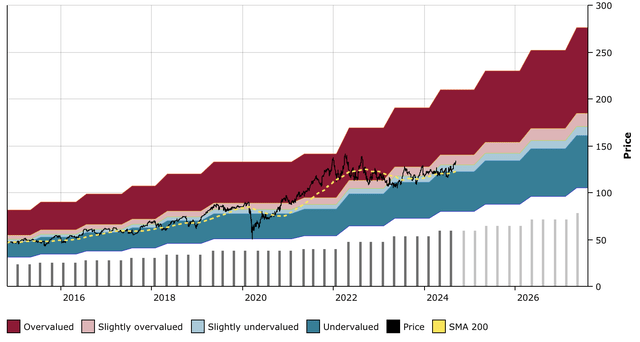

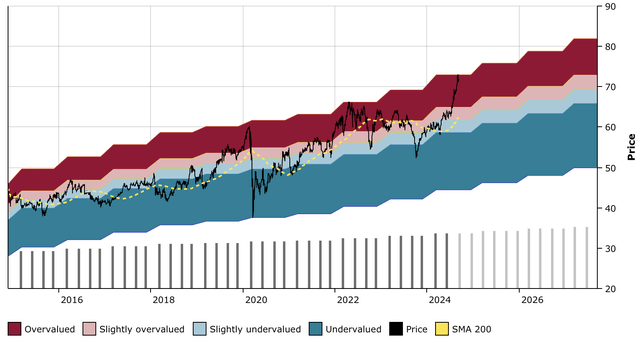

2. Fastenal

FAST peaked at $75 on March 15 this year, and crossed its 200D SMA on June 7, which proved to be a fluke, then again on Aug. 23.

FAST DFT Chart (Dividend Freedom Tribe)

This double dip below the 200D SMA is quite a dangerous setup, and one that looks just like the situation we faced in 2022, when FAST dropped by another 13% after that signal.

The low 2.27% yield is well supported by dividends growing at 11%-12%. But with payout ratios at 75% (earnings and FCF) one might question their ability to sustain such a growth rate as revenues are dropping.

I wouldn’t want to buy at these prices, with this budding negative momentum.

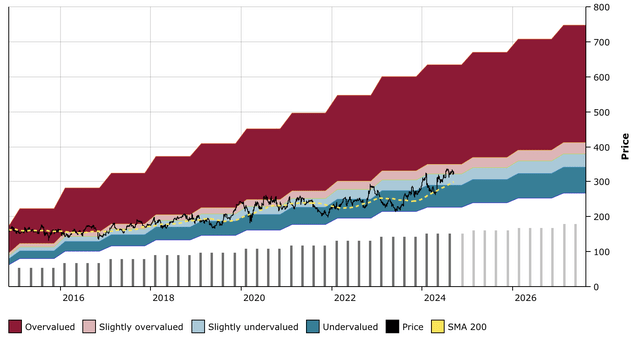

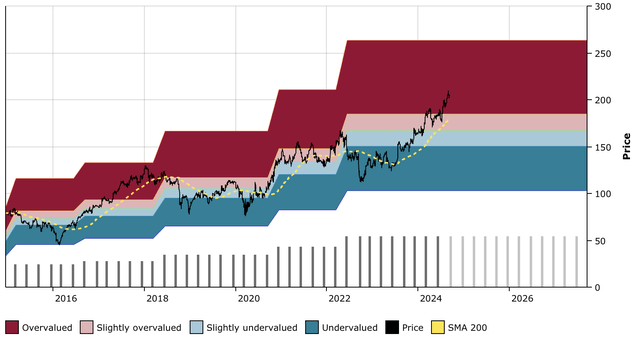

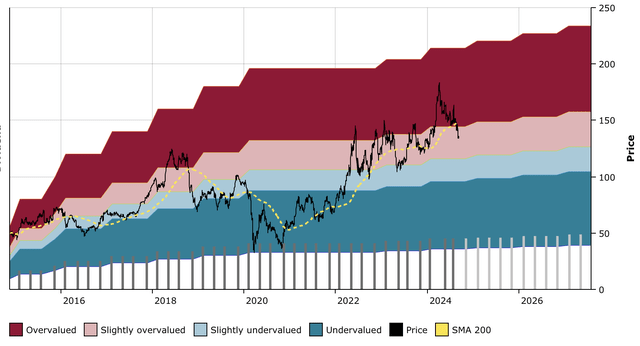

3. Tapestry

Tapestry’s dividend history isn’t exactly glorious.

Flat from 2015 to 2020, then suspended for a year, reinstated in late 2021 at a lower level, and has increased twice to a slightly higher baseline. Investors might have expected an increase in August, but management kept the dividend flat.

I always exert caution with consumer discretionary brands, especially those that sell “luxury” accessories, through brands like Kate Spade and Coach.

TPR DFT Chart (Dividend Freedom Tribe)

They’re just too tied to economic ups and downs, and haven’t proven an ability to significantly return capital to investors.

The stock is yielding 3.4%, and frankly that doesn’t get me excited.

Anyone manually picking stocks would skip TPR, but by a fluke it managed to make its way past SCHD’s screening process.

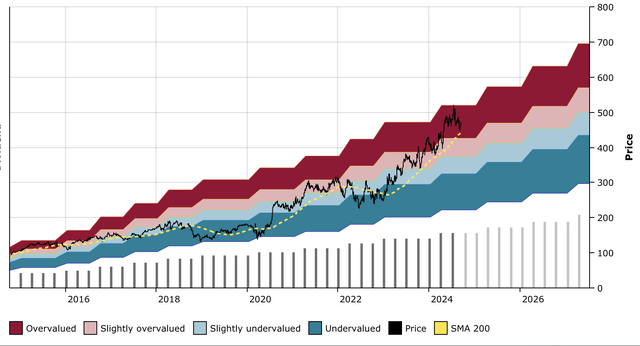

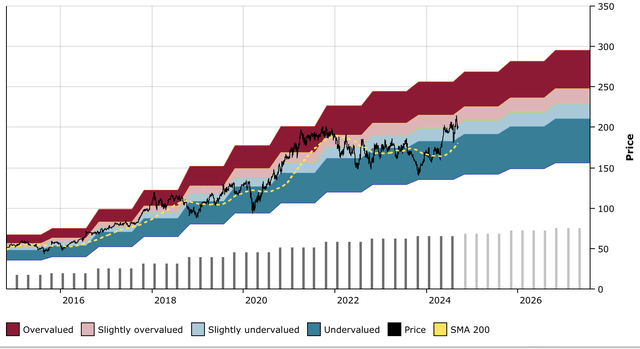

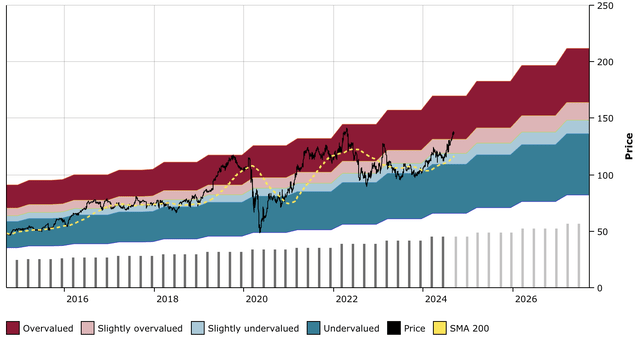

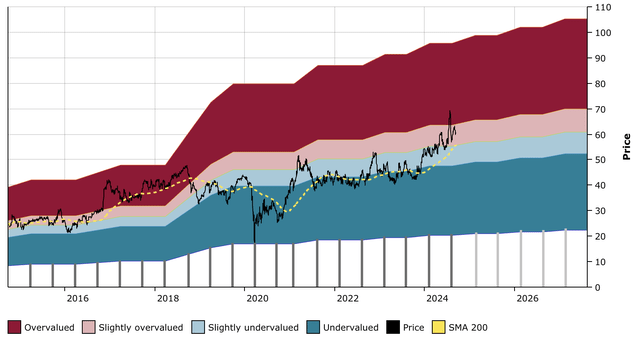

4. Watsco

Watsco peaked on July 16 1t $519.9. Since then, it has corrected to $455.

The level it reached in July, when it yielded 2.08%, was similar to the amount it yielded in 2015 before dropping.

WSO DFT Chart (Dividend Freedom Tribe)

WSO hasn’t yet crossed below its 200 day SMA, but it looks like it’s heading there, and if it crosses below, it might mean danger.

The 2.37% yield is quite below the ten year median 2.88%, and while the 59% FCF payout ratio is healthy, and the history of growing dividends at double-digit rates is encouraging, a reversal looks like it’s in the books.

I see a clear route to a 10% to 15% drop from here in the upcoming year.

I love the stock, the AI data center tailwind for cooling equipment, but I think the valuation has gotten a bit carried away. I wouldn’t be buying at these levels.

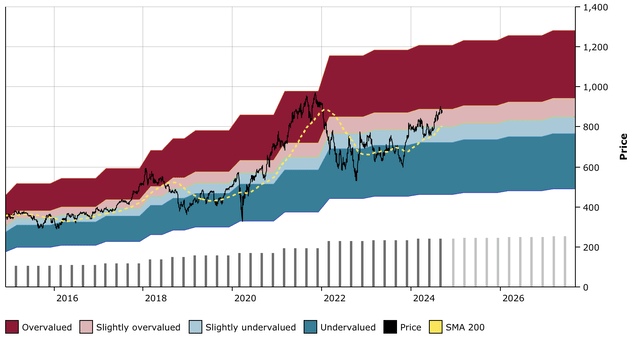

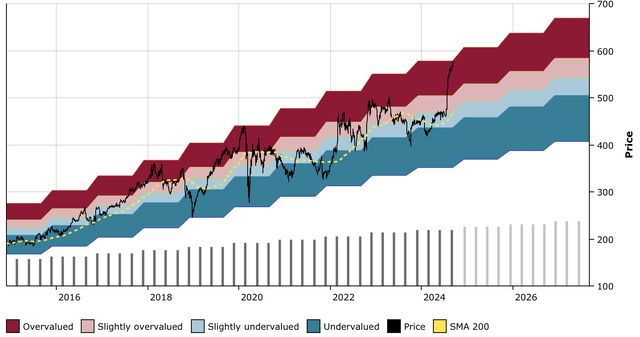

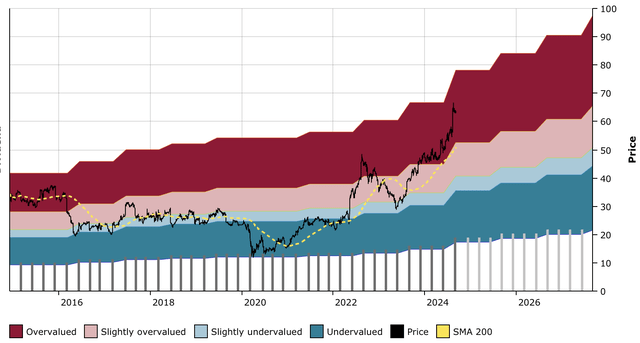

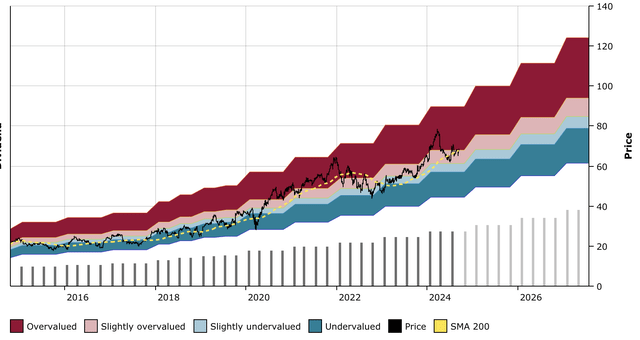

5. Coca Cola

KO has averaged a 5% dividend growth rate this past decade. For a company of such size, that’s not bad.

But everyone is so enamored with the company, probably because of Buffett’s decades of endorsements, that they forget his partner Munger’s quote from above: No matter how wonderful a business is, it’s not worth an infinite price.

KO has yielded 2.7% three times in the past decade. Late 2019, 2022, and now.

KO DFT Chart (Dividend Freedom Tribe)

The past two times, it resulted in 20% drops in price.

Remember what Howard Marks said, returns are a function of price more than of the asset, and no matter the entrenched moat, the beautiful business, and the fanbase, buying today is probably not setting you up for success, despite the likes of Morgan Stanley remaining bullish. My take is they are just chasing momentum, and are late to the party.

I’d avoid buying KO here.

Conclusion

These five stocks which we can argue are very untimely purchases, make up 8.5% of the SCHD.

This is part and parcel of investing in ETFs. you get a mixed bag, some good, some OK, some bad.

I personally prefer to pick stocks and only buy those I believe are good. And don’t get me wrong, the SCHD has a lot of good, and I’ll follow up soon with an article with the five best buys from the SCHD.

Happy Investing!

Read the full article here