Investment Thesis

My first bullish thesis about ServiceNow’s (NYSE:NOW) stock aged well because it rallied 27% since it went live in March. But there was a recent weakness, and it might look like my second call did not age well because NOW underperformed the broader market since July 19. Today, I would like to explain that the recent weakness in the stock’s performance was due to external factors and the overall weak stock market sentiment, but not due to the company’s fundamentals. It is actually vice-versa because NOW’s fundamentals are improving even in the current unfavorable environment with several macro headwinds. The management continues successfully delivering stellar revenue growth, profitability improvement, and massive reinvestments in innovation. The valuation also looks very attractive, according to my analysis. All in all, I reiterate the “Strong Buy” rating for ServiceNow.

Recent Developments

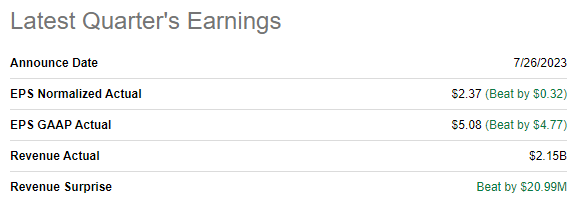

The latest quarterly earnings were released on July 26, when the company topped consensus estimates. NOW demonstrated staggering revenue growth momentum with a 22.7% YoY increase. Profitability metrics followed the topline with a slight YoY rise in the gross margin and a notable expansion in the operating margin. As a result, the adjusted EPS demonstrates substantial YoY expansion from $1.62 to $2.37.

Seeking Alpha

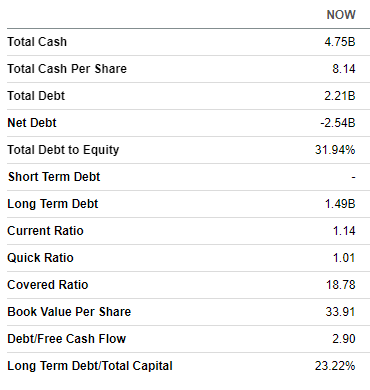

The company generated $559.4 million in the levered free cash flow (FCF) and continued improving its balance sheet. As of the latest reporting date, NOW had almost $5 billion in cash, and the net cash position is also very solid at $2.5 billion. The leverage ratio is very low, and current liquidity is in excellent shape. The company’s fortress balance sheet makes it well-positioned to fuel further growth and innovation in-house or via acquisitions.

Seeking Alpha

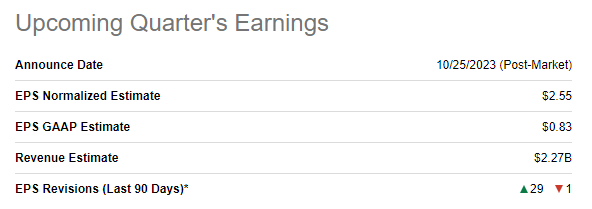

The upcoming quarter’s earnings are scheduled for release on October 25. Revenue growth momentum is expected to sustain since quarterly revenue is projected by consensus at $2.27 billion, which means a 24% YoY growth. The adjusted EPS is expected to follow the top line and expand notably from $1.96 to $2.55. There were 29 upward EPS revisions over the last 90 days, which is also a solid bullish sign indicating the management’s confidence in the company’s near-term financial performance.

Seeking Alpha

I like how the company navigates the current challenging environment. NOW has consistently delivered double-digit revenue growth over multiple years, which is staggering. The pace of the adjusted EPS expansion is also impressive, and the company very rarely misses revenue forecasts and never missed EPS projections since 2018, at least.

Seeking Alpha

ServiceNow is an obvious rockstar in its niche, and the company can charge premium fees and generate stellar profitability. The customers’ loyalty is very impressive. Over the past five quarters, the renewal range was very narrow, between 98-99%. The company’s end-to-end platform provides a suite of comprehensive digital transformation solutions, which gives NOW vast cross-selling expansion opportunities. The expansion of key metrics measuring the monetization of customer relationships demonstrates impressive dynamics.

NOW’s latest earnings presentation

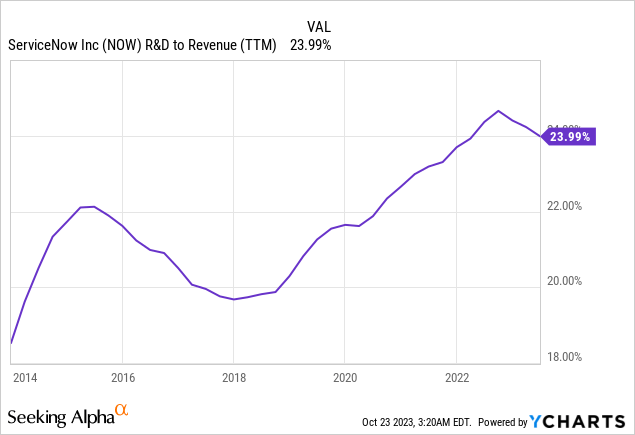

Having high customer loyalty helps companies to build massive brands, and customers become less price-sensitive. This can potentially significantly increase the company’s pricing power, which will ultimately result in the expanded profitability of NOW. This is a strong bullish sign that the management is unwilling to stop the platform’s development since the R&D to revenue ratio is still very high as the company continues to reinvest about a quarter of its sales to innovation despite rapid scaling up.

Valuation Update

The stock rallied 41% year-to-date, significantly outperforming the broader U.S. market. Seeking Alpha Quant assigns the stock a very low “D-” valuation grade because ratios are substantially higher than the sector median. On the other hand, NOW is a profitability superstar, and we should better compare it with historical averages. From this perspective, the stock looks undervalued because current ratios are double digits lower than 5-year averages across the board.

Seeking Alpha

Apart from stellar profitability, NOW also demonstrates impressive growth in its key financial metrics. Therefore, I must proceed with the discounted cash flow (DCF) simulation. I use a 10% WACC for discounting. Revenue consensus estimates project a 16% CAGR for the next decade, and I consider it conservative enough for my DCF. I use the 16% TTM FCF margin for the base year and expect the two percentage points yearly expansion.

Author’s calculations

According to my DCF simulation, the business’s fair value is nearly $150 billion. This is about 35% higher than the current market cap, and the upside potential looks very attractive. My estimation for the stock’s fair price is $730.

Risks Update

While the company demonstrates stellar performance, which is indicated by massive revenue growth and solid profitability expansion, the macro environment looks harsh. The company’s top line demonstrates resilience with its consistent double-digit revenue growth over multiple quarters in a row. But in the short term, stock price heavily depends more on emotions and market sentiment rather than fundamentals. That said, the current sentiment in the stock market looks pessimistic. The reasons are on the surface: Declining corporate profits of major American corporations, high interest rates, expensive oil, and massive levels of uncertainty in terms of global geopolitics. All these unfavorable factors adversely affect valuations as investors’ fear level increases. As an aggressive growth company, ServiceNow’s valuation can also suffer despite demonstrating strong financial performance.

Potential investors also should be aware that the stock is highly volatile and might experience significant swings in the price. For example, NOW reached its all-time high of almost $700 in October 2021, and within the next 12 months, the stock price more than halved due to a general weakness in the stock market caused by high inflation and the war in Ukraine, which commenced in early 2022. That said, investors considering investing in NOW should be ready to tolerate substantial volatility and hold the stock over multiple years.

Bottom Line

To conclude, ServiceNow is still a “Strong Buy”. Despite recent weakness in the stock price performance, the company’s fundamentals are still improving notably. Revenue growth momentum is strong, and key operating metrics also demonstrate impressive dynamics. The management is in a “pedal to the metal” mode in terms of driving further innovation and platform improvement. Lastly, my valuation analysis suggests that the stock is massively undervalued.

Read the full article here