QOE Capital Co-Authored by Analyst Sally Ma

Thesis

SM Energy Company (NYSE:SM) specializes in independent oil and gas exploration and production. With its long-standing and principled approach to its business, SM is a premier operator of top tier oil and gas assets. Our analysis indicates that SM is currently undervalued with a target price of $60.13 where the current trading price is $43.66 (7/01/2024), representing a 37.72% upside potential.

Company Overview

SM Energy Company has been doing business for more than 100 years as an independent exploration and production company that was formed in 1908. The company started in St. Mary Parish, LA for just 17,800 acres of land. With various leases and consolidations in the 1900s, the company changed its name to St. Mary Land & Exploration Company and was successfully listed on NASDAQ in 1992. It wasn’t until 2002 when the company transferred its public listing to the New York Stock Exchange under the ticker SM, leading to the company’s name today. Currently, the company is headquartered in Denver, Colorado with a focus on hydrocarbon exploration.

The company now operates in both the Midland Basin and Southern Texas, seeking innovative ideas to optimize capital efficiency, performance, and reduce impact on shared natural resources. Operations in the Midland Basin are considered as the best-in-class, known for its rich petroleum, natural gas, and potassium deposits, while Southern Texas offers significant economic hydrocarbon accumulations that are yet to be discovered. As oil and gas are essential resources to make everyday life possible, the company is currently present in products varied across home and lifestyle, wardrobe and textiles, recreational and safety products, medical equipment and pharmaceuticals, and emerging technologies.

Qualitative Analysis

As demand for natural resources continues to increase, the positioning of SM Energy Company becomes increasingly essential every day. Hence, to better understand the current industry situation, we have performed an analysis of the competitive forces:

Threat of New Entrants:

Despite the rising demand and volatility involved with natural resources, this industry still maintains a natural technical barrier for new entrants, hence a high barrier to entry. The oil and gas industry typically requires a substantial amount of capital investment for exploration, drilling, and production development. New entrants will also face strict regulatory requirements in regards to environmental impact, safety standards, and leasing permits, which can also be costly.

With established companies such as SM Energy Company, it can greatly benefit from economies of scale by already having existing relationships with drilling operations, technology adoptions, and access to resources. This results in competitive cost advantages when compared to new companies. As one of the earliest companies to enter this industry, it sure builds reputable business opportunities that others cannot compete with.

Threat of Substitutes:

The threat of substituting companies within the industry is relatively low. One reason is for the one mentioned above with a long-established brand image and services over the past decades, we believe SM Energy Company will be able to uphold its relationships and business standards. However, we cannot ignore other industry competitors that already exist within the market.

On the other hand, substitutes to oil and gas natural resources are increasingly popular. With the current society trend for green renewable energy, other sources such as solar, wind, and biofuels are becoming non-negligible challenges as technology advances and environmental concerns grow. At the same time, all natural resources face the problem of availability and affordability. This will determine the extent of the threat to traditional gas and oil products, as well as government regulations. As volatility in commodities is inevitable, the company can consider expanding its services into alternative energy.

Bargaining Power of Suppliers:

Suppliers within this industry usually consist of specialized drilling equipment, hydraulic fracturing services, and other technology intensive services, which have high bargaining power. Due to their expertise and limited competition, the suppliers hold significant bargaining power when it comes to collaborating with oil and gas companies. Also for their limited competition, it increases the competition among existing companies for better terms of contract. We believe that SM Energy Company has already established and is able to maintain long contracts with existing suppliers, eliminating some concerns.

Bargaining Power of Buyers:

Since bargaining power of suppliers is high, bargaining power of buyers is only moderate when compared. Depending on the market conditions and volatility, buyers of commodities can have very different bargaining powers as the negotiation power is largely affected by the prices of oil and gas, which is influenced by global supply and demand dynamics, geopolitical conflicts, and economic conditions.

Over the past few years, market volatility and uncertainty have been quite high with instability in the Middle East, greatly affecting market prices of commodities. Although this risk still remains big today, market conditions have become more stable recently, and we believe that the company can mitigate this issue with long-term supply contracts or partnerships while still having leverage power in negotiating prices and terms.

Existing Competition:

Despite the difficulty for new entrants, existing rivalry remains high. The industry is very competitive with numerous companies vying for market share in key regions like the Permian Basin, Eagle Ford, and Bakken formations, where SM Energy Company operates. These companies mainly compete on product efficiency, technological innovation, and operation excellence for lower costs and high profitability during price fluctuations.

As we have been seeing with the history of SM Energy Company, mergers and acquisitions within this industry is not uncommon. Such consolidations within the industry can intensify rivalry as larger entities merge together to create greater market power and economies of scale. As a result, we encourage the company to seek out strategic potential merging benefits to eliminate potential competition within the industry.

Main Investment Points

Sustainable Long-Term Capital Structuring

Similar to fiscal year 2023, SM Energy Company has laid out multiple objectives to reach for 2024. With the success and outperformance over the 2023 year, we are optimistic about the company in accomplishing future goals.

Over the past year, the company was able to increase return of capital to stockholders while maintaining a strong balance sheet. The increased return of capital generated $300M return to stockholders, $125M to acquisition capital, and $171M in reduction of net debt. This resulted in a 7% annual yield to market capitalization while decreasing the amount of debt to less than $1B (non-GAAP) and 6.9M shares repurchased in 2023.

Having a healthy financial performance is crucial for a company like this who faces a lot of market risk, and this balanced approach to long-term profitability is exactly helping mitigate those risks. At the same time, the company also focused on capital efficiency and operational execution through accelerated completions. Going forward, the company continues to build top-tier inventory to apply differential strengths in geosciences which began with the acquisition in the Midland Basin, increasing its position by 37%.

These prominent goals have helped SM Energy Company to exceed its competitors and peers, which acts as an important stepping stone in 2024 and going forward.

Successful Expansion in Dawson County

In 2023, SM Energy Company entered an agreement for the acquisition of 20,000 net acres of land in the Dawson County and northern Martin Counties to expand its success from Q2 2023 by increasing its drilling and completing activities in the future.

According to Enverus Intelligent Research, horizontal well completions in the Dawson regions have increased about 5x over the past three years when compared to previous years. To continue this, the company started targeting a northern Middle Basin step out with a 90%-plus oil-weighted Dean Formation overlying the similarly oily Wolfcamp A. Total production in the areas was up nearly 12% from the previous year quarter, demonstrating potential. This helped the company in exceeding its expectations for 2023, hoping to remain well positioned for a positive trajectory in 2024.

SM Energy Company has proven its ability to expand strategically, helping them to enhance operational efficiency and healthy balance sheets. As mentioned earlier, being able to expand can help reduce existing rivalry while augmenting competitive advantage. Hence, we expect to see this positive growth through 2024 in line with strategic objectives in expanding portfolio quality and depth.

Valuation

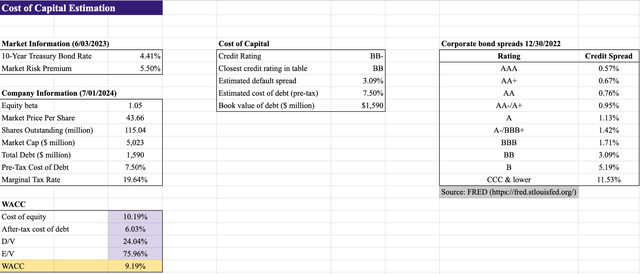

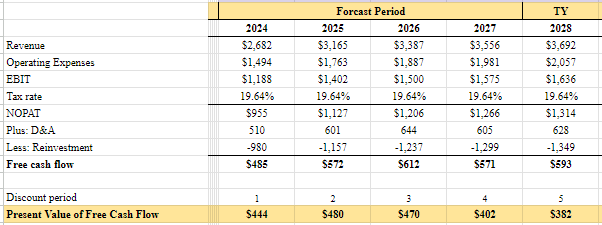

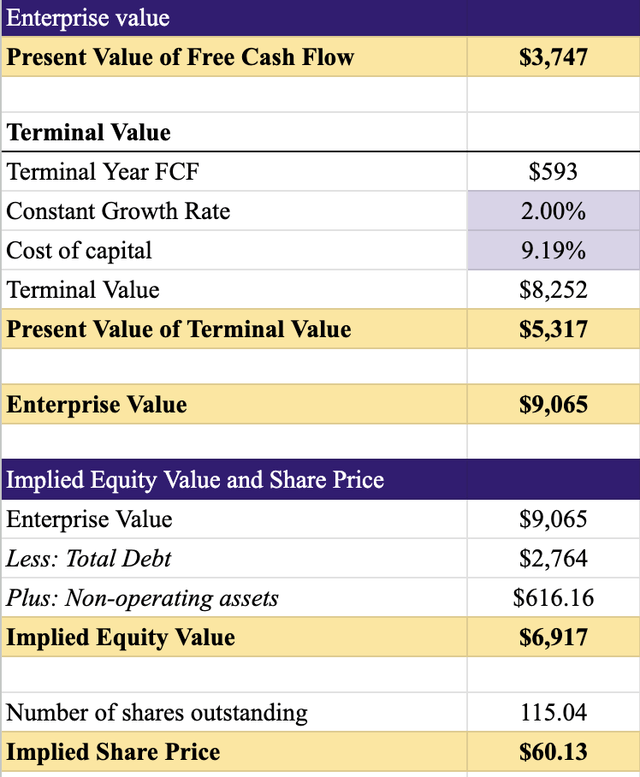

In order to combine and leverage and driving points mentioned above, a DCF valuation model was performed with a forecast period of five years (2024 – 2028) with historical data over the past five years (2019 – 2023).

Using the information as of 7/01//2024, we have derived a WACC discount rate of 9.19%. The beta calculation was derived from historical performance returns of the market and SM Energy Company with a linear correlation to assess how the company’s movement correlated with the market. As we took consideration of the pandemic, we looked at years 2021 – 2023 and arrived at a beta of 1.05, which is close to the market beta.

QOE Capital

SM Energy Company management released some expectations for the company’s 2024 revenue to be estimated around $2.5B. From there, with the growth calculations based on reinvestment, an initial growth rate of 13% was applied to 2024, linearly interpolated to the terminal growth rate. We believe that the terminal growth rate is reasonable due to the rising amount of opportunities available from diversification and expansions, leading to a 2% constant growth rate going forward. Moreover, we believe that the energy and natural resources industry will remain popular and with high demand in the next few years. As a result, the DCF arrived at a final trading price of $60.13, representing 37.71% upside.

QOE Capital QOE Capital

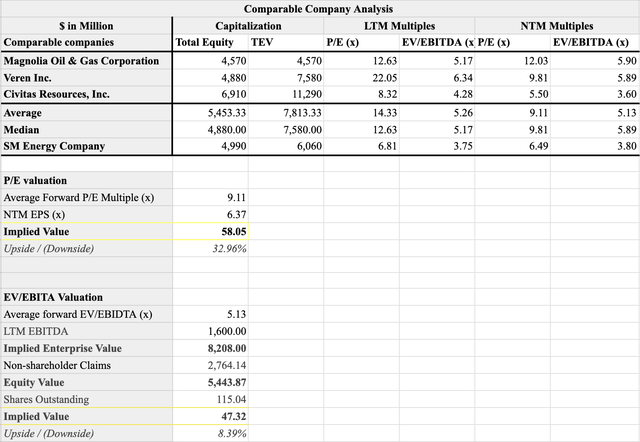

As we have mentioned earlier, SM Energy Group faces fierce competition from substitutes and existing competitors. Thus, we identified three competitors within the same industry to compare its performances: Magnolia Oil & Gas Corporation, Veren Inc., and Civitas Resources, Inc. From both the P/E and EV/EBITDA valuation, we see an upside implied trading price for SM Energy. Although not as much from the DCF, it still indicates that the company is currently undervalued as compared to industry peers. Once again, supporting our thesis of ‘buy’.

QOE Capital

Risks

Commodity Market Risk

Similar to many other companies within the gas and oil industry, SM Energy Company faces strong risks associated with commodity price volatility. The prices of crude oil, natural gas, and natural gas liquids (NGLs) are highly volatile and influenced by global supply-demand dynamics, geopolitical events, economic conditions, and weather patterns. As we have been seeing impactful geographic instability over the past few years, any changes in the government policies (domestic and international) can greatly impact the global energy markets. Fluctuations in prices can significantly impact SM Energy’s revenue and profitability.

We recommend the company to utilize hedging strategies to minimize the negative impact of price fluctuations. For example, using various financial derivatives like futures and options to control risk exposure. Also, SM Energy Group can aim for a diversified portfolio and greater control over the supply chain to maintain its competitive advantage. As mentioned above, the company can consider expanding into more environmentally friendly natural resource industries to minimize industry risk and market risk.

Green Energy Trend

Recently, consumer attention has been rising in sustainability and finding alternatives with environmentally friendly products and companies. This shift, if possible in the long run, can hurt SM Energy Group if more customers shift towards green energy companies such as solar, wind, or biofuels. This heightens the number of competitors, not just directly in the same industry, but broadened to all energy companies. For example, Vestas as a global leader in energy sustainable solutions and Siemens Gamesa in global renewable energy.

Over the past few years, we can also see the government pushing forward for climate change. As President Biden promised in his campaign, the passing of the Inflation Reduction Act in 2022 pledged $369B in climate investments over the upcoming decade. This includes goals of reducing carbon emissions and greenhouse gas emissions. Solar company, First Solar, donated at least $2M in helping Biden’s presidential campaign. In return with this bill, the company’s stock price has doubled with profit soaring due to government subsidies in relevant fields. We can exactly see here how green energy companies are benefiting from societal concerns and government regulations, which in turn is hurting companies like SM Energy. This once again highlights the importance of diversification that we recommend.

Conclusion

Our final recommendation for SM Energy Company is ‘buy’ due to rising demand in natural resources and shifts towards green energy that we hope the company will benefit from. When investing in the company, it is important to analyze both catalysts and risks, especially in an industry that is very volatile with global events. Sometimes, if the right actions are taken, risks can turn into great investment and growth opportunities for the company. Therefore, we expect to see positive trends in the future.

Read the full article here