The Trade Desk (NASDAQ:TTD) is one of the leading technology platform providers for advertisers and ad agencies to purchase digital ad inventory. TTD is rapidly becoming the key independent marketplace for entities other than behemoths like Google (GOOGL) (GOOG), Meta/Facebook (META), and Amazon (AMZN) that have the capacity to develop their own ad platforms and also service the marketplace, as is the case with Google’s DoubleClick. The Trade Desk appears likely to remain an important independent marketplace, and also one that is likely to benefit from the growing market for ads on streaming services offered by traditional media producers, as well as Netflix (NFLX).

The Trade Desk’s business model is to assist ad buyers in buying and managing ad campaigns within the digital marketplace. As such, it should benefit from the continued increase in spending on digital advertising. The Trade Desk does not own any media or websites that service ads, as opposed to the primary competitor in this market, Google’s DoubleClick, which services third-party websites and content creators, as well as its own sites such as YouTube and Google Search. Similarly, Amazon has its own advertising platform.

The Trade Desk is the primary independent marketplace, and a key choice for entities that do not want to give companies like Google and Amazon valuable data on their advertising. This would include issues such as an awareness of what products are gaining traction and interest from consumers, and which may allow for a company like Amazon to enter that market, and subsequently promote its own competing brands.

The Trade Desk’s client base continues to grow over time, as the Internet grows, as well as due to the addition of ad servicing on many streaming services that were previously commercial free. Similarly, TTD’s revenue per client/customer continues to increase over time, and has almost tripled over the last five years. This growth appears to be based on multiple factors, including growing spending on digital campaign, but also TTD’s improving capacity.

One of the key capabilities that The Trade Desk developed is similar to that which Meta and Google also had to develop following Apple’s (AAPL) decision to initiate privacy policies that substantially limited third parties from recognizing any personally identifiable information from users on iOS. These large players had to develop workarounds that would facilitate their own user identification capabilities. The Trade Desk’s development of its proprietary user identifier, UID2 (or UID 2.0), was a costly initiative, but one that places it amongst the few independent entities with such a capability. Most competitors with such capacities are within the mega-cap technology space, such as Google and Meta.

The Trade Desk continues to grow, and in the second quarter of 2024 it reported sales that were about 26% higher than in the same quarter a year earlier. Further, TTD’s outlook for the third quarter anticipates a similar level of year-over-year growth. A key component to TTD’s revenue growth this year is advertising on streaming services.

The Trade Desk has developed partnerships with many large production houses and streaming services, including Disney (DIS), Netflix, and NBC’s Peacock, as well newer digital streaming companies such as Roku (ROKU). Some of these services did not initially include ad-supported streaming, such as Disney+ and Netflix, but added those choices in the recent past and are seeing growing subscriber bases for their lower priced choices that are ad-supported.

Since these companies offer premium content, their growth is likely to yield higher than average ad pricing for TTD. This should mean that TTD’s revenue per client is likely to continue to increase, as advertisers are likely to select ads on the higher cost and higher quality programming that has been added to The Trade Desk’s inventory from these premium streaming services. This should result in increased revenue growth, and also potentially yield increased margins.

While it is difficult to project future margins on a subset of advertising inventory, what is clear is that advertisements placed within video streaming services like Netflix and Disney+ are more likely to include specifics upon the viewer, or at least the household. This factor makes those ads more valuable. Similarly, these applications are a key driver of the usage and growth within the connective TV marketplace, which continues to take share from traditional broadcasting. Further, due to the real time targeting of identifiable potentially valuable customers, or their households, connective TV marketing is more lucrative for publishers and companies like TTD, which estimates that connective TV’s CPMs average about $20, while traditional broadcast TV has a $10 CPM.

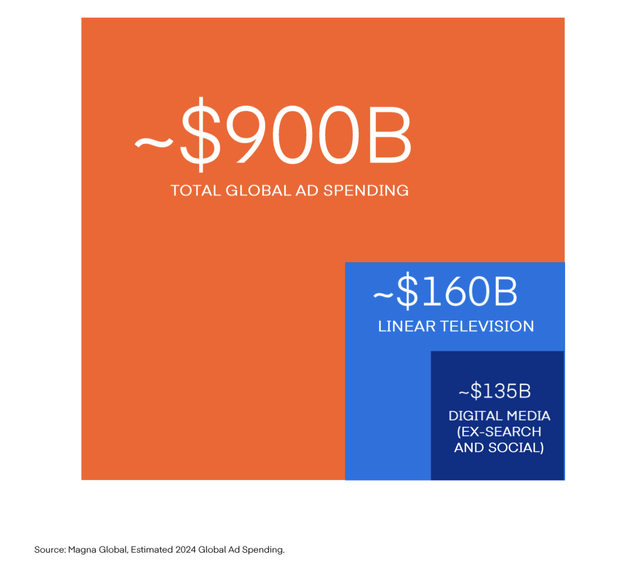

Other reasons why advertisers are likely to prefer connective TV advertising on premium streamers include attribution across devices, resulting in clearer data on impressions delivered, as well as frequency and, in many cases, video completion rates. At the moment, the total digital media advertising market, excluding search and social, is about $135 billion, while traditional linear television ad spending is about $160 billion.

Digital versus linear TV and total ad market (TTD’s Q2 2024 earnings presentation)

Over the next few years, this digital market is likely to surpass the traditional one. This should happen due to both the growth of streaming viewership, and especially on ad-supported premium streaming services, as well as the higher average cost per view for these targeted ads.

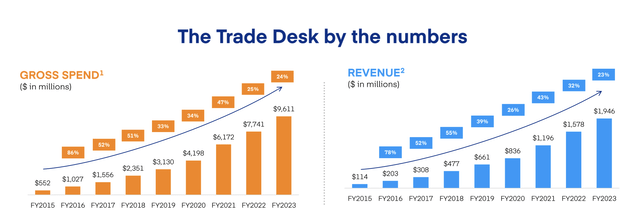

Given TTD’s last reported revenue of $585 million and that it expects to generate $618 million or greater in the third quarter, TTD will effectively bring in as much revenue in these two quarters as it did in all of 2021. While this rate of growth is unlikely to sustain for an extended period of time, even if we place a conservative 10% growth rate on TTD’s revenue over the next five years, its revenue would be over $3 billion annually.

TTD revenue and market totals (TTD’s Q2 2024 presentation)

Nonetheless, TTD grew by about 23% last year and appears to have the capacity to grow its revenue by a level close to this over the next couple of years. If it can sustain 20% growth over each of the next two years, that would result in essentially adding as much revenue as the company totaled in 2021. Moreover, TTD has reasonably strong profit margins, which it should be able to maintain or even potentially increase due to higher value premium ad-supported streaming. Last quarter, TTD realized adjusted EBITDA of about $242M, resulting in a margin of 41 percent. If TTD’s growth and margins can maintain such projections, which may be conservative, the company may then be revalued to over $200 per share, or essentially doubling.

Technicals

TTD shares appear to be on the verge of breaking out of a trading range where shares have remained for most of 2024. This trading range was basically between $80 and $105 per share. Shares have spent most of the last few months at the top of this trading range, but fell all the way to support at the start of August. Since then, shares have returned back to upward resistance, and appear likely to soon break out of this range.

TTD’s daily candlestick chart (Finviz.com)

If TTD shares can move higher from here, it also appears reasonably likely that a level around the $100s will become support. This is primarily premised upon shares remaining in a tight trading range around $100 for most of the summer, other than the brief time it spent testing support in early August. If Shares were to fall from here, and decline through the high $90s, it may then be the case that TTD shares would likely re-test support around $80, but the more probable move here seems to be it breaking out to the upside.

Risks

The Trade Desk’s risks include that it faces competition from companies that are larger and highly capable of competing, such as Google and Amazon. Google’s DoubleClick remains the largest platform for servicing ads on websites, and Amazon’s capabilities are not to be underestimated. Beyond competing for business, these mega-cap entities are also able to undercut advertising pricing and potentially sustain a prolonged period of losses in an effort to thwart competition. Nonetheless, current government scrutiny indicates that these companies are unlikely to do anything so dramatic in the near term as to eliminate competitors like TTD, and may actually be forced to lessen their competitiveness in the future.

Another concern is that some of its larger partners could develop their own in-house capabilities. The largest such concerns would be from entities like Disney and Netflix, which provide premium content that demands higher priced advertising. Similarly, such partners could be lured to a new competitor that offers them better pricing. Such outcomes appear unlikely in the near term, but this landscape is subject to change at the pace of technological advancement.

Conclusion

The Trade Desk is the main choice for an independent advertising marketplace, and one that has entered valuable partnerships with several of the larger and higher quality streaming content providers. The current government scrutiny of Google makes it unlikely that DoubleClick will be able to thwart competition like TTD. Google may even have to come to an agreement where it becomes less capable of retaining its dominance within the digital ad marketplace. Amazon may be similarly stifled from becoming too powerful of a competitor within this space.

Premium content providers appear likely to prefer working with TTD rather than companies like Google and Amazon, since they are also competitors. As a result, it appears TTD’s probable revenue growth, and particularly from premium ad-supported streaming services, is underappreciated by the marketplace. The Trade Desk’s valuation should appreciate as the market comes to recognize the strength of TTD’s platform, and the partnerships it recently forged.

Read the full article here