Weyco Group (NASDAQ:WEYS) is a shoe designer and wholesaler. The company owns six brands focused on men’s leather dress and casual (Stacy Adams, Nunn Bush, Florsheim) and winter and outdoor boots (Bogs, Rafters, Forsake).

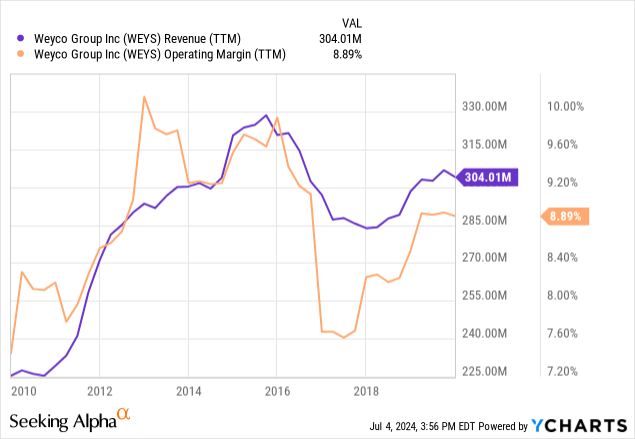

The company’s revenues and profitability have stagnated for much of the past decade as the casualization of men’s apparel has eaten into its dress-oriented leather shoes. Like most wholesalers, the company benefited and then suffered from the pandemic’s inventory crisis and posterior glut. However, despite falling sales, the company has maintained gross and operating margins while remaining competitive in the market.

Today, Weyco trades at an EV/NOPAT multiple that implies a sufficient return under a scenario of pre-pandemic profitability. However, the company is posting higher profits despite having lower sales than before the pandemic, meaning the current profits might be more permanent than thought. If that is the case, the multiple could reprice upward. Further, the retailers to which Weyco sells might start recomposing their inventories soon, potentially increasing the company’s revenues. For those reasons, I believe Weyco is a Buy at these prices.

Company intro

Channels: Weyco is a shoe wholesaler. The company designs the products, manufactures them with suppliers in Asia, and resells them to retailers via a salespeople team. 80% of sales come from wholesale, about 12% are DTC via e-commerce websites, and the remaining 8% comes from wholesale sales in Australia and APAC.

Brands and products: The company has two groups of brands: men (called legacy) and outdoors. The legacy brands are Florsheim, Stacy Adams, and Nunn Bush. These brands represented 80% of wholesale in FY23.

The three brands were created in the early 20th century and enjoyed a period of good quality reputation. For example, the Florsheim Imperials are sought after in vintage markets, whereas the Stacy Adams were very in vogue in the black communities of the Midwest between the 1960s and 1990s.

However, today, these brands compete in the cheaper categories of leather shoes, loafers, and hybrid casuals. They retail for $50/$70 for casuals and $80/$120 for leather shoes. They enjoy some of the renown of the past but are commodity-type shoes.

The outdoor segment is mostly composed of Bogs, a boot brand with a strong position in the winter and rain boots market. These are not the classical outdoor boots from Columbia, but rather more bulky and durable. They are useful for blue-collar workers and farmers in heavy winter areas.

Stagnant 2010s: During most of the 2010s, the company’s sales and profits were stagnant. This might sound like a negative, but I believe it is actually not so much. The company’s products are relatively dressy, and men’s fashion has moved to casual styles. This means that during the period, the company’s main segment was shrinking, yet Weyco was able to keep its market and profits. Today, the company is more positioned in hybrids.

Pandemic boom and bust

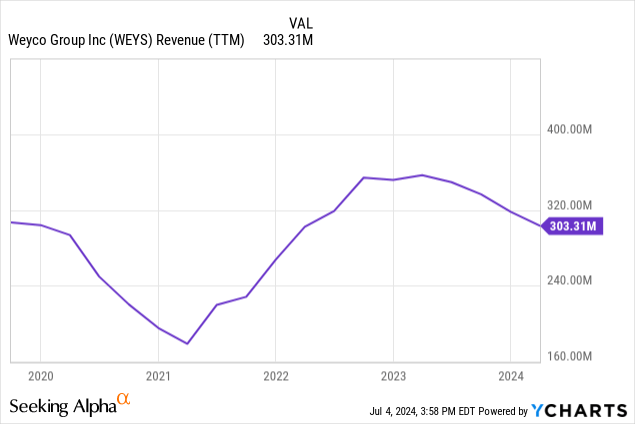

The relatively boring Weyco was obviously moved by the pandemic’s boom and bust that affected all consumer categories. Revenues exploded in 2021 and 2022 as consumers flooded the markets and retailers built inventories, only to retrace fiercely in 2023 and 2024, with wary retailers trying to reduce their inventories.

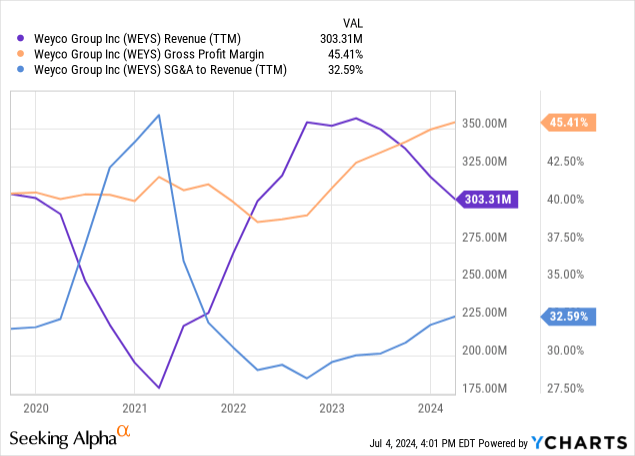

However, Weyco’s is different from other similar stories in that despite falling sales, the company’s gross margins were maintained and even grew. The company was able to raise prices in 2022 with higher freight, but as supply prices receded, it maintained its wholesale prices, so margins expanded. Further, the company’s SG&A structure delivered, but not a lot, given that as a wholesaler, its SG&A structure is smaller than other more retail-focused competitors.

Weyco’s CoGS includes only the products and inbound shipping costs, whereas the distribution center costs are embedded in SG&A. Further, inventories are recorded using LIFO, meaning that recent sales should reflect current market conditions.

Current valuation and expectations

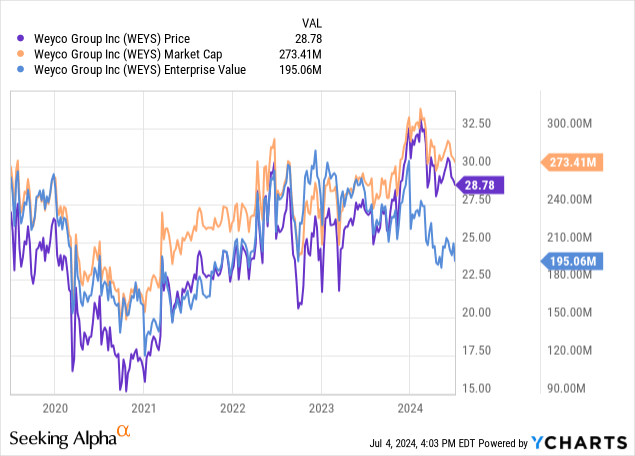

Today, Weyco trades for an EV of $195 million. It has cash holdings of about $79 million plus long-term securities holdings of $6 million, as of 1Q24.

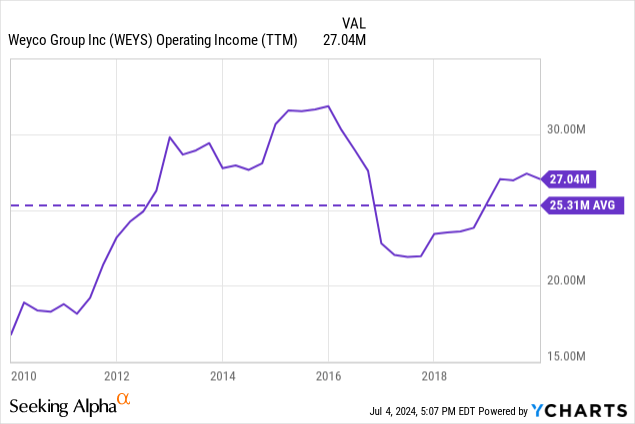

The company’s pre-pandemic average operating income was above $25 million, which after an effective tax rate of 25% imply NOPAT of $19 million. Therefore, Weyco trades at an EV/NOPAT of about 10x, considering the profits it was generating before the pandemic.

However, the company’s current TTM operating profits are about $39 million, or a NOPAT of $29 million. This is an EV/NOPAT of only 6.7x. To me, this implies that the market expects the company’s profitability to move to its pre-pandemic average. The market believes that Weyco’s current profits are unsustainable.

Forward scenarios

As mentioned, one argument against the above ‘return to pre-pandemic’ thesis, is that Weyco’s revenues are already below pre-pandemic levels. Its CoGS, which in part represent volumes sold, are also below 2019 levels. However, the company’s gross margins and operating margins have not delevered substantially.

In my opinion, the probability that normalized profitability is higher than before the pandemic is higher than what is embedded in the company’s stock price.

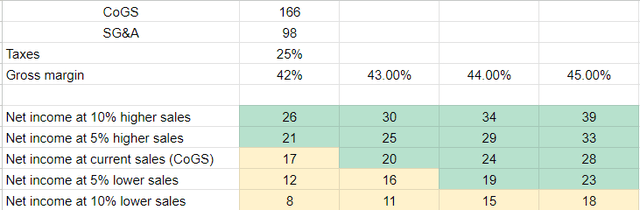

Below is a simple model of Weyco’s profitability, considering CoGS as a variable component and SG&A as a fixed cost component. The model provides NOPAT for different scenarios of gross margins and of sales (measured via CoGS). The green scenarios are those for which the company’s EV/NOPAT multiple is at or below 10x.

Simple napkin model for Weyco (Author)

We can observe that with its current gross margins, the company could continue posting lower sales, as much as 10%, and still generate close to a 10% earnings yield. At lower margins, the situation is different, but the company is relatively well protected from loss scenarios.

For that reason, I believe the company’s stock offers compelling protection against negative scenarios (of continuing decreasing sales and gross margins).

Potential for recovery

The company’s current scenario is very challenging. Q1 sales were down 18% YoY, as they are compared to peak sales in early 2023.

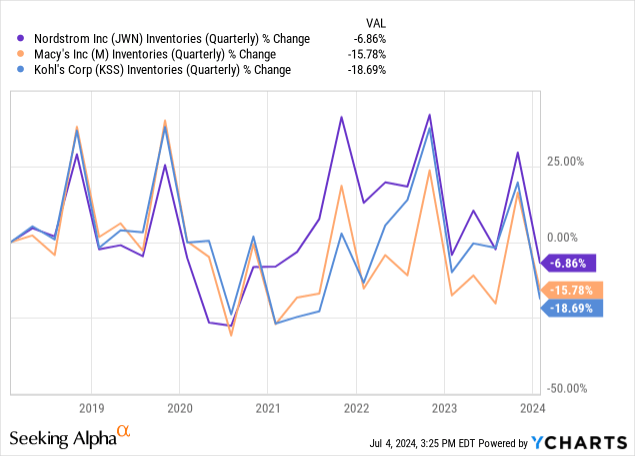

Destocking and restocking: The company’s customers, retailers like Nordstrom, Macy’s and Kohls, have been sharply reducing their inventory purchases in order to clear the excessive inventories they built during 2022, and because they are cautious that 2024 demand will be even slower. The glut has been specially harsh for outdoor products like Bogs boots (sales down 23% in 1Q24), given that customers bought a lot of these products after the pandemic and retailers overestimated future demand. The outdoors market is saturated.

However, as seen above, the inventories of some of the large retailers carrying Weyco’s products are below pre-pandemic levels, and getting close to the shortage levels of 2020/21. Of course, these inventories are not only shoes, but they indicate that a restocking cycle might be close. Even if retail demand does not recover, eventually the retailers will need to stock at pre-pandemic levels to maintain adequate supply.

End demand: Weyco’s management commented on the latest call and on FY23’s 10-K that they believe end demand for their products is healthy. The problem, they say, is that retailers are still cautious.

I believe there are signs of this healthy end demand. For example, if you visit the webstores for Kohls’ casuals or leather shoes, you will see Weyco’s products ranking high. The same is true for Zappo’s loafers and leather shoes. Weyco’s prices are very competitive with other brands in the same segments.

Further, the company’s online sales have been growing, 4% in FY23 and 10% in 1Q24. This is consistent with upward trends in traffic, according to Semrush, for Stacy Adams, Nunn Bush, and Florsheim.

Conclusions

In my opinion, the market is overdiscounting the problems Weyco will face in the future. The stock is adequately priced for scenarios that imply lower margins and/or lower sales, meaning it provides a margin of safety. The company’s close to $80 million in cash reserves provide more help in this respect. Further, the stock is undervalued considering both a neutral scenario (with sales stabilizing in 2H24) or positive scenarios, with recoveries in wholesale. This provides for an opportunity. For that reason, I consider Weyco is a Buy at these prices.

Read the full article here