Introduction

It’s time to talk about what has become one of my all-time favorite dividend growth stocks: Carlisle Companies Incorporated (NYSE:CSL).

The company was added to my portfolio in May 2023 and is already one of my biggest winners, having returned 95% since then – excluding dividends.

On May 15, 2023, I called the stock an “Underappreciated Dividend Growth Stock,” hinting at its subdued valuation. Back then, the stock traded at just 12x free cash flow.

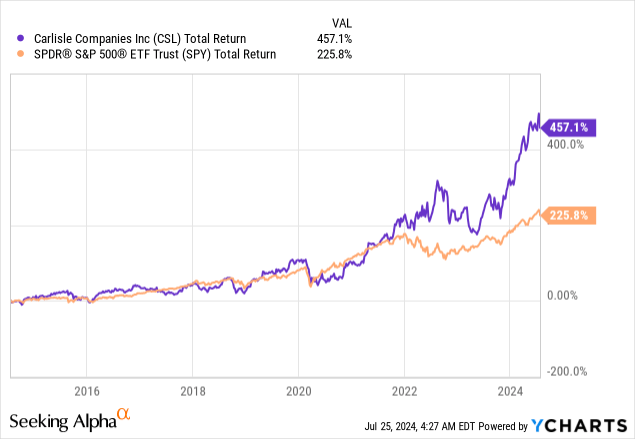

The ten-year total return of the company is now close to 460%, beating the S&P 500’s stellar return of 226% by a wide margin.

My most recent article on this stock was written on April 28. Back then, I called it a “Soon-To-Be Dividend King With Tremendous Return Potential” in the title.

Now, I’ll update my thesis using its just-released quarterly earnings. These numbers not only confirmed my bull case but also highlighted the company’s extreme resilience in what has become a tough spot for cyclical companies.

So, as we have a lot to discuss, let’s get right to it!

The “Golden Age” For Commercial Building Maintenance

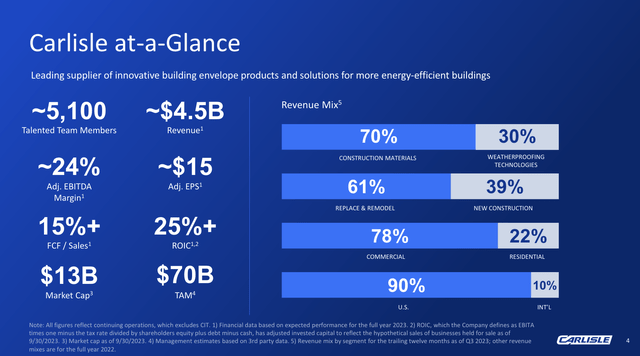

As I wrote in my most recent article, Carlisle has become a pure-play construction materials provider. Roughly 70% of its revenues come from construction materials, followed by weatherproofing technologies.

Most of these products are sold for remodeling/maintenance projects for commercial properties in the United States.

Carlisle Companies

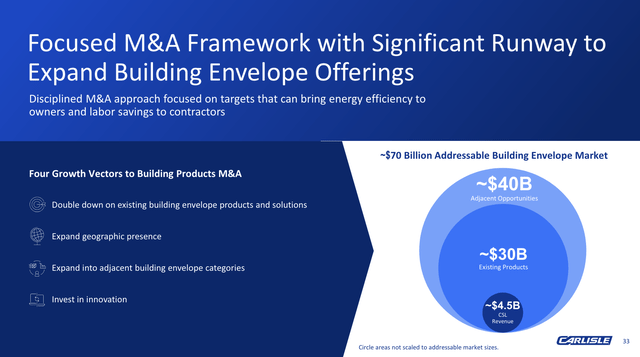

The company estimates it is dealing with a total addressable market of $70 billion, where it currently has a footprint of less than 7%.

Through both organic growth and strategic M&A, the company wants to capture a bigger piece of this pie.

Carlisle Companies

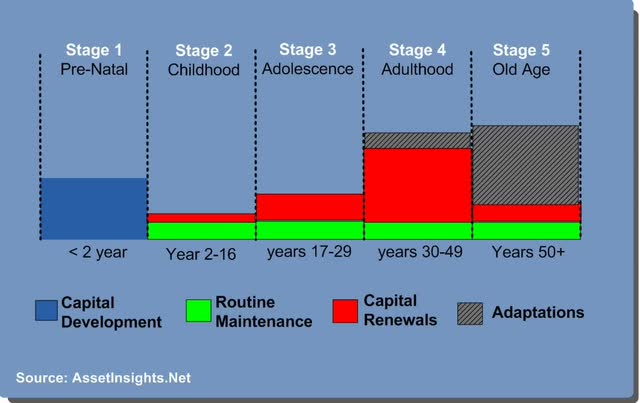

One fascinating aspect of the commercial building industry is that we may be at the start of the “golden age” of remodeling demand.

As I wrote in a recent article on The Home Depot, Inc. (HD), the average age of a commercial building in the United States was 53 years in 2022. Now, that number is 55 years. The average lifespan of a commercial building is 50-60 years before it triggers a wave of maintenance requirements.

AssetInsights

This massive secular tailwind is now meeting other secular tailwinds, including economic reshoring, which also requires more commercial buildings in the United States to support the expansion and return of major industrial supply chains.

The Home Depot is betting on this trend by buying SRS, a leading specialty trade distributor in the building supplies industry. Meanwhile, billionaire entrepreneur Brad Jacobs founded QXO, Inc. (QXO) to do the same.

Smart money is figuring out just how attractive this market is.

After years of reshaping its business, Carlisle is in a fantastic spot to capitalize on this demand.

Carlisle’s On Track For Long-Term Growth

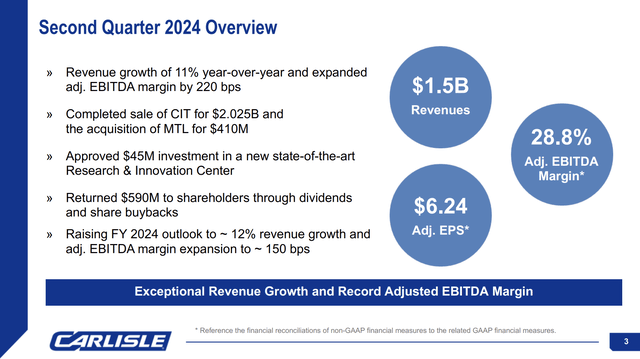

In the second quarter, Carlisle has shown impressive financial numbers, with an 11% year-over-year increase in sales, reaching $1.5 billion.

According to the Phoenix-based giant, this revenue growth is supported by pent-up reroofing demand, a strong start to the construction season, normalizing inventory levels, and operational efficiencies. Even better, the company’s profitability also saw significant improvement, allowing adjusted EPS to surge by 33% to $6.24.

Additionally, the adjusted EBITDA margin rose by 220 basis points to a record 28.8%, which perfectly highlights the company’s effective cost management and pricing strategies.

Carlisle Companies

The company attributes this success to its Vision 2030 growth measures, which aim to push adjusted EPS to more than $40 by 2030, supported by 5% annual organic revenue growth, adjusted EBITDA margins of more than 25%, and a return on invested capital of more than 25%.

As we can see below, this strategy is built on six pillars.

- Continuous improvement through the Carlisle Operating System (“COS”).

- Enhancing the Carlisle Experience.

- Accelerating innovation.

- Strategic M&A.

- Disciplined capital allocation.

- Attracting top talent.

Carlisle Companies

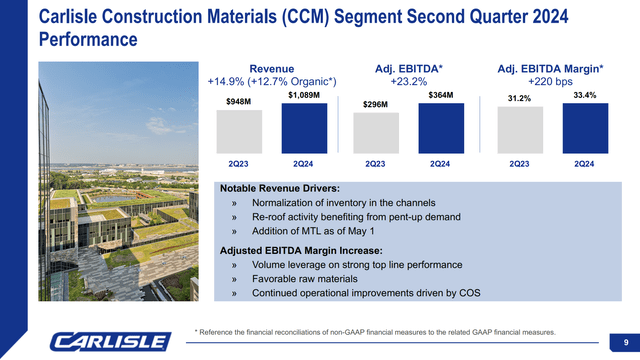

With that said, diving a bit deeper into its financial performance, we’re seeing $1.1 billion in quarterly revenues in its Carlisle Construction Materials (“CCM”) segment. That’s a 15% year-over-year increase, supported by 13% organic growth and the acquisition of MTL.

Carlisle Companies

CCM’s adjusted EBITDA surged by 23% to $364 million, and its adjusted EBITDA margin expanded by 220 basis points to 33.4%. According to the company, this growth reflects the benefits of volume leverage on sales growth, favorable raw material costs, and continuous operational improvements.

With regard to the MTL acquisition, headquartered in Wisconsin, this company positions Carlisle as a leader in the $4 billion architectural metal industry.

We were pleased to close on our acquisition of MTL during the second quarter, adding a tremendous set of assets that provide innovative, high-performance metal edge and wall systems. This addition of MTL aligns perfectly with our Vision 2030 strategy and meets our acquisition criteria. By deploying our Carlisle integration playbook at MTL, we are on track to exceed the $13 million of synergies we announced in May. We now expect to deliver $20 million of annual synergies in year 3. – CSL 2Q24 Earnings Call (emphasis added).

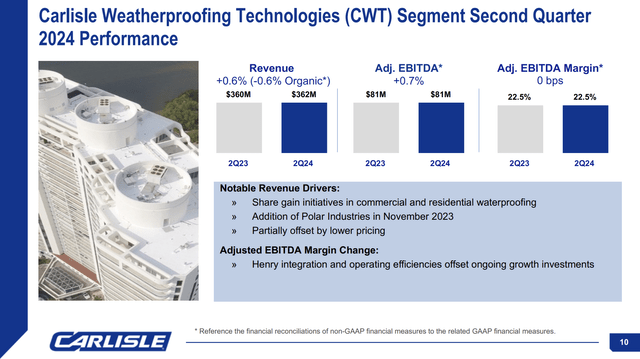

The Carlisle Weatherproofing Technologies (“CWT”) segment was a bit weaker, with a 0.6% contraction in organic revenues. However, the company saw a higher market share, bought Polar Industries in November 2023, and was able to maintain elevated adjusted EBITDA margins.

Carlisle Companies

Moreover, in addition to acquiring growth, the company is investing internally to pave the way for more innovation.

For example, the company’s planned $45 million investment in a state-of-the-art research and innovation center in Carlisle, PA, is aimed at supporting its goal of generating 25% of revenues from new products introduced within five years by 2030.

Additionally, the company believes increasing R&D spending to 3% of its sales by 2030 will support its competitive edge even further.

Great News For Shareholders

One of the company’s strengths is free cash flow generation.

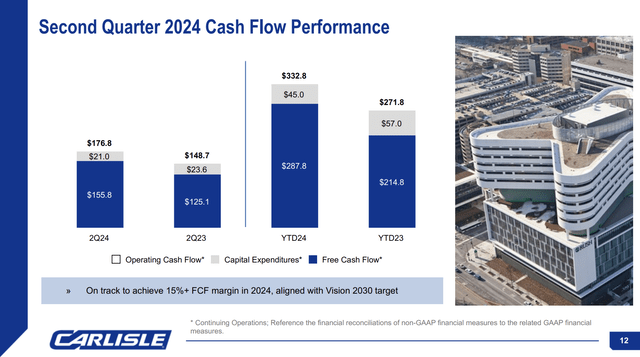

In the first six months of this year, it generated $333 million in operating cash flow, up $61 million from the prior-year period. Capital expenditures came in at $45 million, resulting in a free cash flow of $288 million, which is a $73 million year-over-year increase.

Carlisle Companies

On a full-year basis, it aims to maintain a free cash flow margin of over 15%, which would align with its Vision 2030 target.

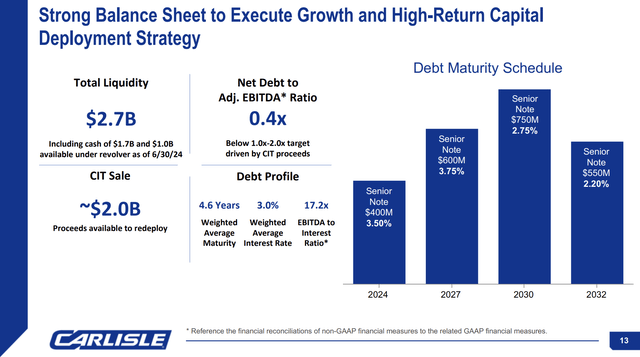

Moreover, strong free cash flow has provided the company with tremendous financial stability.

The company has $2.7 billion in liquidity, a net leverage ratio of just 0.4x EBITDA (below its 1.0-2.0x target range), and a weighted average interest rate of just 3.0%.

Carlisle Companies

So, in addition to having low financial risk, the company does not need to prioritize financial health over shareholder distributions.

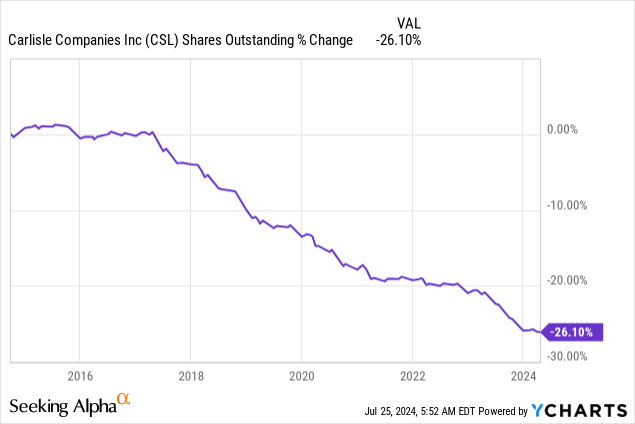

In the second quarter, the company paid $40 million in dividends and bought back stock worth $550 million. Since the inception of its buyback program, the company has bought back more than 26% of its shares.

It also has a fantastic dividend profile.

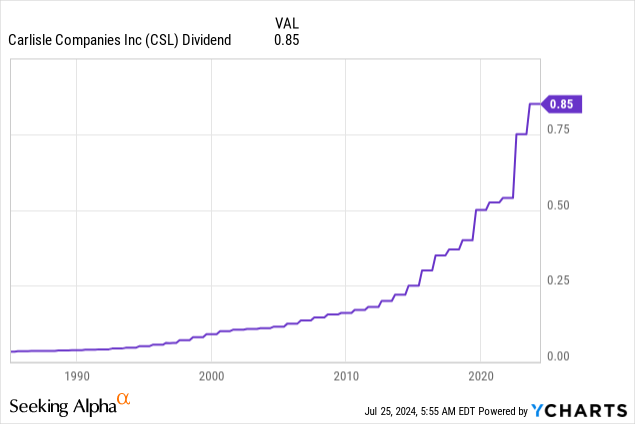

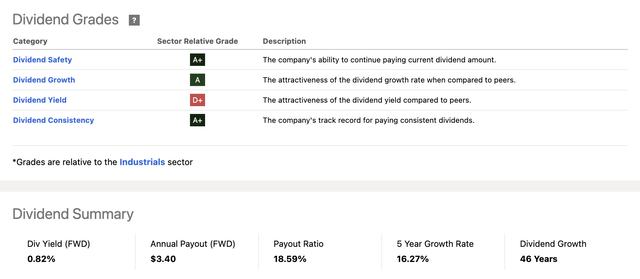

After hiking its dividend by 13.3% on August 3, it currently pays $0.85 per share per quarter, translating to a yield of just 0.8%. The dividend has a payout ratio of less than 20%, a five-year CAGR of 16%, and a track record of 47 consecutive annual hikes.

In other words, the only reason why the CSL yield is still low is because stock price gains more than offset dividend growth.

Hence, the company, which is three years away from becoming a Dividend King, has just one low grade on its Seeking Alpha Dividend Scorecard: its yield.

Seeking Alpha

While a 0.8% yield makes CSL unsuitable for income-seeking investors, the company’s total risk/reward remains fantastic.

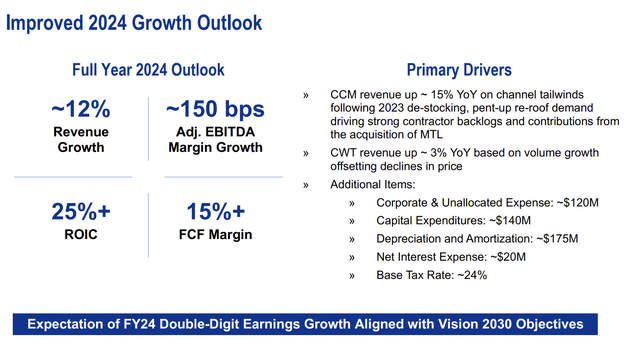

In addition to expecting more than $40 in earnings per share in 2030 (2030 Vision), the company raised its full-year guidance for 2024.

The company expects at least 12% revenue growth, 150 basis points higher adjusted EBITDA margins, and double-digit EPS growth – all aligning with its Vision 2030.

Carlisle Companies

This bodes well for its valuation.

Valuation

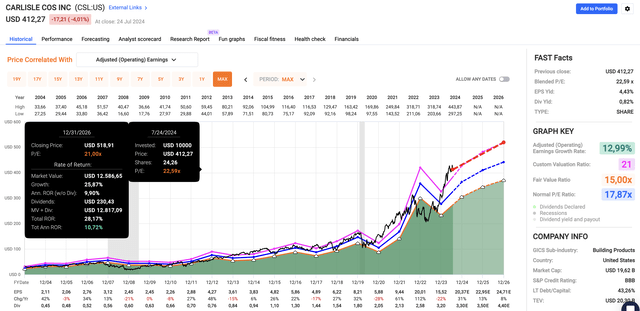

CSL trades at a blended P/E ratio of 22.6x. This is slightly above its 10-year average P/E ratio of 21.0x.

FAST Graphs

However, using the FactSet data in the chart above, a slight premium is justified. This year, analysts expect 31% EPS growth, potentially followed by 13% and 8% growth in 2025 and 2026, respectively.

This implies 10-11% annual returns.

Moreover, using its +$40 EPS target from its 2030 Vision program, the company could have room to $840 per share (21x$40). This implies roughly 100% upside through 2030.

While all of this is subject to change amid economic uncertainty, I believe CSL is in a great spot to generate elevated long-term results, which is why I am adding to my position on corrections.

Takeaway

Carlisle Companies has quickly become a standout in my portfolio, delivering a 95% return since May 2023.

Their latest earnings reaffirm my bullish view, showing impressive financial growth and resilience. With a 10-year return of 460%, far outperforming the S&P 500, the company is capitalizing on the booming commercial building maintenance market.

Moreover, their Vision 2030 strategy targets significant EPS and margin expansion, supported by strategic acquisitions and a bigger focus on innovation.

Despite a modest dividend yield, CSL’s robust free cash flow and shareholder-friendly policies underscore its long-term potential.

Hence, I remain confident in CSL’s trajectory and am eager to capitalize on market corrections to further expand my position.

Pros & Cons

Pros:

- Growth Potential: With its Vision 2030 strategy, CSL targets substantial EPS and margin expansion, aiming for over at least $40 in EPS by 2030.

- Market Position: Carlisle is well-positioned in the commercial building maintenance market, a sector poised for growth due to aging infrastructure and economic reshoring.

- Shareholder-Friendly: The company generates robust free cash flow, supports a low payout ratio, and has an aggressive share buyback program.

- Consistent Dividend Growth: The company has consistently elevated dividend growth, a very healthy balance sheet, and a subdued payout ratio.

Cons:

- Low Dividend Yield: Despite regular hikes, CSL’s dividend yield remains low at 0.8%, which may not appeal to income-focused investors.

- Economic Sensitivity: As a cyclical company, CSL’s performance is tied to economic conditions, which can come with volatility.

- Valuation Premium: Trading at a P/E ratio slightly above its 10-year average could indicate a limited margin of safety if the company fails to achieve its long-term goals.

- Acquisition Risks: While strategic M&A is part of its growth plan, there are always risks in integrating new acquisitions.

Read the full article here