Investment Thesis

ChampionX Corporation (NASDAQ:CHX) has posted strong performance since its merger in 2020 while the latest quarterly earnings results missed the top line and the bottom line. After reviewing its performance by segment in combination with industry-wide trends, we conclude that there is more to the eyes than the headline for the company’s profitability and momentum. Its products that can help improve efficiency and safety for the oil and gas well operators have shown resilience against declining client activities. The steps it has taken to adapt to the changing industry could carve a way of growth forward. We recommend a hold for this stock.

Company Overview

ChampionX Corporation, formerly known as Apergy Corporation with ticker “APY” and based in The Woodlands, Texas, is a global provider of chemistry solutions, artificial lift systems, and highly engineered equipment and technologies for drillers and producers in oil and gas production. It has four reportable segments: Production Chemical Technologies (PCT), Production & Automation Technologies(PAT), Drilling Technologies (DT), and Reservoir Chemical Technologies(RCT), where the Production Chemical Technologies segment and Reservoir Chemical Technologies segment together as the Chemical Technologies business.

Strength & Weakness/Risks

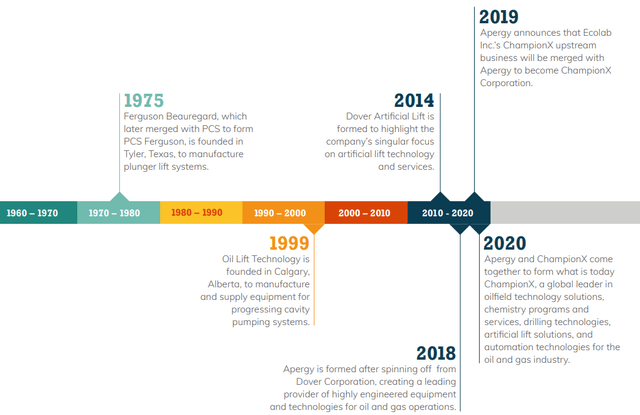

With products ranging from fracking chemicals to artificial lifts for oil and gas well production, ChampionX’s products are mostly aimed at the Explorers & Producers (E&P) and Midstream oil and natural gas value chain. The company has a long history of actively absorbing complementary services to upgrade its core strength to stay competitive. The current ChampionX was formed after Apergy and ChampionX, the upstream unit of Ecolab, merged in 2020. So to evaluate its current business, some of the previous historical data points may not be entirely comparable.

CHX Recent Merger History (Company 2022 ESG Report)

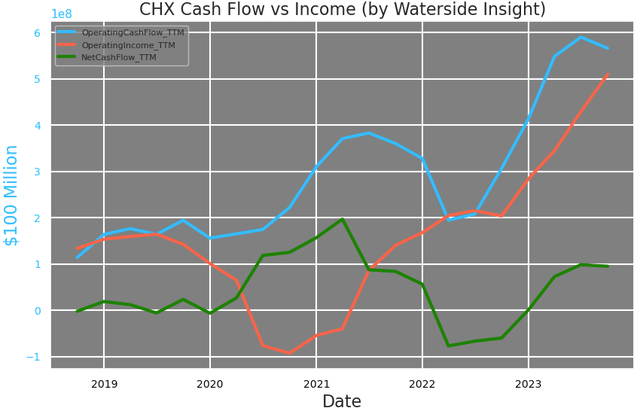

Judging from the basic financial metrics, this merger seems to be a success. Both its operating income and operating cash flow have doubled on a TTM basis compared to pre-merger after overcoming an initial dip. The biggest outflow of its net cash flow in Q3 was for capital expenditure and repurchase of common stock. Net cash flow fluctuated but managed to stay much higher than pre-merger.

CHX: Cash Flow vs Net Income (Calculated and Charted by Waterside Insight with data from company)

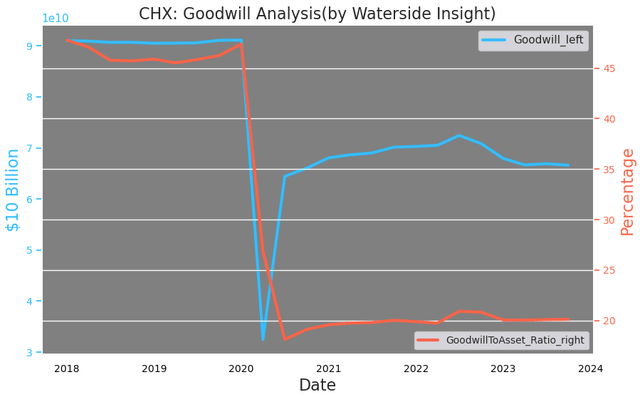

While inflated goodwill usually is a byproduct of M&As, in the case of ChampionX it is actually lower than before the merger both in absolute value and as a percentage of assets. It was halved in the latter.

CHX: Goodwill Analysis (Calculated and Charted by Waterside Insight with data from company)

Reviewing its latest financials, the Q3 earnings reported last week have missed both on the topline by $28.15 million and on the bottom line by $0.08 of EPS. But not all is gloomy if we comb through the results.

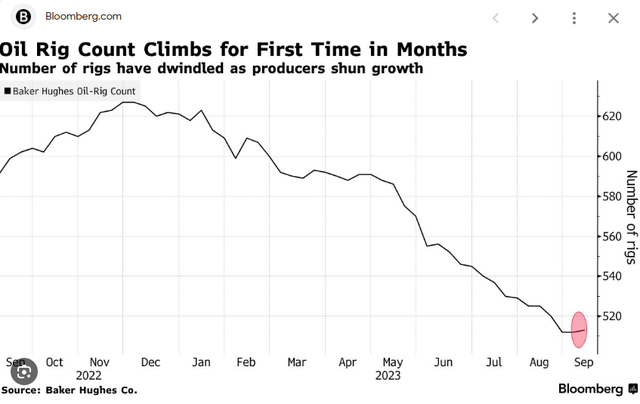

For its topline growth, the company’s total revenue grew about 26% YoY in 2022, but in Q3, its first nine months of growth was about a 1% YoY decline. Its largest segment, Production Chemical Technologies’ revenue increased by 27% YoY in 2022, mostly due to higher volume in North American and International operations, market share expansion, and price increases. Its North American business has over 68% of the total headcount and about 50% of total revenue, and is the largest geographic contributor. PCT segment focuses on oil sand chemical solutions that separate oil, water, and gas in both onshore and offshore production. By Q3 this year, this segment has only grown 5% YoY for the first nine months mainly from market share expansion and price increases to offset inflation. This segment’s revenue was also boosted by $30 million from the sales to Ecolab that were previously included in Corporate & other. Without it, the revenue growth would have been essentially flat. Comparing this with last year, the volume growth has noticeably slowed down mostly due to lower activity in US land from both drilling and completion. According to Bloomberg, the rig count has been sliding this December last year and only seemed to halt this trend recently.

US Oil Rig Count in 2023 (Bloomberg, Baker Hughes)

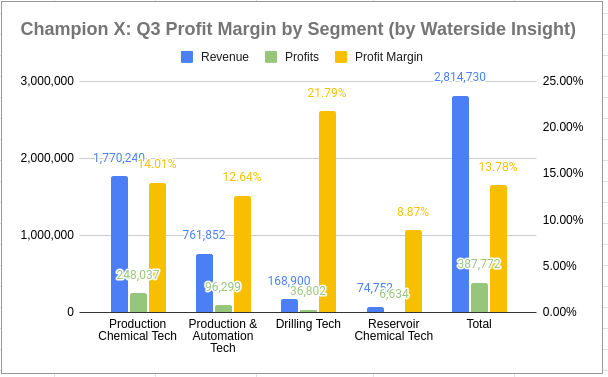

However, strong growth was still simmering on the profit front. The PCT segment, which accounted for 62% of all the revenue and 64% of total profits, has its profit margin growing 73% higher YoY. This segment focuses on managing and controlling corrosion, oil and water separation, flow assurance, sour gas treatment, and a host of water-related issues. The slowdown in volume This is mostly due to “productivity initiatives, and lower expenses in 2023 related to restructuring expenses and charges associated with the CT Russia Business in the prior year’s period”, according to its 10Q.

CHX: 2023 Q3 Profit Margin by Segment (Calculated and Charted by Waterside Insight with data from company)

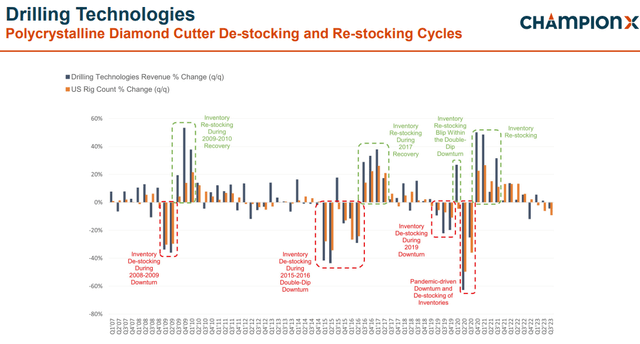

The most profitable segment is one of its smaller segments, Drilling Technologies, which experienced declining YoY revenue. It cited lower U.S. rig count and customers de-stocking inventory as the reasons. The de-stocking and re-stocking cycles of the polycrystalline diamond cutter, which is the main product this segment provides, are closed following the US Rig Count reported by Baker Hughes. This cycle seems to have been exiting the restocking phase and starting a mild de-stocking phase since early this year. However, the reduced production expenses contributed to the profits for the DT segment, which led to a 21.79% profit margin with 18% YoY growth. Productivity efficiency seems to be a recurring theme.

Champion X: Drilling Technologies vs Stocking Cycles (Company Q3 Presentation)

Its smallest segment, Reservoir Chemical Technologies, had a $44 million decline in revenue but $80 million profit growth YoY, although its profit margin was the smallest profit at 8.87%. This segment provides specialty products that support well-stimulation, construction, and remediation needs. Not only it has experienced higher volume from product sales in the US and Latin America, but also has benefited from cost reduction initiatives associated with the exit of certain product lines.

The only segment that reported both strong growth in revenue and profits in Q3 is the Production & Automation Technologies. With its 27% share of the revenue, the PAT segment achieved 7% growth in topline and 36% in profits, not only from higher volume, a favorable price mix but also productivity gain. This segment’s main products are artificial lift and digital automation applications associated with it.

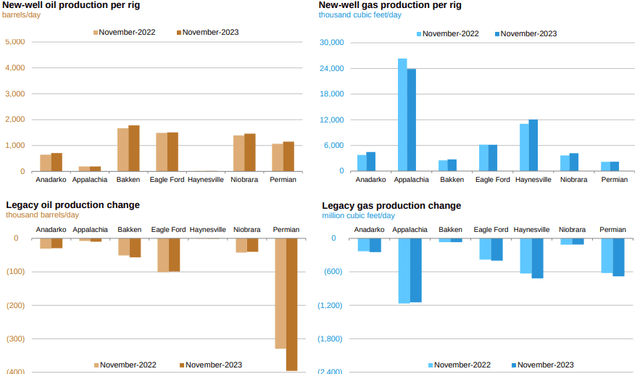

Oil and Gas Well productivity (US Energy Information Administration)

The data above from EIA about rig productivity shows that new wells can be expected to have increasing production while legacy stays flat or decreasing. This is nothing new but what stands out is the comparison between the two. For Permian, the legacy production drop is more significant than the increase of the new wells in oil production. For Appalachia, the new gas well produces much more than the decrease from the legacy ones. The artificial lift equipment is critical for the oil and gas operators to increase pressure within the reservoir and improve production through the life cycle of the well. They are directly linked to the economics of the operators’ profits and losses as both new and legacy wells can use production boost. ChampionX’s software for the operators to adjust the artificial lift system to the expected production rates on-site or remotely is important for the optimization. At the core of its business, the growth of this segment reflects its strength and competitiveness. The company was recently named the 21st member of Permian Strategic Partnership, from a region that makes one of the largest oil production in the States. And maybe the chart above could partially explain why, the legacy oil wells in this region need more boost safely than otherwise.

The comparison and contrast above have shown what drove the company’s growth in the recent quarter isn’t as clean-cut as the headline perhaps suggested. It seems YoY lower volume and client demand have been developing, along with negative impacts from inflation. However, the company is able to raise prices to offset the cost while consistently improving productivity growth and reducing expenses greatly helping to stabilize and improve its profit margin.

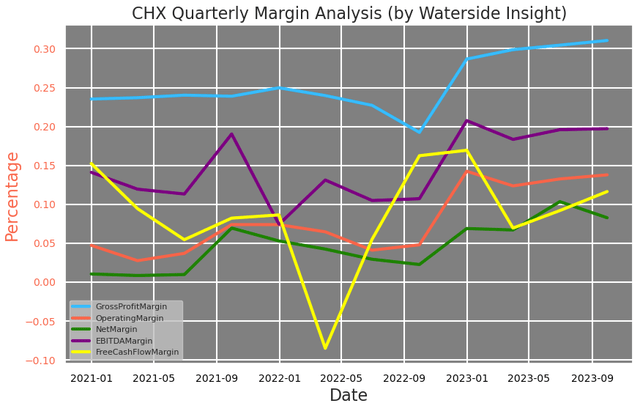

Therefore, we can see from the perspective of its margin, that there are no signs of slowdown despite weak topline growth this year. This is especially telling when we contrast this with the rig count chart presented earlier. The steep decline in client activities hadn’t dented the profitability spectrum.

CHX: Quarterly Margin Analysis (Calculated and Charted by Waterside Insight with data from company)

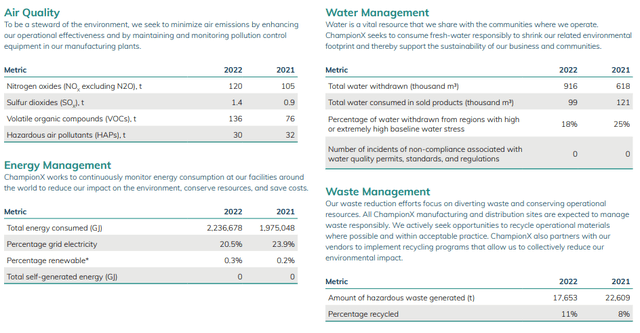

Another aspect of ChampionX’s future growth development is its increasing engagement in providing carbon footprint reduction tools. Unlike other large players in this field that directly participate in the drilling and production process, the company does not have the capability to provide some of the “reversal” such as carbon capture and storage to reduce its clients’ impact. However, its technical know-how can provide more delicate support in this ESG process. It has rolled out an all-important emission monitoring device called “SOOFIE continuous emission monitoring system”, which provides onsite methane emission detection. The company quoted a recent case where SOFFIE helped one of its customers detect and avoid a catastrophic leak at a production facility in real time, resulting in environmental and financial savings. It already has a real-time digital automation system with a modular architecture that connects all its global technical experts in chemical solutions and production that monitor and optimize the treatments, well, artificial lift system, and production downtime. Such a system is able to extract more value from existing infrastructure while improving safety and reducing emissions. The newest emission monitor system is a natural extension of this integrated system, which means when the company sells, it sells the whole package. It is a must-have for its customers who are facing increasing pressure to make use of existing infrastructure while limiting greenhouse emissions. This goes back to how the company was able to raise prices to offset costs and subdue volume growth to boost profits growth. The digital solution and platform enable it to function in an asset-light operating model compared with traditional oilfield services firms, leading to more effective cost management through adverse market environments. Its emphasis on safeguarding safety in production has become crucial for operators’ economics.

ChampionX plans to “Accelerate Digital and Emissions Growth” as one of its four priorities in growth strategy. We all understand that drilling activities are going to have a declining trend in the long term. But at its core, ChampionX is a technological company. In a bold question, we ask if it is possible for it to transition into a more cleantech application in a not-too-distant peak-oil future. We think the potential and drive are there. The company has been using its drilling tech to dig water wells in remote areas by partnering with Ultera and WHOlives. It also partners with OPRC and US Synthetic to develop reliable solutions for capturing and converting hydrokinetic energy from ocean waves and river currents into renewable electricity. Its 2022 ESG report highlights its technological application in air quality control, energy, water, and waste management, which can all improve efficiency and be environmentally positive. For now, we don’t want to oversell this point but just leave it as it is for the management and investors to reckon with.

CHX Eco-Friendly Management and Control (2022 ESG Report)

Back to its current main business and looking ahead to Q4, the company expects only a $30 million increase or a 4% growth in revenue, mostly coming from international business expansion. However, with the war in the Middle East escalating, oil prices seem to have firm support around $90 for WTI. Although it may not completely change the year-end holiday seasonal decline for ChampionX’s North American business, the upward momentum of the oil prices could have a positive impact on its clients’ activities should the war last longer than anticipated.

Financial Overview & Valuation

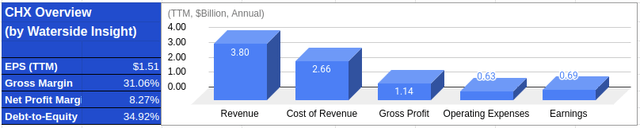

CHX Financial Overview (Calculated and Charted by Waterside Insight with data from company)

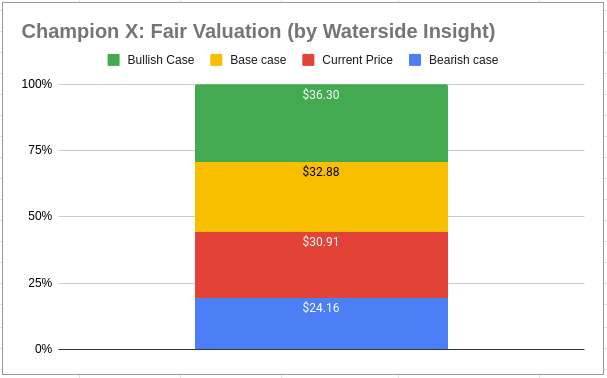

Based on our analysis above, we use our proprietary models to assess ChampionX’s fair value by projecting its growth ten years ahead. We assume a cost of equity of 10.77% with a WACC of 12.93%. In our base case, the company had a limited decline in next year’s growth while although maintaining some stability in its earnings, its cash flow volatility could increase in 3 to 5 years time, and it eventually found some footing in balancing its drilling and ESG business; it was priced at $32.88. In the bullish case, it grew strong safety solutions for oil and gas producers while developing more growth drives outside of drilling by applying its technological advantage in solving related problems; it was priced at $36.30. In the bearish case, the continued curtailing of drilling activities eventually took a hit on the company’s growth, but it maintained a strong lead in efficiency and safety solutions without a business line in cleantech applications; it was priced at $24.16. The current market price is tilted to the bearish side.

We don’t see a major downside for the company in the near term as its products are proven to be critical in both boosting well production and providing environmental safeguards. When push comes to shove, the possibility of more mergers to bring the company to transition into higher-margin cleantech is still there. The Ecolab merger in some sense is already a step in that direction.

CHX Fair Valuation (Calculated and Charted by Waterside Insight with data from company)

Conclusion

Although ChampionX is not a big company compared to other oil and gas titans, its technological development and future growth could reflect a broader transition for this industry as a whole. The company has a well-crafted asset-light development model and strong net demand from the producers for its products. It should be able to weather the medium-term trend of declining drilling activities. Moreover, more technological applications of related oil and gas field problems could use its know-how, which could spell potential business lines in clean tech as a transition. We find the company both dynamic and adaptable to industry changes that major downside could be avoided. For now, it is a hold for us.

Read the full article here