GEOS Can Dodge The Slowdown

I discussed Geospace Technologies Corporation (NASDAQ:GEOS) in the past, and you can read the latest article here, published on May 22. In Q3, its oil & gas business continued to underperform due to gaps in marine OBX rental fleet demand, which lowered its utilization. Factors like inclement weather and unawarded client surveys were responsible for the deteriorated performance in the energy operations. A weak cash flow in 9M 2024 remained a matter of concern for the investors.

However, the company’s initiative to increase the share of revenues from adjacent and emerging markets reduced the typical energy market volatility. Its smart valve technology and the Aquana product line produced sufficiently strong results. Plus, its recent slew of contracts in ocean bottom wireless seismic data can signal a recovery in outlook. The stock is reasonably valued compared to its peers. Given the short-term challenges and the opportunities forming in the medium term, I view it as a “hold.”

Why Do I Keep My Rating Unchanged?

In my last iteration on GEOS published on May 22, I discussed how the company’s oil and gas business underperformed due to slow project execution and lower fleet utilization. It also saw deferral of large rental projects and negative cash flows. Despite that, growth potential in the offshore industry and focus on adjacent and emerging markets would help stabilize revenues. I wrote:

GEOS’ growth momentum has been thwarted in the near term due to the lag between crude oil price recovery and seismic data acquisition activities. Over the medium term, I expect increased activity in the offshore energy market to lead to higher utilization for its rental fleet of OBX ocean bottom nodes. The company’s diversification strategy has reduced earnings volatility. Effective use of new product lines, including a detection system, has significantly increased its share of revenues from non-energy activities.

Since then, the company has become cautious due to the lack of demand for seismic products. Gaps in OBX rental contracts, unawarded client surveys, and weather delays affected utilization. The energy industry environment has not been conducive. On the other hand, water meter cables and connectors and defense department projects breathed life into its emerging market business. Cash flows turned negative again in 9M 2024. Considering the company’s robust balance sheet, I maintain my rating at a “hold.”

Business Strategies

GEOS’s Q3 2024 Investor Presentation

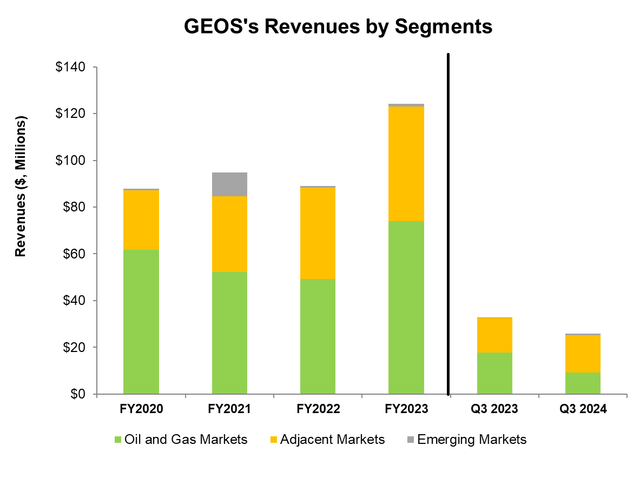

Geospace aims to diversify beyond the seismic industry. It plans to bring new products to market, leaning on growth in its Adjacent and Emerging Markets. The company has been cautious about the seismic market, which saw significant volatility in recent months. It has adjusted its supply or manufacturing capabilities to meet demand. It will not keep an inventory but will serve the market when needed to keep costs down.

The company’s Adjacent Markets segment grew impressively in Q3 following an increased acceptance of the Aquana product line. It expects to see growth through the Internet of Things (or IoT) and cloud-based technologies. Investors may note that Aquana is a smart valve technology that allows municipalities to control the valve. It increases the smartness in monitoring and is a new technological use in this space. It gained significant traction over the last couple of years. It sees uses in municipalities and multifamily usage.

Challenges And Opportunities

In Q3, gaps in OBX rental contracts affected GEOS’s revenues from the Oil and Gas Markets segment. The delays are related to a previously announced contract (valued at ~$3.6 million) and accounted for a portion of the differential from Q3 2023. Unawarded client surveys, unexpected weather delays, and customers’ operational difficulties contributed to the extended gaps. The energy industry has been relatively weak in 2024. The US rig count has dropped by 5% year-to-date. Crude oil prices remained steady, but natural gas prices have decreased in 2024. The management expects the situation to normalize in Q4.

The key among the new growth areas is the water meter cables and connectors, which are generating additional revenues. I expect substantial revenue contributions from the Aquana smart water valve and IOT technology products. The other revenue enabler is a higher backlog from the DARPA contract in the Emerging Markets segment. I discussed in my previous article that the GAO (Government Accountability Office) can spend additional money on some of the projects, although it is unlikely to occur before 2025. So, the government budgetary cycles will largely determine the performance of the emerging market segment. As of June 30, 2024, this business segment had a backlog of ~$750,000, owing mainly to a U.S. Border Patrol contract. I see further opportunities from government agency security projects and advanced energy and energy transition monitoring projects.

Recently, GEOS announced the sale of OBX-750E seabed ocean bottom wireless seismic data acquisition nodes in a $10.5 million contract. Also, in August, it announced a 240-day rental contract for OBX-750E, shallow water seabed wireless seismic data acquisition nodes. The value of the agreement is estimated to be $11.9 million, to be delivered in Q4 2024.

My Estimates

Seeking Alpha

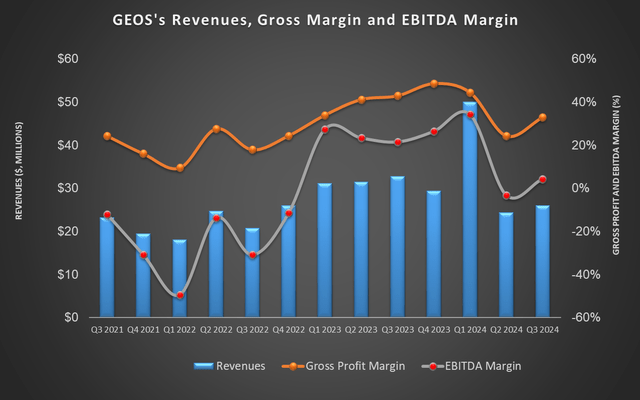

Over the past 16 quarters, GEOS’s quarter-over-quarter adjusted EBITDA declined by 4.5% on average. However, in recent times, it has managed to remain positive on more occasions than not. While its Q4 EBITDA would change little, I expect adjusted EBITDA to increase by 3%-5% in the next four quarters.

Q3 Performance Analysis

GEOS’s Filings

As announced in the Q3 earnings released on August 8, GEO’s year-over-year revenues from the Oil and Gas Markets segment decreased by 48%. Severe gaps in OBX rental contracts caused revenues caused lower utilization for its wireless seismic rental fleet and led to a revenue decline in Q3 2024. The segment’s operating income turned to a loss in Q3 from a profit a year ago.

Revenues in the Adjacent Markets segment increased handsomely (7% up) year-over-year in Q3. Operating income remained steady during this period. Higher revenues from water meter cables and connectors and increased contributions from the Aquana smart water valve led to the growth. GEOS’s revenues from the Emerging Markets segment also increased significantly, although its share of total revenues is low (~2%).

Cash Flows And Liquidity

In 9M 2024, GEOS’s cash flow from operations turned negative over the previous year despite a marginal revenue rise. As a result, free cash flow turned negative in 9M 2024. If we include proceeds from the sale of rental equipment (net of gains), free cash flow will still deteriorate in 2024 from a year ago.

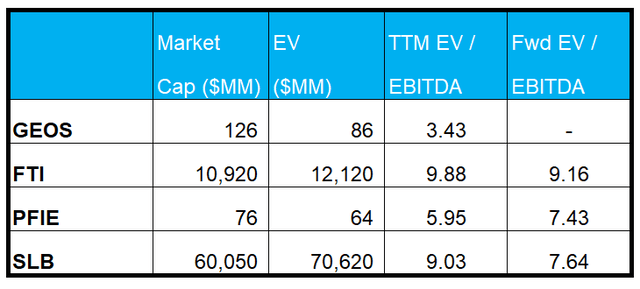

With zero debt, GEOS has a distinct advantage over some of its peers (FTI and SLB). As of June 30, its liquidity (cash and short-term investment) was $57 million. In Q4, it anticipates capital expenditures of $5 million, including the capex for additions to its rental equipment.

In 9M 2024, GEOS’s cash flow from operations turned negative over the previous year despite a marginal rise in revenues. As a result, free cash flow turned negative in 9M 2024. With zero debt, GEOS has a distinct advantage over some of its peers (FTI and SLB). As of June 30, its liquidity (cash and short-term investment) was $57 million. In Q4, it anticipates capital expenditures of $5 million, including the capex for additions to its rental equipment.

Relative Valuation Imply And Target Price

Author Created And Seeking Alpha

GEOS’s current EV/EBITDA multiple (3.4x) is much lower than its five-year average (16.6x). So, it appears to be undervalued versus its past. If the stock trades at its five-year average, it would provide a 251% upside potential. However, I do not see the stock trading anywhere close to its past average. The stock price decreased by 2.5% since my last publication on May 22, when I recommended a “Hold.”

As I discussed earlier in the article, I expect 3%-5% adjusted EBITDA growth in the next four quarters. Feeding these values in the EV calculation and assuming the current EV/EBITDA multiple holds, the stock can trade between $9.9 and $10.1, implying a marginal 1% upside.

Risk Factors

Over the past year, crude oil prices have been relatively stable, while natural gas prices have been down. When commodity prices correct or decrease, upstream operators’ capital spending budgets typically contract in response. In FY2023, customers outside the United States accounted for approximately 50% of GEOS’s revenues. Typically, trade wars and trade restrictions impact the company’s financials. Given the changing geopolitical environment, such instances can affect the company’s revenues and margins in the future.

What’s The Take On GEOS?

Seeking Alpha

The energy market has been challenging GEOS’s performance as utilization has fallen in 2024. It saw gaps in OBX rental contracts following unawarded client surveys and adverse weather. The situation can reverse with the recent acquisition of a few projects on ocean bottom wireless seismic data. The company’s strategy is to focus on non-energy markets, including water meter cables and connectors, generating additional revenues. It plans to bring technological advances in these fields.

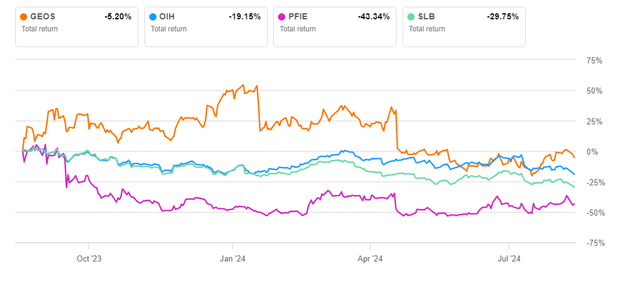

The defense sector is another area that continues to receive new contracts. So, the stock outperformed the VanEck Oil Services ETF (OIH) in the past year. Cash flows deteriorated in 9M 2024. The stock’s relative valuation appears fair to me. I expect the stock price to produce marginally positive returns, which validates my “hold” rating.

Read the full article here