Sometimes, acquisition deals come along that make all the sense in the world, and mark a big pay-off for investors who bet on a small but winning idea. Sometimes, those deals don’t end up going through, and they’re left picking up the pieces of a company that still has to go it alone.

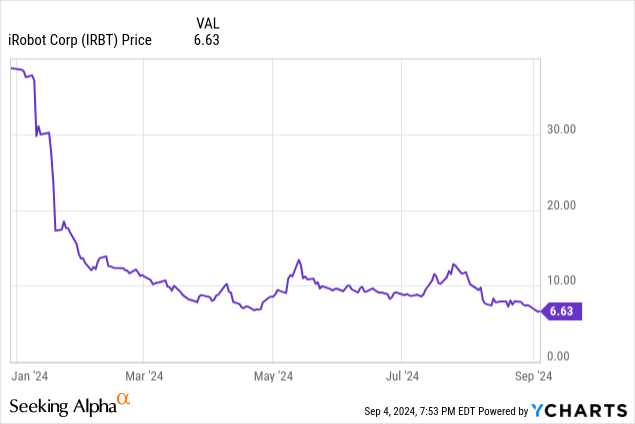

Today, we’ll be looking at iRobot Corporation (NASDAQ:IRBT), a company whose price absolutely cratered since the expected acquisition by Amazon (AMZN) fell apart back in January in the face of European opposition. There’s no point in re-litigating the question of whether the acquisition should’ve been stopped, iRobot still stands alone.

What I want to do is analyze the company, warts and all, as it stands at its much cheaper price today. The question is whether, floating near a 52-week low, this is a good rebound candidate, and if the company looks like it can survive without being part of the online retail giant.

Understanding iRobot

iRobot is a consumer robot company with a 30-year history and substantial business both domestically and internationally.

In its early history, the company hit a home-run with its Roomba product, a robot vacuum cleaner that has become an icon in the future of robots in the home. The company has seen revenue and demand decline in recent years.

iRobot is working presently to reorganize after the Amazon deal fell through, trying to improve its iRobot OS and cut costs, trying to improve their gross margins, which have been dwindling in recent years.

Balance Sheet

|

Cash and Equivalents |

$108 million |

|

Inventory |

$101 million |

|

Total Current Assets |

$340 million |

|

Total Assets |

$586 million |

|

Total Current Liabilities |

$222 million |

|

Total Liabilities |

$437 million |

|

Total Shareholder Equity |

$149 million |

(Source: Most recent 10-Q from SEC)

iRobot has a fair amount of cash on hand in the wake of the Amazon failure. The company is not, on the surface, terribly financed, though there is concern about profitability and how long that cash is going to last, which will be discussed further.

The really interesting thing, I think, is that at current prices the company is trading at a price/book value of 1.34, which is well below the sector median of 2.17. That’s what attracted me initially to the company, as having dropped to new near-term lows, it might be a rebound candidate. That’s only one metric, though, and we’ll be considering more than just the balance sheet.

The Risks

iRobot admits that it expects an operating loss for the foreseeable future. While the company is desperately trying to cut expenses and fix the declining margins, there is no guarantee that the company will ever return to profitability in the future. That’s a very big deal, as to survive as a going concern, iRobot absolutely has to turn a profit someday.

Getting from here to a survivable future is going to require spending cash, and the company warns in its 10-K that the cash they have may only last them about 12 months. The company may need to raise more working capital, and for an unprofitable company that likely means dilution of shares.

Restructuring is ideally the answer for iRobot, but there is no guarantee that the restructuring is going to work, or at least end with a worthwhile resultant company.

Even if they can navigate the difficulties of the near future, iRobot faces a lot of intense competition from other robot providers, and that’s going to be a drag on their margins in the future.

Statement of Operations

|

2021 |

2022 |

2023 |

2024 (1H) |

|

|

Total Revenue |

$1.56 billion |

$1.18 billion |

$890 million |

$316 million |

|

Gross Profit |

$550 million |

$350 million |

$196 million |

$63.5 million |

|

Gross Margin |

35.1% |

29.6% |

22.0% |

20.1% |

|

Operating Income |

($1 million) |

($240 million) |

($269 million) |

($49 million) |

|

Operating Margin |

(0.1%) |

(20.3%) |

(29.7%) |

(15.5%) |

|

Net Income |

$30 million |

($286 million) |

($305 million) |

($62 million) |

|

Diluted EPS |

$1.08 |

($10.52) |

($11.01) |

($2.16) |

(Source: Most recent 10-K and 10-Q from SEC)

iRobot of 2021 was very much a different company than it is today. In 2021, the company was profitable, and if it was trading at these prices it would look very appealing to me.

Sadly, the revenue has dropped about in half over the last couple of years, gross margins have shrunk substantially, and the company as it stands today is absolutely bleeding cash.

If there is a bright spot, it’s that the estimates suggest that the rate of loss is going to go down in the future. This year, it is expected the company will report $792.5 million in revenue and lose $3.67 per share. Next year the revenue will trickle up to $818 million and the loss per share will be down to $1.15.

The most recent quarter saw iRobot missed both on revenue and lost more money than was anticipated. This is potentially a bad sign, as the company doesn’t have so many resources that it can afford to make a lot of mistakes trying to restructure to a sustainable company.

Conclusion

Long ago, I bought an iRobot-brand Looj to try to automate cleaning my gutters. I put the robot into the gutter, and within about 30 seconds, it hurled some mud into my face, then promptly flipped over and fell to the ground. I sort of feel like that’s a metaphor for what investors have had to happen to them when they invested in iRobot before the planned Amazon acquisition.

Don’t get me wrong, the company has a chance of righting the ship. But even at the reduced price it currently trades at, to me, the risk is much too high to justify a new investment. I would keep an eye on the falling knife, but I would very much stay away from it for now. I’m rating it a hold, at best.

I would keep an eye on iRobot for signs that the restructuring is working, and more importantly for signs that the gross margins and the shrinking revenue trends are starting to reverse. Without that, the company is, in my opinion, only going to keep declining without the obvious way out of an acquisition. This is a company whose investors would’ve been better off if the Amazon deal had survived.

Read the full article here