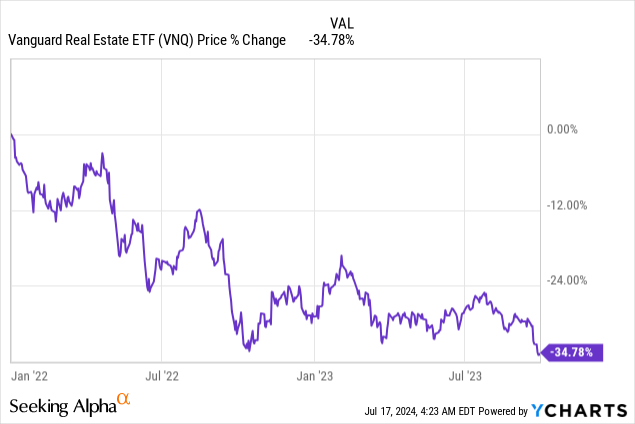

Real estate investment trusts (REITs) (VNQ) got absolutely pummeled over the past two years.

Their share prices crashed by ~35% even as most of them grew their cash flows and dividends by ~10% during this same period:

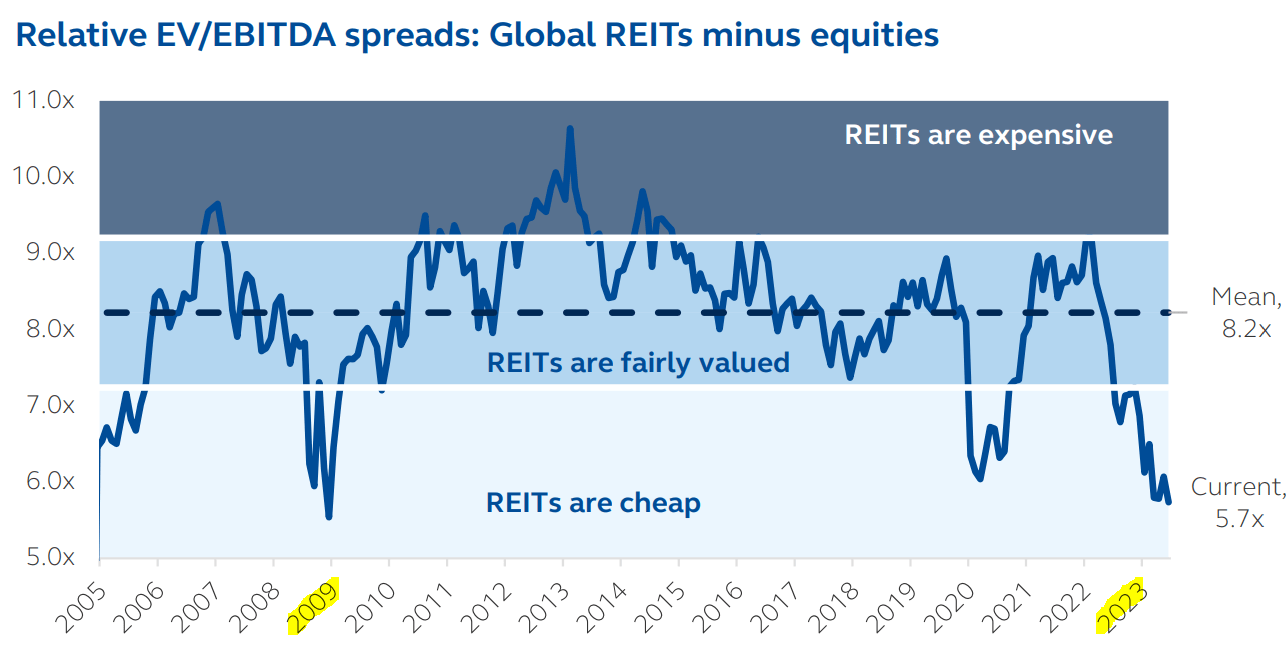

Valuations got so low that we started to compare them to those of the great financial crisis. Most REITs were not this cheap even during the pandemic:

Principal Asset Management

And the #1 reason for this is, of course, the surge in interest rates.

It caused investors to sell REITs, regardless of their strong fundamentals, to reallocate into bonds, treasuries, and money market funds.

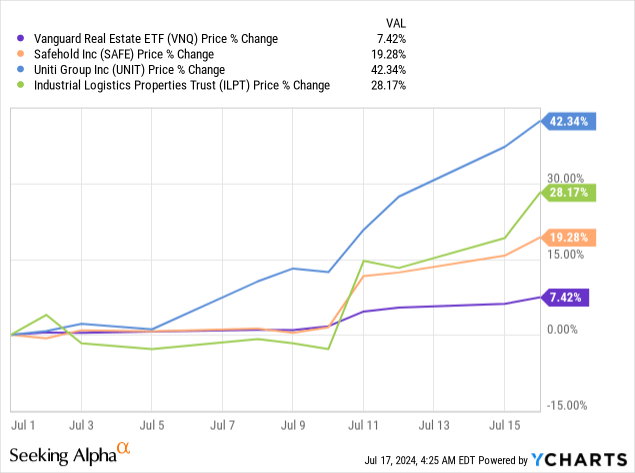

But REITs just pulled an UNO reverse card. It is very likely that interest rates will now gradually return to lower levels, and REITs have already started their recovery. In the last week alone, REITs surged by 7% on average, with some individual names such as Uniti Group (UNIT) rising by as much as 40%:

And I expect this rally to continue because of four key reasons:

1) Valuations remain exceptionally low

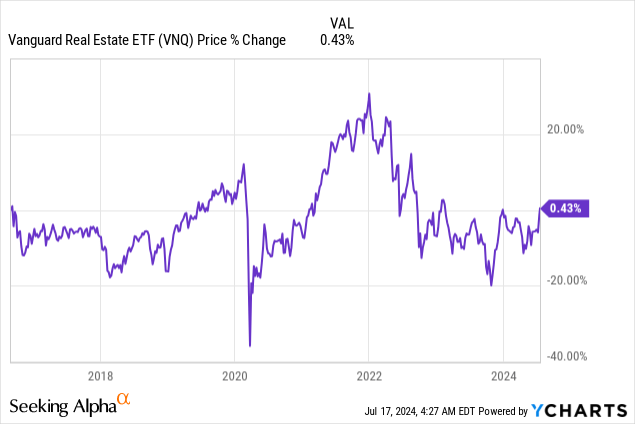

The first important point is that despite this rally, most REITs remain cheap relative to most other asset classes.

Yes, they are up 10%. However, remember that they had declined by 30% in the past two years, and even before that, their performance had been nothing exceptional in previous years as we had the pandemic and a rate hiking cycle leading up to it. So the market sentiment of REITs has been low for a long time now. REIT share prices have not really changed since 2016!

Moreover, REITs greatly benefited from the high inflation of recent years, as it allowed them to rapidly grow their rents. This explains why most REITs are today earning higher cash flows, even despite the surge in interest rates.

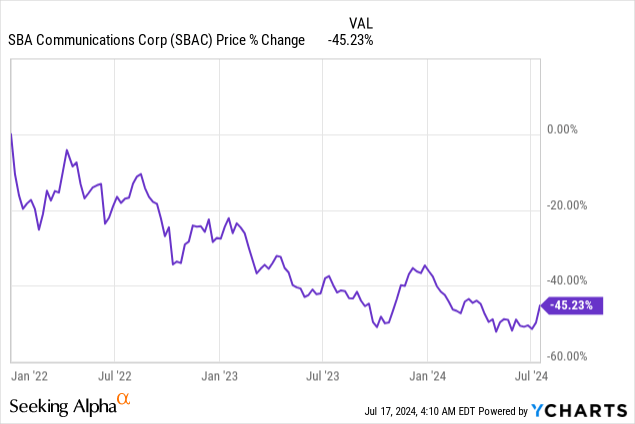

Take the example of SBA Communications (SBAC): Its share price is today still 45% lower than it was in late 2021, and that’s despite earning 23% higher cash flow today than it did back then:

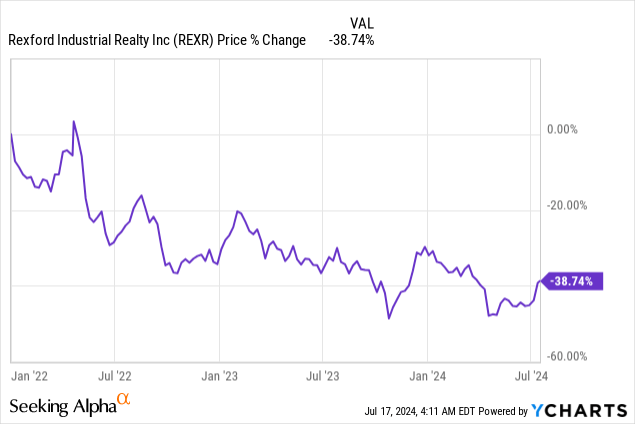

Or Rexford Realty Trust (REXR): Its share price has crashed 39% despite today earning ~40% higher cash flow than in late 2021. This essentially means that its valuation multiple is today just 1/3 of what it was in late 2021, even after the recent rally.

And yes, I know that some of you will think that these REITs were overpriced in late 2021, and that is true to an extent. Valuations were a bit stretched back then. But today, it is the opposite. Valuations are still at a near-decade low, even following the recent rally. We think that fair value is somewhere in the middle ground.

2) Rate cuts have not even started yet

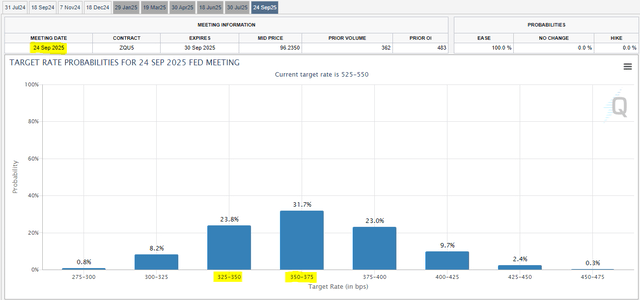

REITs have now started to rally on the prospect of a single 25 basis point rate cut in September.

But you need to look a little further. The debt market is now pricing ~2% lower interest rates by September 2025:

FedWatch

This means that it likely won’t end at a single rate cut now in September. Rather, we are likely to get many more rate cuts in the coming months, resulting in a steady flow of good news for the REIT sector.

Here, it is interesting to compare European REITs to US REITs because interest rates have already been cut once in the Eurozone, and it has pushed their share prices to a lot higher levels.

To give you a few examples that we own:

- Vonovia (OTCPK:VONOY) is up 75% since March.

- Helios Tower (OTCPK:HTWSF) is up 73% since March.

- Cibus Nordics (CIBUS) is up 55% since March.

US REITs are up, but they have not risen nearly as much as these European REITs and as interest rates are cut, I expect them to follow the same path. It will gradually change the narrative from “higher for longer” back to “TINA = there is no alternative.”

3) Rent growth is about to accelerate.

Right as interest rates are cut, rent growth is also strongly expected to accelerate. That’s because the high inflation of recent years and the surge in interest rates have put most new construction projects on halt.

Currently, new construction starts are at a decade-low in many property sectors. This means that the demand/supply dynamics will soon shift strongly in the favor of landlords.

BSR REIT’s (HOM.U:CA; OTCPK:BSRTF) recently said this (emphasis added):

“The pipeline of new supply is very thin beyond this year. And with migration into our markets continuing, we expect new supply to be absorbed by early 2025. We therefore believe that 2025, 2026, 2027 and beyond will be significantly stronger years for our rental markets. I would now like to review our guidance for 2024, which we updated yesterday.”

That’s for apartments. Here’s what the CEO of Prologis (PLD) said about industrial properties (emphasis added):

“I think what’s important to understand in the cycle is the recovery potential in 2025 related to each of the constituent pieces. Hamid walked you through the demand picture. But what’s important to recognize is the supply picture. That was a big factor over the last year, 18 months. And the meaningful falloff in supply is marked. It’s off 80% from peak. It’s off about 1/3 from pre-COVID levels.”

Finally, here’s what Blackstone (BX) said after acquiring $17 billion worth of REITs on a recent conference call (emphasis added):

“We’ve already done a number of big deals this year, and we’ll be net buyers for some time. So our attitude towards real estate is quite positive. And can you imagine being down 60%, 70% in construction in good areas? I mean this is how you really make money in real estate.”

So it appears very likely that rent growth will accelerate in 2025.

This is happening right as interest rates should be cut.

And I think that this is a compelling combination that should materially improve the sentiment of the REIT sector.

Presently, investors perceive REITs as slow-growth vehicles facing oversupply in a higher-yield environment.

Soon, they will perceive them as high-yielding vehicles with accelerating growth due to real estate shortage in a lower-yielding world.

4) Institutional capital allocations are yet to change

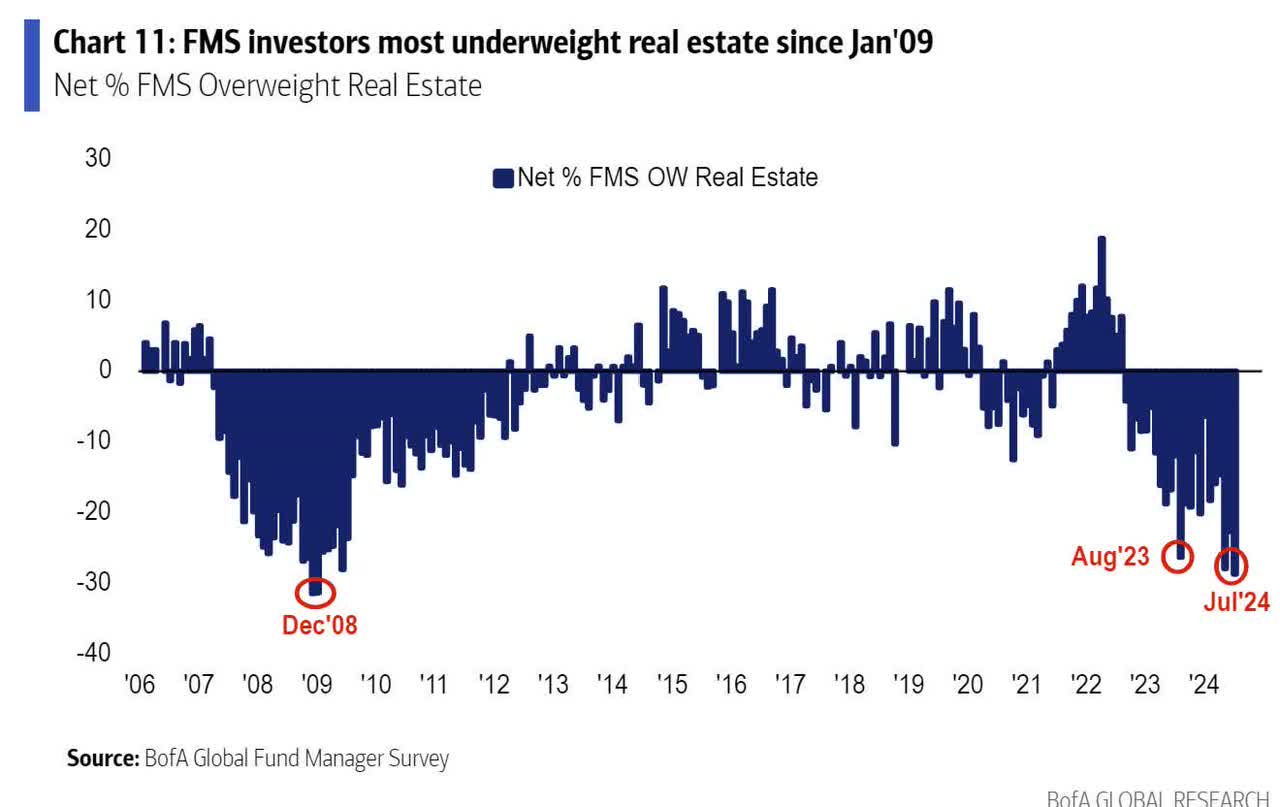

Despite the recent surge, investor’s allocations to REITs remain at the lowest point since the great financial crisis.

That’s what peak bearishness looks like:

BofA Global Fund Manager Survey

This means that there is a ton of capital that’s likely to soon shift back to the REIT sector as the narrative changes.

This shift has not even started yet, and REITs are rising already.

So just imagine how REITs will perform when interest rates are cut, rent growth accelerates, and institutional capital returns to the sector.

Opportunistic private equity players like Blackstone (BX) are already buying REITs, and I am not talking about them. I am here referring to all the pension funds, endowment funds, etc. that have been happily hiding in treasuries, but will soon need to reconsider their allocation to keep generating income in a lower-interest rate environment.

I think that the rally could be just beginning.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here