Powersports retailer, Polaris (NYSE:PII), is trading lower following Q3 results. In my last update on the stock shortly after the Q2 print, I viewed shares as priced to perfection in the $130/share price range, my estimated target price. Since hitting that level, shares have been on a downward track.

Presently, shares trade near new 52-week lows at a forward trading multiple of about 9x. While this may attract attention, I believe the stock will remain under pressure in the months ahead.

Q3 results came in worse than expected and the company outlined earnings guidance that was significantly downgraded from their prior forecast. The downgrade came amid fresh challenges on the manufacturing front. It also came in the face of a waning demand environment, one that I don’t see improving any time soon.

For investors seeking new or additional positioning in PII, I believe shares are best left on hold, given the current operating weakness.

Summary Of PII Q3 Results

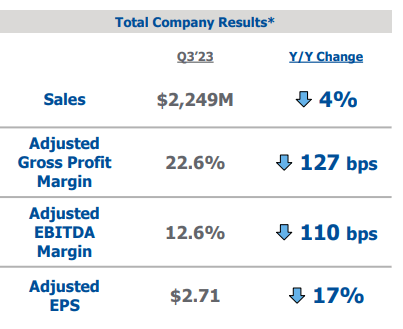

Q3 sales growth was weak across segments, with total overall sales down 4% YOY and +$20M below expectations. One factor driving the weakness was lower shipment volumes relative to the same period last year, one that included elevated shipping volume in compensation for low dealer inventory levels. North American retail, though up 5% was still lower than expected. PII also noted a higher promotional environment during the period.

PII Q3 Earnings Presentation – Summary Of Operating Results

The promotional environment, as well as higher manufacturing costs, took a bite out of PII’s margins in Q3. Adjusted gross profit margins and EBITDA margins were each down 127 basis points (“bps”) and 110bps, respectively. To blame for the increased promotional activity was the higher rate environment, which effectively added an additional premium to their product offerings, and higher dealer inventory levels.

In addition, total overall sales were geared to a more unfavorable product mix, due in part to slower production of their premium Off Road products, which includes PII’s new XPEDITION and RANGER XD.

The setbacks in product manufacturing and weaker end market demand forced the management team to narrow their full-year sales guidance to the lower end of their range and to also lower their margin and adjusted EPS guidance.

Sales growth is now seen at a midpoint of 4%, down from the previous target of 4.5%. Even more notable is the sizeable revision in adjusted EPS, now seen down 8% at the low end of the range. This compares to down just 2% in PII’s previous forecast.

Market Reaction To PII Results

Investors sent shares down about 3% in extended trading immediately following the release. Shares retained those losses in early morning trading on Wednesday.

The losses bring total YTD performance to a negative 11%, a far cry from the S&P’s (SPY) 11% gain over the same period.

Seeking Alpha – YTD Share Price Performance Of PII

The losses are a rapid comedown from July, when PII hit new 52-week highs.

Key Takeaways Of PII’s Q3 Results

Weakness In Off Road Recreation: On the surface, PII’s Off Road segment looked strong. The unit gained share during the quarter, and North American retail was up 5%, comparably better than the low single-digit percentage increase reported by the overall industry.

The strength, however, was led by the more commercial aspects of the business, such as utility. On the recreation side, revenues were down 20%. PII also incurred manufacturing hurdles, which hindered their ability to roll out their more premium product lines, those with a higher margin profile. The combination of higher production costs and an unfavorable mix ultimately contributed to the 265bps decline in margins during the period.

The snow season was noted by CFO, Bob Mack, to be off to a good start. And the company presentation noted that the demand metrics remain healthy for new and premium products. But without the actual sales figures, it’s hard to get bullish on the call-outs.

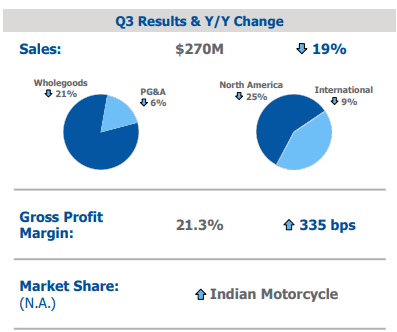

Margin Strength In On Road Segment: In Q3, PII continued to report strength in their motorcycle offerings. Retail sales were down in the low-teens percentage range due to increased promotions from heightened competition levels. The unit, nevertheless, still gained market share and performed stronger than the overall industry.

PII Q3 Earnings Presentation – Summary Of On Road Segment Performance

The segment also faced a difficult comparable environment, with YOY revenues down 19% due to lower shipping volumes relative to the same period last year, where PII realized a large catch-up on motorcycle shipments following constraints earlier in 2022.

Despite the more challenging operating environment, margins in the On Road segment continue to impress. In Q3, margins were up 335bps due in part to a favorable product mix. The expansion in margins also represented the fifth straight quarter over 250bps.

PG&A Offerings Continuing To Offset Weakness Elsewhere: While consumers appear to be pulling back on the larger discretionary vehicle purchases, there is no apparent waning in appetite for PII’s offerings of parts, garments, and accessories.

Q3 marked a record quarter for PG&A revenues, with sales up 12% YOY. The continuing strength in PG&A indicates that product utilization remains high. This may bode well in future periods as newer models are rolled out by the company.

Is PII Stock A Buy, Sell, Or Hold?

I have flip-flopped on PII in prior coverage on the stock. In early coverage, I viewed shares neutrally due to their higher trading multiple at the time of coverage. In addition, shares were also trading near their previously estimated fair price of $130/share, leaving little room for upside.

In more bullish coverage, I’ve cited the pullback and the upside potential in relation to my target price, which did materialize in July. But since then, shares have pulled back to new 52-week lows. In a prior operating environment, I would have seen the pullback as an opportunity for new addition. Not anymore.

PII is continuing to gain market share across segments, particularly in their offerings of motorcycles. But their Marine division continues to be a perpetual drag on the business. And elsewhere, PII appears to have missed a sales opportunity due to manufacturing challenges, which impeded production of their premium product offerings, a product class that remains in demand from those on the higher end of the income spectrum, while also carrying a higher margin profile.

Looking ahead, I don’t see the operating environment turning in PII’s favor. Interest rates are likely to stay higher for longer. This will continue to create an embedded premium on their discretionary products and will likely result in continued weakness on the recreational side. Promotional activity in turn may hang around for longer than expected. Margins could take time to recover, and I view it as more likely for PII to hit the lower end of their EPS target than the upper. This warrants a hold on the stock, in my view.

Read the full article here