PulteGroup, Inc. (NYSE:PHM) operates as a homebuilder in the United States, developing a range of single-family homes. The company works under multiple brand names, including Centex, Pulte Homes, Del Webb, and others.

The homebuilding industry is seeing turbulent industry trends amid high inflation, higher but lowering interest rates, and a weak labor market. However, I believe that the industry’s long-term outlook still stands good as PulteGroup continues to grow in line with peers with top-of-the-line margins.

With an impressive long-term history of incredibly profitable growth, PulteGroup’s stock has compounded at a 21.7% CAGR in the past decade. This is on top of the fact that the company pays out a current 0.6% dividend yield, as cash flows are largely spent on fueling EPS growth. The company more notably does a significant amount of share repurchases, decreasing outstanding shares by nearly 43% from 2014.

Ten Year Stock Chart (Seeking Alpha)

A History of Impressive, But Industry-Aided Growth

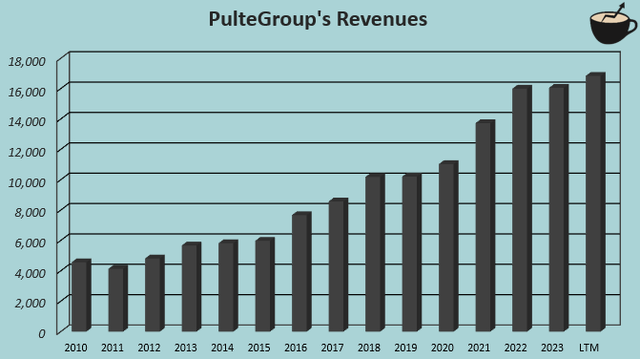

After the great financial crisis, PulteGroup has grown its revenues incredibly well. It had a CAGR of 11.8% from 2014 to Q2/2024, only including a very moderate boost from small cash acquisitions. United States median housing prices have surged 46.7% in the same period at a 4.1% CAGR, so the foundation for the home building industry has been great with incredibly good demand.

Author’s Calculation Using TIKR Data

The industry-trend aided growth is mostly in line with PulteGroup’s peers. The company’s 11.8% CAGR from 2014 outpaces Toll Brothers’ (TOL) 10.7% CAGR in a near-similar fiscal period, NVR’s (NVR) 9.0% CAGR, KB Home’s (KBH) 10.9% CAGR, and Taylor Morrison’s (TMHC) 11.1% CAGR. However, many industry peers have also exceeded PulteGroup’s growth. For example, TopBuild (BLD) has achieved a 14.0% CAGR in the same period, D.R. Horton (DHI) has achieved a 17.1% CAGR in a similar period, Lennar Corporation (LEN) an even better 17.4% CAGR. Of the seven mentioned large peers & PulteGroup, PulteGroup ranks 4th in growth.

While revenue growth has been primarily in line with most industry peers, PulteGroup has achieved similar growth with much higher margins – the current 21.6% operating margin, growing historically alongside revenues, ranks first against the previously mentioned peers. The mentioned peers’ average stands significantly lower at 16.5%, enabling PulteGroup to grow at an incredible current 17.7% return on total capital.

With the great margin profile, I believe that PulteGroup’s financial profile stands good in the industry even during turbulent industry demand. The company has managed to grow well, but also diligently, as shown by the great margins. The long-term growth could slow down from potential weaker industry trends, but PulteGroup’s earnings profile should stay good regardless.

The Industry’s Short-Term Outlook Is Mixed, But the Long-Term Outlook Remains Good

Contrary to most of the past decade, the US home building industry’s outlook has recently been more uncertain, with higher interest rates and lower purchasing power amid high inflation. Most of PulteGroup’s large peers’ revenues turned downwards during 2023 at an average -2.4% revenue decline between the previously mentioned peers, whereas PulteGroup’s own growth also nearly halted into just 0.4% in the year.

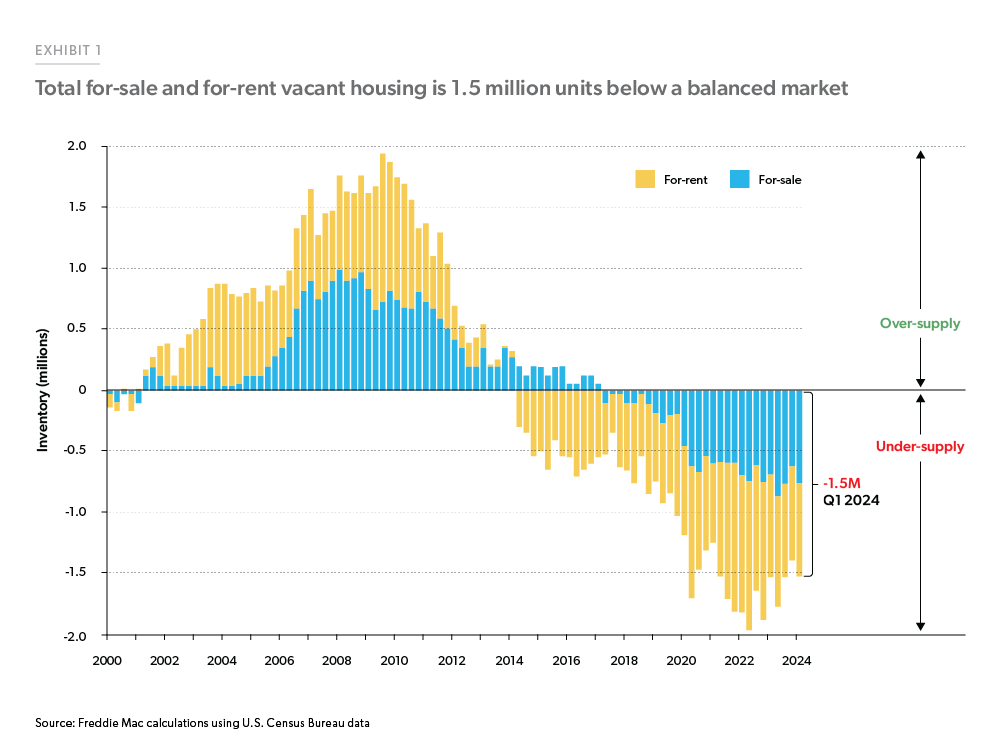

As interest rates have begun declining ahead of the Fed’s rate cuts, the home building industry’s demand could start to see upbeat momentum once again. Freddie Mac anticipates in the August forecast that lowering mortgage rates will start elevating the currently weaker industry demand in upcoming quarters, with a soft labor market and elevated inflation still causing some slowdown in the overall optimistic outlook. Also speaking for an improving industry outlook, Beazer Homes (BZH) also sees a good upcoming year ahead, as I recently wrote in an article on the stock.

PulteGroup already managed to grow revenues by 9.8% in Q2 with stable margins with a similar Q1 growth, highlighting the company’s good operational performance that beat Wall Street’s expectations.

Freddie Mac

While some uncertainties in the short-term outlook remain related to interest rates and especially a slower labor market, the long-term industry outlook still stands good. Freddie Mac still calculates a significant housing undersupply in the US market, continuing the great industry trend for home builders since the 2009 oversupply peak. The US population is also expected to grow at a healthy rate, providing a sustainable foundation for the industry – I don’t believe that an industry meltdown is likely in the upcoming years.

The undersupply has started to slow down slightly, though, potentially providing a more moderate long-term growth outlook past the short-term turbulence.

The PHM Stock Is Near Fairly Valued

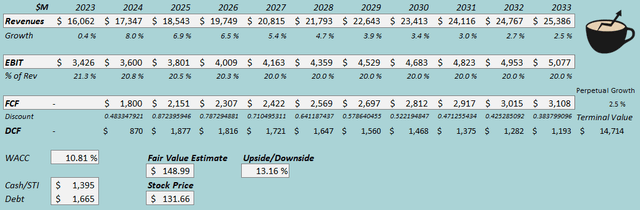

I constructed a discounted cash flow [DCF] model for PulteGroup’s stock to estimate a fair value.

In the model, I estimate good, but more moderate revenue growth going forward at a 4.7% CAGR from 2023 to 3033, and 2.5% perpetual growth afterward as industry trends seem to suggest good, but lower growth in the future.

I also estimate the incredibly good margin level to slow down slightly into a 20.0% sustained EBIT margin level in the upcoming years, as the record-high margin level could well slow down from more moderate industry demand. With the estimated growth, PulteGroup likely needs to tie up a good amount of working capital into land, as well as spend a good amount in capital expenditures to fuel the growth. As such, I estimate a moderate cash flow conversion.

As PulteGroup capitalizes its interest expenses, as is typical for home builders, I don’t subtract the outstanding debt from the fair value estimate with the interest expenses already being factored into free cash flow. I also only estimate the cost of equity in my CAPM.

DCF Model (Author’s Calculation)

The estimates put PulteGroup’s fair value estimate at $148.99. This is 13% above the stock price at the time of writing. While not attractive enough for a Buy rating, I believe that PulteGroup’s stock comes with a fair margin of safety when considering the excellent margin performance and fair growth.

CAPM

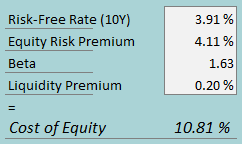

A weighted average cost of capital of 10.81% is used in the discounted cash flow [DCF] model, derived from a capital asset pricing model [CAPM]:

CAPM (Author’s Calculation)

As told, I only estimate the cost of equity for PulteGroup due to interest expenses being capitalized. To estimate the cost of equity, I use the 10-year bond yield of 3.91% as the risk-free rate. The equity risk premium of 4.11% is Professor Aswath Damodaran’s estimate for the US, updated in July. Yahoo Finance estimates PulteGroup’s beta at 1.63. With a liquidity premium of 0.2%, the cost of equity stands at 10.81%.

Peer Comparison Highlights a Fair Margin of Safety

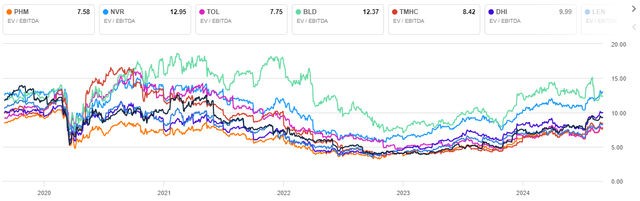

Against the mentioned peers in the home building industry, PulteGroup trades at a cheaper EV/EBITDA – PulteGroup’s 7.6 trailing EV/EBITDA is well below the peers’ average of 9.8, providing a margin of safety to the stock’s valuation in the industry.

Peer EV/EBITDA (Seeking Alpha)

As PulteGroup’s revenue growth is in line with peers, but the company has achieved far better profitability, I don’t believe that such a lower valuation reflects a poorer performance. Rather, the stock seems to come at a margin of safety.

Takeaway

In the past decade, PulteGroup has grown with incredibly good margins in the greatly performing home building industry. The industry’s weaker short-term outlook from 2023 has disturbed the growth temporarily with higher interest rates and a weaker labor market, but Freddie Mac sees a recovery ahead. With the long-term industry outlook standing healthy, and with PulteGroup, Inc.’s moderate valuation, I initiate the stock at a Hold rating.

Read the full article here