Investment Rundown

Thermon Group Holdings, Inc. (NYSE:THR) has seen impressive revenue growth as the company is charging up to be a growth play. The Q1 FY2024 results land at $106 million in revenues which was largely caused by strong sales growth in North America and Asia Pacific. However, with the run-up the company has had in the last 12 months alone, I see a consolidation phase starting right now. There is still a high interest rate environment and that might be staying around for quite a long time still, according to some. Over the years THR has reduced the long-term debts very well but if they seek to accelerate expansions and revenue growth further then more debt may have to be taken on, which in this environment would hurt the bottom line as interest expenses would grow.

I think right now THR is better suited as a hold in anticipation of strong earnings results in the next report. Should the report produce disappointing results or not the double-digit top-line growth I want to see, there may be a big drop in valuation seeing as the price has grown so quickly last few months.

Company Segments

THR is a global provider of tailored heating solutions for diverse process industries. Their product range includes control systems, monitoring solutions, and heat tracing technologies. Renowned for their environmental heating solutions, they operate under respected brand names like Ruffneck and Caloritech. Beyond their core offerings, Thermon also supplies heating equipment for transportation, filtration products, and rail and transit solutions. With a vast network of sales representatives and distributors, they serve an array of industries, including semiconductors, pharmaceuticals, renewable energy, and various others. Their comprehensive solutions cater to the heating needs of clients worldwide.

Thermon Group’s strategic move in 2017 to acquire CCI Thermal Technologies Inc. for CAD 258 million is a noteworthy example of such expansion through acquisition. CCI Thermal Technologies, a provider of advanced heating and filtration solutions, brought valuable assets to the Thermon Group. This acquisition significantly diversified Thermon’s product offerings and enhanced its position in the industrial heating and filtration market, reinforcing its competitive edge in the industry. Over the last 5 years, the topline growth rate has been 5.51% on average and has only really accelerated in the last few years following further integration and utilization of the application the company made.

Investor Presentation

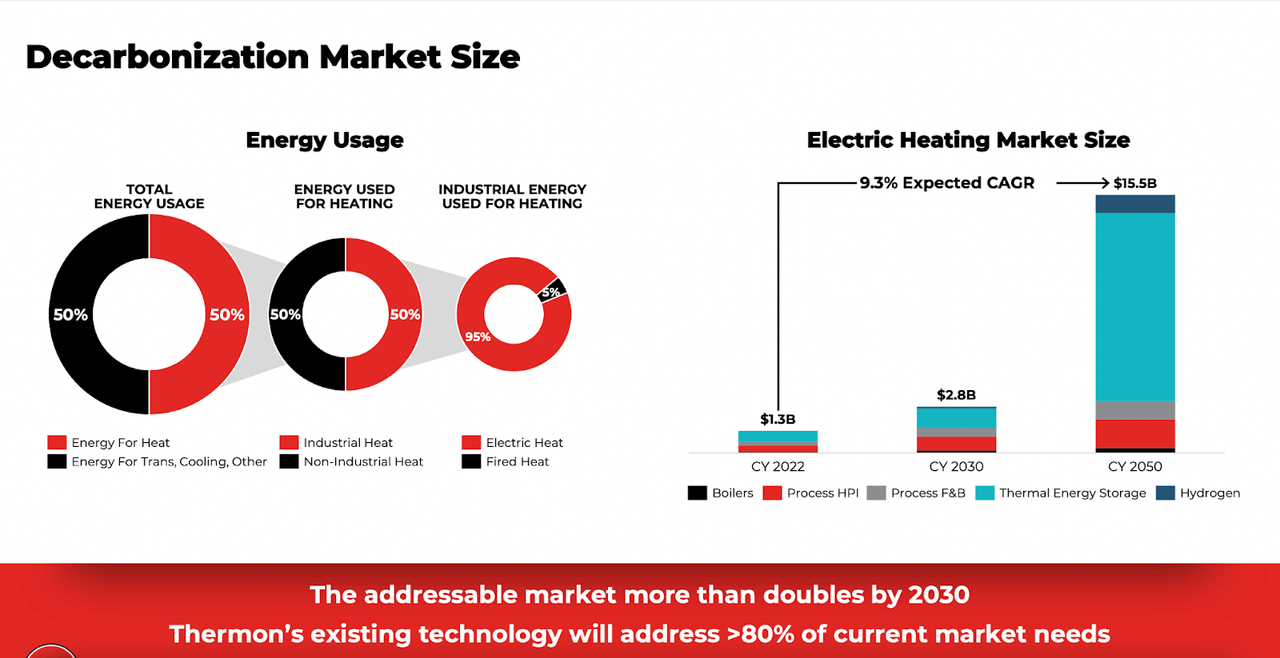

The market that THR is operating in right now is quite large and is expected to continue to grow even further in the coming years. Until 2050 there is an expectation of a 9.3% CAGR which if THR continues to make strategic acquisitions like they have been could potentially achieve similar top-line growth elves. With the company also placing a focus on cutting down on their leverage I think they are in a strong financial position to take on more debt to finance more acquisitions and buyouts. This assumption is also with the notion that THR will maintain margins and continue to improve upon them.

Macrotrends

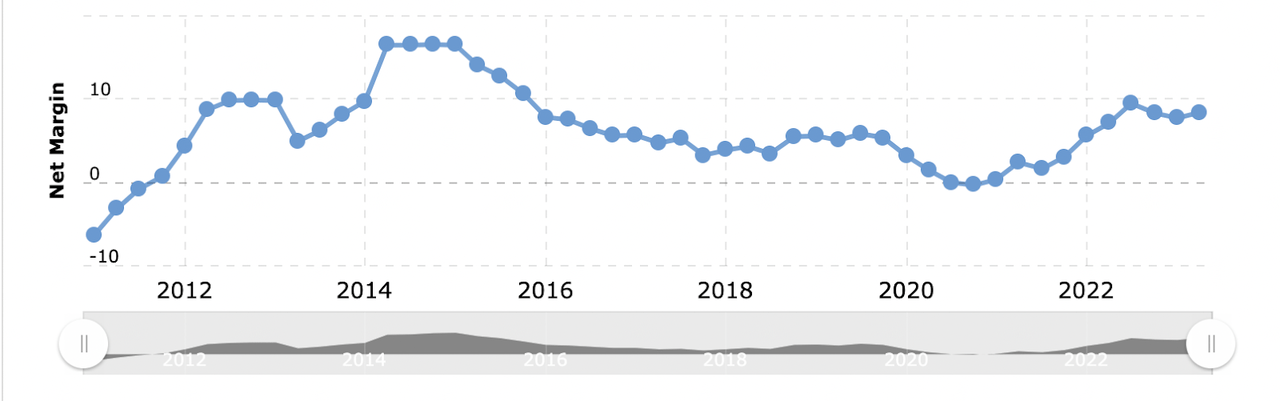

As seen above the company is in a steady uptrend over the last few quarters as they reached a bottom back in 2021 for their net margins. Going forward I think that THR will crucially have to focus on achieving and maintaining strong organic growth rates. They have the market trends in their favor energy for heat is still a massive part of the total energy usage in the US and internationally as well.

Earnings Highlights

The last quarter yielded quite impressive top-line growth for the company and I think this is something that may be kept up too. The sales grew by 12% as markets like North America and Asia Pacific showed resilience.

Margins expanded quite as well and gross profits grew to $47 million, a 27% YoY increase. Bookings are now at $120 million which puts THR at a book-to-bill ratio of 1.12x. The positive results have been a key factor in the growth of the share price over the last 12 months. In terms of valuation, THR is still below broader sector averages. On earnings multiple for example it’s nearly 11% below and on an EV/EBIT it’s 12% below.

Investor Presentation

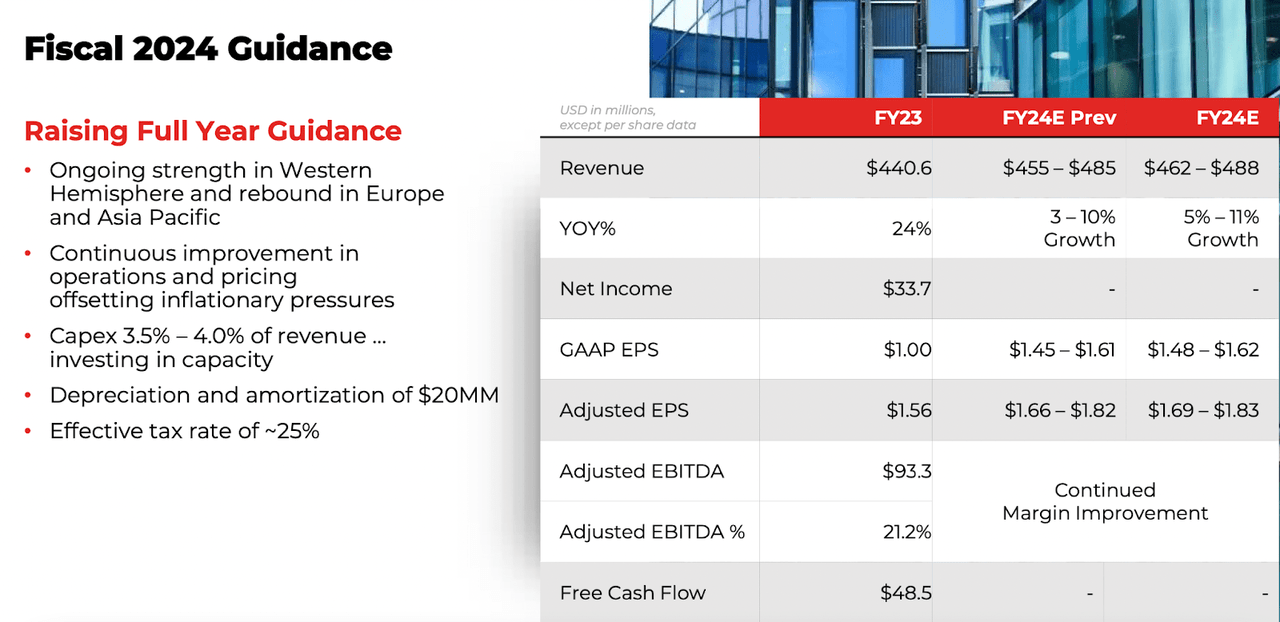

The guidance for 2024 looks very good as THR is raising it following signs of robust demand. Revenue is set to grow to $462 – $488 million in total. That means a YoY growth rate of 5 – 11% and EPS of $1.83 on the higher end. This means THR is only really trading at a 2024 p/e of 14 and seeing as it has achieved stronger growth rates than the electric heating market so far as shown in the pictures above, justifying a higher premium seems reasonable. I would be comfortable holding at a p/e of 18 even, leaving a 2024 price target of $32 or an upside of 26% right now. This type of upside seems very appealing but I do stand strong with my hold rating. You still benefit from holding shares even if the upside is strong. My reasoning behind a hold is tied to their potentially still being some risks with short-term headwinds like rising interest rates or more medium-term risks like prolonged higher interest rates. This would limit the amount of capital that THR could have access to and potentially harm revenue growth outlooks.

Risks

THR product demand is subject to fluctuations in various industries, and abrupt changes in this demand can significantly influence their sales and overall revenue. Moreover, price volatility in key raw materials, particularly petrochemicals and electrical components, can lead to shifts in manufacturing costs, ultimately impacting profit margins. THR needs to navigate these industry-specific challenges effectively to maintain a stable financial performance.

Seeking Alpha

Another short-term concern pertains to THR’s rapid share price growth within a relatively brief timeframe, potentially raising the risk of consolidation or making it more susceptible to a significant decline in the event of a broader market downturn.

Final Words

THR has had strong results so far but I am waiting for the next few reports to show a maintenance of this momentum and an ability to continue generating strong bottom-line margins. The upside is appealing but I am sticking with a hold for now as you are still getting the benefit of a potentially appreciating share price. Rating THR a hold for now.

Read the full article here